RBS 2013 Annual Report Download

Download and view the complete annual report

Please find the complete 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Serve customers well.

This is our purpose.

rbs.com

Annual Report and Accounts 2013

Table of contents

-

Page 1

Annual Report and Accounts 2013 Serve customers well. This is our purpose. rbs.com -

Page 2

... wide range of products and services to personal, commercial and large corporate and institutional customers through its two main subsidiaries, The Royal Bank of Scotland and NatWest, as well as through a number of other well-known brands including Citizens, Charter One, Ulster Bank and Coutts. Why... -

Page 3

... Report 2013 Financial Results Our purpose and values Our business model and strategy RBS at a glance UK Retail UK Corporate Wealth International Banking Ulster Bank US Retail & Commercial Markets Non-Core Business Services Governance at a glance Chairman's statement Chief Executive's review... -

Page 4

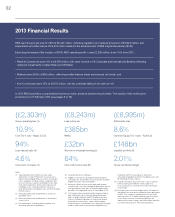

... Tier 1 ratio - FLB lll (3) 94% Loan:deposit ratio (4) £32bn Short-term wholesale funding (5) £146bn Liquidity portfolio (6) 4.6% Core return on equity (7) Notes: (1) Operating proï¬t/(loss) before tax, own credit adjustments, Payment Protection Insurance costs, Interest Rate Hedging Products... -

Page 5

...income in UK Corporate and International Banking offsetting improved impairments in Ulster Bank and UK Retail. Markets operating proï¬t, excluding £18 million of impairments related to the creation of RCR, was down 58% to £638 million, reï¬,ecting its smaller balance sheet and reduced risk levels... -

Page 6

... RBS held 28.5% of Direct Line Insurance Group. On 26 February 2014, RBS announced that it had entered into a placing agreement to complete the sale of its residual interest (except for 4.2 million shares held to satisfy long term incentive plan awards granted by RBS to Direct Line Group management... -

Page 7

... of new facilities were made available to new and existing clients. RBS also helped UK companies, universities and housing associations to raise £24.7 billion through bond issues in 2013. RBS repaid all its borrowings from the Bank of England Funding for Lending Scheme (FLS) in 2013 but continues... -

Page 8

... customers, shareholders and communities. Our values: Serving customers We exist to serve customers. We earn their trust by focusing on their needs and delivering excellent service. Working together We care for each other and work best as one team. We bring the best of ourselves to work and support... -

Page 9

... customers well, and work to fully embed our values in everything we do. Our employees believe in the goals of RBS and already 1 in 2 people have seen a change in how their team works. More information on our progress in 2013 to build an engaged and inclusive workforce will be available in our RBS... -

Page 10

... our debt securities we have issued. We also earn fees from ï¬nancial services and other products we provide to our customers as well as rental income from assets we lease to our customers. Our Markets business earns income from client driven trading activities particularly Rates, Currencies, Asset... -

Page 11

... 2013 RBS announced a full review of its customer-facing businesses, its IT and operations, and its organisational and decision-making structures. As a result of this review, we have announced a refreshed strategic direction with the ambition of building a bank that earns its customers' trust... -

Page 12

... Key Measures Value drivers Return on equity (1) Cost:income ratio Risk measures Core Tier 1 ratio Loan:deposit ratio Short-term wholesale funding (STWF) Liquidity portfolio (7) Leverage ratio (8) 4% (4) 154% (5) £297bn (6) £90bn (6) 28.7x (9) (31%) (2) 97% (3) Worst point 2012 Core 8.9% 59% Group... -

Page 13

... RBS a really good bank demands more. That is why we are still investing more effort in all of our businesses to serve customers well. RoW 4% Centre 1% UK Retail 25% Europe 9% Markets 17% USA 24% Total income by region 2013 UK 63% US Retail & Commercial 15% Ulster Bank 4% International Banking... -

Page 14

... 2013. • Customer deposits increased by 7%, above UK market average. • Net interest margin held steady, despite tightening margins on new mortgages. Lower income was earned on current account balances, but savings margins improved. Building a better bank that serves customers well In March 2013... -

Page 15

... cost of repairs and replacement stock while businesses wait for insurance claims to be paid. UK Corporate Chris Sullivan Chief Executive Performance highlights Return on equity (%) Cost:income ratio (%) Loan:deposit ratio (%) Risk-weighted assets (£bn) 2013 7.9 50 80 86.1 2012 14.5 44 82 86.3 23... -

Page 16

... value of our inter-connected world. Wealth Rory Tapner Chief Executive Performance highlights Return on equity (%) Cost:income ratio (%) Loan:deposit ratio (%) 2013 12.0 77 45 12.0 2012 13.1 75 44 12.3 6% Risk-weighted assets (£bn) Contribution to Core income Performance overview • Operating... -

Page 17

...and communication, the changes were successful. TomTom now has one, single payment process for suppliers across the world. International Banking John Owen Chief Executive Performance highlights Return on equity (%) Cost:income ratio (%) Loan:deposit ratio (%) Risk-weighted assets (£bn) 2013 3.9 73... -

Page 18

..., creating much-needed new homes as well as hundreds of construction jobs. Ulster Bank Jim Brown Chief Executive Performance highlights Return on equity (%) Cost:income ratio (%) Loan:deposit ratio (%) 2013 (32.4) 64 120 30.7 2012 (21.8) 62 130 36.1 4% Risk-weighted assets (£bn) Contribution to... -

Page 19

...efï¬ciency and security for our customers. US Retail & Commercial Bruce Van Saun Chief Executive, RBS Citizens and Head of RBS Americas Performance highlights Return on equity (%) (1) Cost:income ratio (%) (1) Loan:deposit ratio (%) Risk-weighted assets (£bn) 2013 7.2 73 91 56.1 2012 8.9 71 86 56... -

Page 20

...income in 2013 compared with 2012 reï¬,ected both the strategic scaling back of the balance sheet and risk reduction in a difï¬cult market environment with client activity limited by uncertainty over monetary policy in the US. For further information see page We provide ï¬nancing, risk management... -

Page 21

... different criteria and are not directly comparable. For further information see page 154 Business Services Simon McNamara Group Chief Administrative Ofï¬cer • We issued two million time-saving contactless cards in 2013 allowing customers to make quick and easy payments for everyday items under... -

Page 22

... and operating performance. The Board fully supports our new values, which were launched in 2013 and focus on serving customers, working together, doing the right thing and thinking long term. It is vital that the Board continues to set the tone from the top to drive essential cultural change and... -

Page 23

... full committee report on pages 64 and 65. Executive Committee Supports the Group Chief Executive in managing the Group's businesses. It reviews strategic issues and initiatives, monitors ï¬nancial performance and capital allocations and considers risk strategy, policy and management. RBS Capital... -

Page 24

... down as Group Chief Executive. We selected Ross McEwan to re-energise the task of building a bank that earns its customers' trust, improves operating efï¬ciency and can move down the path back to full private ownership. The Board and I want to thank Stephen Hester for his dedication to RBS and to... -

Page 25

... trusted bank we aspire to be. The Board fully supports the new values we launched in 2013, and it is vital that we continue to set the tone from the top in the coming year to drive essential cultural change. On many of these issues we have engaged closely with HM Treasury (HMT) through UK Financial... -

Page 26

..., and where we can serve their needs better than anyone else." Chief Executive's review Ross McEwan Chief Executive Since 2009 RBS has cleaned up the world's largest bank balance sheet by removing more than £1 trillion in assets. This was a remarkable achievement, born of absolute necessity, but... -

Page 27

... ï¬nancial services group when in fact we are now largely a UK-based bank. Our operating model means our customers and shareholders end up paying for parts of the business that cost too much and deliver too little in their interests. This needs to change. RBS needs a strategy that will address the... -

Page 28

... every business in our current structure will be best placed to deliver on our strategy. Technology investment will enable some to improve service at a rate that outpaces the market, but others will not. For those activities where we can't see a clear path to being number one, we will review on the... -

Page 29

Chief Executive's review 27 announced our intention to remove £9 billion of the worst credit risks from the Ulster Bank balance sheet. Our second step is focused on improving customer experience and shareholder return. As outlined in November, we are reviewing our business to make it viable and ... -

Page 30

... Bank Rate remained at 0.5%, although market rates increased towards the end of the year on expectations of tighter monetary policy in the United States. There were no additions to the stock of assets purchased through the quantitative easing programme. In August 2013, the Monetary Policy Committee... -

Page 31

... the bank, and the Group continued to suffer from legacy conduct issues during 2013, notably in relation to PPI, Interest Rate Hedging Products and mortgage-backed and other securities litigation. During the year, the Group focused on embedding good conduct at the heart of its business, working to... -

Page 32

... Financial Group, in particular, are cornerstones of this capital strategy. Top and emerging risk scenarios RBS identiï¬es and monitors its top and emerging risk scenarios. A number attracted particular attention from senior management during 2013 which are discussed below. For further information... -

Page 33

..., and attended by senior representatives from the customer facing divisions as well as Human Resources, Sustainability, Risk Management, Communications, Legal, Strategy and Corporate Services. The Chairman of the board also regularly attends the meetings. The work of the Committee is essential to... -

Page 34

..., achieving our best ever score in 2013. The Index ranks companies' corporate sustainability performance, based on analysis of economic, environmental and social issues like corporate governance, risk management, branding and climate change. The CDP is an independent, investor-driven organisation... -

Page 35

... operations. We have adopted and contributed to a number of internationally accepted codes, notably the Equator Principles and the UN Global Compact, which speciï¬cally address the management of human rights issues. The RBS Group Code of Conduct sets out the standards we expect our people to work... -

Page 36

34 Approval of Strategic Report The Strategic Report for the year ended 31 December 2013 set out on pages 1 to 33 was approved by the Board of directors on 26 February 2014. By order of the Board. Aileen Taylor Secretary 26 February 2014 Chairman Philip Hampton Executive directors Ross McEwan ... -

Page 37

... the Chairman Our governance structure Our Board Executive Committee Corporate governance Report of the Group Nominations Committee Report of the Group Audit Committee Report of the Board Risk Committee Report of the Group Sustainability Committee Directors' Remuneration Report Other Remuneration... -

Page 38

... search, Stephen was succeeded by Ross McEwan on 1 October 2013 and Ross now has his sights firmly set on building a bank focused on our customers and shareholders. Also on 1 October 2013, Bruce Van Saun took up his new role as Chairman and Chief Executive of RBS Citizens Financial Group, Inc... -

Page 39

... Board also received support from the Group Secretary in a number of other areas related to board effectiveness such as Board process and information flows, continuing professional development and induction for new directors. Corporate governance This is the first year that we are required to report... -

Page 40

...governance structure RBS Capital Resolution Board Oversight Committee Group Board The main decision making forum at Group level, setting the strategic direction of the Group and ensuring that the Group manages risk effectively. The Board is accountable to shareholders for financial and operational... -

Page 41

... Group Executive for Retail Banking Services and Executive General Manager responsible for the branch network, contact centres and third party mortgage brokers at Commonwealth Bank of Australia, Managing Director of stockbroking business First NZ Capital Securities, and Chief Executive of National... -

Page 42

...chief executive of Standard Life plc. He was also previously a director of the Association of British Insurers, a member of the former Chancellor of the Exchequer's High Level Group on Financial Services and Chairman of the Edinburgh World City of Literature Trust. In 2007 he was the Prince of Wales... -

Page 43

... as a Durham chartered accountant. He then moved into banking • Chairman of the Somerset House Trust joining SG Warburg, specialising in corporate finance, • Chairman of the Boat Race Company and was appointed as Co-Head and Managing Director Limited of its US investment banking business in 1989... -

Page 44

...services and risk management, including previous Committee membership(s): responsibility for Aviva's continental European and • Board Risk Committee (Chair) International life and long-term savings businesses. He • RCR Board Oversight Committee (Chair) held a number of senior executive positions... -

Page 45

... interest rate products, foreign exchange, asset backed securities, emerging markets, credit fixed income and debt capital markets. In this capacity, he oversees businesses which provide financing, risk management and advisory services to major corporations, financial institutions and public sector... -

Page 46

... Chief Executive Officer of RBS Citizens Financial Group, Inc. and Head of RBS Americas in October 2013. Prior to taking up his current role, Bruce was Group Finance Director and a director of the Company, RBS and NatWest having been appointed to those positions in 2009. Bruce has more than 30 years... -

Page 47

...of reference include key aspects of the company's affairs reserved for the Board's decision and are reviewed at least annually. The terms of reference are available on rbs.com>about us. Chairman The role of Chairman is distinct and separate from that of the Group Chief Executive and there is a clear... -

Page 48

... team. The balance between non-executive and executive directors enables the Board to provide clear and effective leadership across the Group's business activities. The standard terms and conditions of appointment of non-executive directors are available on rbs.com or from RBS Secretariat. Board... -

Page 49

... opportunity to engage directly with divisional management on key issues and supports the Board's succession planning activity. Group Chairman Group Chief Executive Group Finance Director Senior Independent Director Board committee Chairs Group Secretary Group Chief Risk Officer Head of Conduct and... -

Page 50

... into statutory audit services; Government reforms on executive remuneration and reporting; and Developments in European company law and corporate governance. • preparing a detailed framework of key themes for discussion and questions which was used to structure individual meetings held... -

Page 51

... complex work well throughout the year, providing strong support to the Board. • • the Group Chief Executive and Group Finance Director meet regularly with UKFI, the organisation set up to manage the Government's investments in financial institutions, to discuss the strategy and financial... -

Page 52

... into account business requirements and industry developments. In 2013 discussions focused principally on executive director succession and the search for new non-executive directors. The Board also held a separate session on succession planning for the Executive Committee in June 2013. Group Chief... -

Page 53

... The chart below sets out the tenure of non-executive directors. The chart below details the gender diversity of the Board. Board and committee membership The Committee reviewed the membership of the Group Sustainability Committee during 2013 following feedback from the 2012 evaluation. It was... -

Page 54

...by the Group Audit and Board Risk Committees to the Group's business divisions and control functions continued in 2013. The programme allows members of the Committees to spend additional time with areas of the business which the Committees judge would benefit from a more detailed review. Invitations... -

Page 55

... focus. During 2013, the Committee spent a week in Asia to review the Markets, International Banking, Wealth, Business Services and Group Finance operations in the region. Internal Audit management made presentations to the Committee at two separate visits, covering functional strategy, bench... -

Page 56

... instruments carried at fair value including the Group's credit market exposures; the appropriateness of the carrying value of goodwill and other intangible assets, placing particular focus on International Banking and RBS Citizens Financial Group, Inc. Following an impairment review at year end... -

Page 57

... with the RBS Group Pension Fund. The Committee will monitor the investment strategy, capital impact and funding of the scheme during 2014, as negotiations progress. As discussed in the report of the Board Risk Committee, changes to the Divisional Risk and Audit Committee structure, designed to... -

Page 58

... services related to the accounting records or financial statements; the experience and expertise of the senior members of the engagement team; the proposed scope of the audit work planned and executed; the quality of dialogue between the External Auditor, the Committee and senior management... -

Page 59

... to the ad hoc approval process. Information on fees paid in respect of audit and non-audit services carried out by the External Auditor can be found in Note 5 to the consolidated accounts on page 403. The Group Audit Committee reviews the policy annually and prospectively approves the provision of... -

Page 60

...of conduct risk: employee conduct; market conduct; corporate conduct; and conduct towards customers. These standards have been applied in the Committee's consideration of issues including the review of the sale of interest rate hedging products to SME customers. The Committee has also placed renewed... -

Page 61

... into business as usual. More detailed information on each of these areas is set out in the Board Risk Committee report that follows. 2013 was a challenging year for the Board Risk Committee and I would like to extend my gratitude to my fellow members and to the Group's senior leadership team for... -

Page 62

... sessions with the Risk Management function to consider key risk areas and the risk strategy and operating model. Full details about the programme of visits is set out in the Report of the Group Audit Committee on page 53. Membership of the Board Risk Committee The Board Risk Committee comprises at... -

Page 63

... and policy RBS has a clear risk strategy supported by well defined strategic risk objectives. The members of the Board Risk Committee provide input to the overarching strategy for the business on an ongoing basis. During 2013, the Board Risk Committee reviewed the implementation of the Group Policy... -

Page 64

... new market risk caps and changes to the existing limits. In the second half of 2013 the Committee reviewed proposed changes to the Single Name Concentration framework for Banks and a new Single Name Concentration grid for Large Corporates. The Committee also considered the Economic Capital model... -

Page 65

... of the Board Risk Committee Risk architecture The Committee reviewed the preparations underway to ensure compliance with the new best practice principles that had been defined by the Basel Committee of Banking Supervision (BCBS) for internal risk reporting and data aggregation practices, which... -

Page 66

... conduct that supports the Group's values of serving customers, working together, doing the right thing and thinking long term; oversight of how the Group is balancing the needs of all its stakeholder groups including customers, investors, employees, regulators and communities/society and alignment... -

Page 67

... Committee held six Committee meetings in 2013 in addition to seven stakeholder engagements sessions. Both were attended by senior representatives from the customer facing divisions as well as Human Resources, Sustainability, Risk Management, Communications, Legal, Strategy and Corporate Services... -

Page 68

... Dear Shareholder, This year's remuneration report is published at an important moment for RBS. Five years on from the company's rescue, RBS is substantially safer and smaller, has a new Group Chief Executive, and has embarked on a new strategy positioning customers at its centre. In this changing... -

Page 69

...in 2013. Employee engagement is strong and clear evidence that key values are being embedded across the Group. • Decisions made on pay • Full details of decisions for both current and former directors are set out in this report. Ross McEwan's salary on appointment as Group Chief Executive... -

Page 70

... made across the business in 2014 will be less than 2%. RBS is a major UK employer and, as a bank playing a key role in the economic recovery, we understand the importance of getting our pay decisions right. We are committed to a high level of transparency and I believe the new reporting and voting... -

Page 71

... are directly applicable although any future salary increases will take into account performance rating during the year. Element of pay Base salary Operation Maximum potential value Paid monthly and reviewed annually. Determined annually. The rates for 2014 are as follows: Group Chief Executive... -

Page 72

...each): of fixed pay (i.e. base salary, • Economic Profit fixed share allowance, • Relative Total Shareholder benefits and pension). For Return (TSR) these purposes awards will • Safe and Secure Bank be valued in line with the • Customers and People European Banking Authority rules, including... -

Page 73

... shareholders. Changes for Executive Directors • EDs will no longer be eligible to receive annual bonuses. • The new structure outlined in the policy table introduces a fixed share allowance for EDs which will be released in equal tranches over a five year period. However, the Group Chief... -

Page 74

... and the level of fees paid to directors of comparable major UK companies. Non-executive directors do not participate in any incentive or performance plan. Non-executive directors' fees are reviewed regularly. Maximum potential value The rates for the year ahead are set out in the annual report on... -

Page 75

.... An annual employee opinion survey takes place which includes a number of questions on pay and culture. This includes questions as to whether employees believe they are paid fairly for the work they do, how remuneration at RBS compares to other financial services organisations and how good a job... -

Page 76

... review process, the disciplinary procedure and terms for dismissal in the event of personal underperformance or breaches of RBS policies. The Committee retains the discretion to make payments (including but not limited to professional and outplacement fees) to mitigate against legal claims... -

Page 77

... changes. The process takes place in sufficient time for shareholder views to be considered prior to the Committee making any final decisions on remuneration and variable pay awards. Details of shareholder voting on the resolution to approve the last remuneration report can be found in the annual... -

Page 78

... of the Asset Protection Scheme Senior Oversight Committee. (5) Art Ryan is a non-executive director of RBS Citizens Financial Group, Inc. for which he received fees of US$131,000 for the period to 30 September 2013, the date he retired from the Group Board. There have been no payments made to... -

Page 79

... applicable as CEO UK Retail and 24 months against the targets applicable as Group Chief Executive. Notes: The number of shares awarded is based on a multiple of salary and the award price is calculated based on the average share price over five business days prior to the grant date of £3.092 In... -

Page 80

.... Based on share price performance up to 31 December 2013, the threshold targets have not yet been met. Majority of Balance Sheet and Risk measures are currently on track or ahead of target. Cost:income ratio remains challenging to achieve largely due to market-driven income pressures. Positive... -

Page 81

... Financial Group and Head of RBS Americas. He continues to be employed within RBS and therefore no termination payment was made in connection with this change of role. Directors' interests in shares and shareholding requirements (audited) The target shareholding level for the Group Chief Executive... -

Page 82

... the Group's share plans (audited) Long-Term Incentive Plan (LTIP) awards Awards to executive directors under the LTIP are structured as conditional rights to receive shares and are subject to performance conditions and clawback provisions prior to vesting. Awards held at 1 January 2013 (or date of... -

Page 83

... 2013 and 2012 compared with the percentage change in the average remuneration of RBS employees on a global basis. In each case, remuneration is based on salary, benefits and annual bonus. The Group Chief Executive remuneration reflects the change in remuneration arrangements for the new Group Chief... -

Page 84

.... 2013 £m 2012 £m change Remuneration paid to all employees (1) Distributions to holders of ordinary shares Distributions to holders of preference shares Taxation and other charges recognised in the income statement: - Social security and other payments (2) - Bank levy - Corporation tax... -

Page 85

Annual report on remuneration 2014 Annual objectives for the Group Chief Executive and Group Finance Director The executive directors' annual objectives, as set out below, are approved by the Committee and reflect the Group's key strategic priorities. The Board Risk Committee has approved the risk ... -

Page 86

... Profit after Tax is Operating Profit taxed at a standard tax rate. • Attributed Equity is defined as equity allocated to the businesses, calculated as a function of the businesses risk-weighted asset base. • Current Cost of Equity is 11.0%, which is subject to review at least annually. Details... -

Page 87

... and deferral structure. Second quarter • Group Chief Executive departure terms and consideration of appointment and remuneration terms for various senior positions. Presentations from Markets, Corporate and Ulster Bank on business and strategic priorities and people plans. Review of the... -

Page 88

... ordinary share capital (including the B share capital), leaving an available dilution headroom of 5.8%. The company meets its employee share plan obligations through a combination of new issue shares and market purchase shares. Penny Hughes Chair of the Group Performance and Remuneration Committee... -

Page 89

... (1) Remuneration earned for period worked in 2013 at RBS for members of Group Executive Committee plus Group HR Director. (2) Disclosure includes prior year long-term incentive awards which vested during 2013. The amounts shown reflect the value of vested awards using the share price on the day the... -

Page 90

... could have a material impact on the income statement; and - Key control function roles The RBS Staff Dealing Rules and the conditions attaching to discretionary share-based awards prohibit the use of any personal hedging strategies to lessen the impact of a reduction in value of such awards. 88 -

Page 91

... and/or new information would change the annual bonus and/or LTIP decisions made in previous years, and/or the decisions to be made in the current year. • The process for review assessments (which consider material risk management, control and general policy breach failures, accountability for... -

Page 92

...high levels of income including those involved in managing trading activity and supporting clients with more complex financial transactions, including financial restructuring. Those responsible for managing our balance sheet and liquidity and funding positions across the business. Employees managing... -

Page 93

... by the Group, which operated throughout the year ended 31 December 2013 and to 26 February 2014, the date the directors approved the Report and Accounts. This is confirmed by a semi-annual Control Environment Certification process which requires senior members of the executive and management to... -

Page 94

... affect, the company's internal control over financial reporting. The New York Stock Exchange As a foreign issuer with American Depository Shares representing ordinary shares, preference shares and debt securities listed on the New York Stock Exchange (the "NYSE"), the company is not required... -

Page 95

...The directors present their report together with the audited accounts for the year ended 31 December 2013. Group structure The company is a holding company owning the entire issued ordinary share capital of The Royal Bank of Scotland plc, the principal direct operating subsidiary undertaking of the... -

Page 96

... 2013, the Group reached an agreement with an investor consortium led by Corsair Capital and Centerbridge Partners for an investment in these businesses ahead of a stock market flotation. This includes 308 RBS branches in England and Wales and 6 NatWest branches in Scotland. The new bank will... -

Page 97

...Board representation. Further information on male/female representation at various levels of employment in the Group is included in the Strategic report on page 33. Further details on the Board diversity policy can be found at rbs.com>about us. This year the business has been recognised for its work... -

Page 98

... of ensuring 2013 coupon payments on discretionary hybrid capital securities were partly neutralised from a Core Tier 1 capital perspective. The shares were allotted to UBS AG at the subscription prices and determined by reference to the average market prices during the sale periods set out below... -

Page 99

... to all trustees of the Group's pension schemes. Post balance sheet events Other than those matters detailed in Note 42 on the consolidated accounts, there have been no significant events between the year end and the date of approval of these accounts which would require a change to or disclosure in... -

Page 100

... proposed that the Group's longstanding policy of not making contributions to any political party be changed. Shareholders will be asked to renew this authorisation at the Annual General Meeting in 2014. Aileen Taylor Secretary 26 February 2014 The Royal Bank of Scotland Group plc is registered in... -

Page 101

... are of the opinion that the Annual Report and Accounts, taken as a whole, is fair, balanced and understandable and provides the information necessary for shareholders to assess the company's performance, business model and strategy. By order of the Board Philip Hampton Chairman 26 February 2014... -

Page 102

... of information Forward-looking statements Description of business Competition Risk factors Key financials Summary consolidated income statement Results summary Analysis of results Divisional performance RBS Capital Resolution Consolidated balance sheet Cash flow Capital resources Reconciliations... -

Page 103

...the term 'company' or 'RBSG' means The Royal Bank of Scotland Group plc, 'RBS', 'RBS Group' or the 'Group' means the company and its subsidiaries, 'the Royal Bank' or 'RBS plc' means The Royal Bank of Scotland plc and 'NatWest' means National Westminster Bank Plc. The company publishes its financial... -

Page 104

... the income statement. Reconciliations between managed and statutory results are detailed on pages 169 to 171. Glossary A glossary of terms is provided on pages 549 to 556. own credit adjustments; Payment Protection Insurance (PPI) costs; Interest Rate Hedging Products redress and related costs... -

Page 105

... senior management or other key employees; regulatory or legal changes (including those requiring any restructuring of the Group's operations) in the UK, the US and other countries in which the Group operates or a change in UK Government policy; changes to regulatory requirements relating to capital... -

Page 106

...'s trading and structuring teams to meet the client's objectives across financing, risk management, investment, securitisation and liquidity. A new strategy for the Markets division was announced in June 2013 enabling RBS to concentrate on its core customers' needs where the Markets business is... -

Page 107

... NatWest branches in Scotland. The new bank will be called Williams & Glyn, the brand RBS used for its branches in England and Wales before 1985. In March 2013 and September 2013, the Group sold a further 16.8% and 20% respectively of the total issued share capital in Direct Line Insurance Group plc... -

Page 108

...new entrants active and seeking to build their platforms by acquiring businesses made available through restructuring of incumbents. The Group distributes life assurance products to banking customers in competition with independent advisors and life assurance companies. In the UK credit card market... -

Page 109

... senior management, which may include members of the Group Board, or other key employees, and it may suffer if it does not maintain good employee relations. The Group is subject to a number of regulatory initiatives which may adversely affect its business, including the UK Government's adoption... -

Page 110

... Group including on dividend policy, the election of directors or appointment of senior management or limiting the Group's operations. The offer or sale by the UK Government of all or a portion of its shareholding in the company could affect the market price of the equity shares and other securities... -

Page 111

... own debt, Asset Protection Scheme, strategic disposals and RFS MI. In the statutory consolidated income statement, these items are included in total income. (2) Operating (loss)/profit on a managed basis excludes own credit adjustments, PPI costs, Interest Rate Hedging Products redress and related... -

Page 112

Business review Summary consolidated income statement for the year ended 31 December 2013 In the income statement set out below, own credit adjustments, PPI costs, Interest Rate Hedging Products redress and related costs, regulatory and legal actions, sovereign debt impairment and related interest ... -

Page 113

Business review Managed 2013 £m 2012* £m 2011* £m 2013 £m Statutory 2012* £m 2011* £m Basic loss per ordinary and equivalent B share from continuing operations Own credit adjustments Payment Protection Insurance costs Interest Rate Hedging Products redress and related costs Regulatory and ... -

Page 114

... Capital. The UK bank levy is based on the total chargeable equity and liabilities as reported in the balance sheet at the end of a chargeable period. The cost of the levy to the Group for 2013 was £200 million compared with £175 million in 2012. Interest Rate Hedging Products redress and related... -

Page 115

...Markets and International Banking (M&IB) that took place during 2012. Liability management exercises undertaken by the Group during 2012 resulted in a net gain of £454 million (2011 - £255 million). The UK bank levy is based on the total chargeable equity and liabilities as reported in the balance... -

Page 116

... tax assets in Australia following the strategic changes to the Markets and International Banking businesses announced in January 2012 and the effect of the two reductions of 1% in the rate of UK corporation tax enacted in March 2012 and July 2012 on the net deferred tax balance. Earnings per share... -

Page 117

Business review Analysis of results Net interest income Managed 2013 £m 2012* £m 2011* £m 2013 £m Statutory 2012 £m 2011 £m Interest receivable (1,2,3,4,5) Interest payable (1,3,4) Net interest income Yields, spreads and margins of the banking business Gross yield on interest-earning assets ... -

Page 118

Business review Average balance sheet and related interest Managed 2013 Average balance £m Interest £m Rate % Average balance £m Managed 2012* Interest £m Rate % Assets Loans and advances to banks Loans and advances to customers Debt securities Interest-earning assets Total interest-earning ... -

Page 119

Business review Managed 2011* Average balance £m Interest £m Rate % Assets Loans and advances to banks Loans and advances to customers Debt securities Interest-earning assets Total interest-earning assets Interest-earning assets Non-interest-earning assets Total assets Percentage of assets ... -

Page 120

Business review Average balance sheet and related interest continued Statutory 2013 Average balance £m Interest £m Rate % Average balance £m Statutory 2012 Interest £m Rate % Assets Loans and advances to banks Loans and advances to customers Debt securities Interest-earning assets Total ... -

Page 121

... Liabilities Deposits by banks Customer accounts: demand deposits Customer accounts: savings deposits - UK - Overseas - UK - Overseas - UK - Overseas Customer accounts: other time deposits - UK - Overseas Debt securities in issue Subordinated liabilities Internal funding of trading business Interest... -

Page 122

...deposits UK Overseas Customer accounts: other time deposits UK Overseas Debt securities in issue UK Overseas Subordinated liabilities UK Overseas Internal funding of trading business UK Overseas Total interest payable of the banking business UK Overseas 478 441 919 Movement in net interest income UK... -

Page 123

... UK Overseas Customer accounts: other time deposits UK Overseas Debt securities in issue UK Overseas Subordinated liabilities UK Overseas Internal funding of trading business UK Overseas Total interest payable of the banking business UK Overseas 1,271 1,055 2,326 Movement in net interest income UK... -

Page 124

Business review Non-interest income Managed (1) 2013 £m 2012* £m 2011* £m 2013 £m Statutory 2012 £m 2011 £m Fees and commissions receivable Fees and commissions payable Income from trading activities - excluding Asset Protection Scheme - Asset Protection Scheme Gain on redemption of own debt... -

Page 125

... the disposal of RBS Aviation Capital in June 2012, which resulted in lower rental income in Non-Core, partially offset by a lower fair value charge on the Asset Protection Scheme. The continuing strengthening of RBS's credit profile resulted in a £4,649 million accounting charge in relation to own... -

Page 126

Business review Operating expenses Managed (1) 2013 £m 2012* £m 2011* £m 2013 £m Statutory 2012* £m 2011* £m Staff costs Premises and equipment Other administrative expenses - Payment Protection Insurance costs - Interest Rate Hedging Products redress and related costs - regulatory and legal... -

Page 127

... current experience of Payment Protection Insurance complaints received, RBS increased its PPI provision by £1,110 million in 2012, bringing the cumulative charge taken to £2.2 billion, of which £1.3 billion in redress had been paid by 31 December 2012. On 31 January 2013, the Financial Services... -

Page 128

... restructuring of Markets and International Banking announced in January 2012. Accruals in relation to restructuring costs are set out below. At 1 January 2013 £m Currency translation adjustments £m Charge to income statement £m Utilised during the year £m At 31 December 2013 £m Staff costs... -

Page 129

Business review Impairment losses Managed (1) 2013 £m 2012 £m 2011 £m 2013 £m Statutory 2012 £m 2011 £m New impairment losses Less: recoveries of amounts previously written-off Charge to income statement Comprising: Loan impairment losses Securities - sovereign debt impairment and related ... -

Page 130

... value of deferred tax assets in Australia following the strategic changes to the Markets and International Banking businesses announced in January 2012, and the effect of the two reductions of 1% in the rate of UK corporation tax enacted in March 2012 and July 2012 on the net deferred tax balance... -

Page 131

...division UK Retail UK Corporate Wealth International Banking Ulster Bank US Retail & Commercial Retail & Commercial Markets Central items Core Non-Core Operating (loss)/profit - managed basis Own credit adjustments Payment Protection Insurance costs Interest Rate Hedging Products redress and related... -

Page 132

... 2012 £bn 3.95 3.06 3.23 1.73 1.87 3.03 2.96 0.60 1.89 2011 £bn Risk-weighted assets by division UK Retail UK Corporate Wealth International Banking Ulster Bank US Retail & Commercial Retail & Commercial Markets Other Core Non-Core Group before benefit of Asset Protection Scheme Benefit of Asset... -

Page 133

Business review Employee numbers at 31 December (full time equivalents rounded to the nearest hundred) 2013 2012 2011 UK Retail UK Corporate Wealth International Banking Ulster Bank US Retail & Commercial Retail & Commercial Markets Central items Core Non-Core Business Services Integration and ... -

Page 134

... losses Impairment losses Operating profit Analysis of income by product Personal advances Personal deposits Mortgages Cards Other Total income Analysis of impairments by sector Mortgages Personal Cards Total impairment losses Loan impairment charge as % of gross customer loans and advances... -

Page 135

Business review 2013 £bn 2012 £bn 2011 £bn Capital and balance sheet Loans and advances to customers (gross) - mortgages - personal - cards Loan impairment provisions Net loans and advances to customers Risk elements in lending Provision coverage (2) Customer deposits - current accounts - ... -

Page 136

... phase of the UK Government's Help To Buy scheme. Gross lending increased to £8.9 billion in H2 2013. Customer deposits increased by 7%, above the UK market average of 4% due to strong growth in both current accounts (13%) and instant access savings accounts (15%). Net interest income was broadly... -

Page 137

... income Direct expenses - staff - other Indirect expenses Profit before impairment losses Impairment losses Operating profit Analysis of income by business Corporate and commercial lending Asset and invoice finance Corporate deposits Other Total income Analysis of impairments by sector Financial... -

Page 138

Business review UK Corporate continued 2013 2012 2011 Performance ratios Return on equity (1) Net interest margin Cost:income ratio Capital and balance sheet Loans and advances to customers (gross) - financial institutions - hotels and restaurants - housebuilding and construction - manufacturing -... -

Page 139

... with UK Corporate's skills-based volunteering scheme, a programme offering all employees five days to volunteer with a charitable organisation, UK Corporate continued to deliver on its on-going commitment to communities. 2013 compared with 2012 The business delivered a return on equity of 11... -

Page 140

... 76% £bn Capital and balance sheet Loans and advances to customers (gross) - mortgages - personal - other Loan impairment provisions Net loans and advances to customers Risk elements in lending Provision coverage (2) Assets under management (excluding deposits) Customer deposits Loan:deposit ratio... -

Page 141

... in change programmes, including the development of new products and services capability and the implementation of RDR in the UK. Expenses also increased as a result of client redress following a past business review into the sale of the ALICO Enhanced Variable Rate Fund announced in November 2011... -

Page 142

...Banking Net interest income Non-interest income Total income Direct expenses - staff - other Indirect expenses Profit before impairment losses Impairment losses Operating profit Of which: Ongoing businesses Run-off businesses Analysis of income by product Cash management Trade finance Loan portfolio... -

Page 143

...debt financing, risk management and transaction services across its network. Business conditions remain challenging as themes of low interest rates and margin compression continue. International Banking remained focused on cost discipline throughout 2013 and continued to strengthen its balance sheet... -

Page 144

...'s credit rating downgrade and the Group technology incident in June 2012 outweighed economic pressures. This, coupled with the managed reduction in loans and advances to customers, improved the loan:deposit ratio to 91%. Bank deposits were down 51%, mainly as a result of lower short-term balances... -

Page 145

...Operating loss Analysis of income by business Corporate Retail Other Total income Analysis of impairments by sector Mortgages Commercial real estate - investment - development Other corporate Other lending Total impairment losses Of which RCR related (1) Loan impairment charge as % of gross customer... -

Page 146

Business review Ulster Bank continued 2013 £bn 2012 £bn 2011 £bn Capital and balance sheet Loans and advances to customers (gross) - mortgages - commercial real estate - investment - development - other corporate - other lending Loan impairment provisions Net loans and advances to customers ... -

Page 147

... for 2012 was driven by a combination of new defaulting customers and deteriorating security values. Risk elements in lending increased by £2 billion during the year reflecting continued difficult conditions in both the commercial and residential property sectors. The loan to deposit ratio improved... -

Page 148

... Operating profit Average exchange rate - US$/£ Analysis of income by product Mortgages and home equity Personal lending and cards Retail deposits Commercial lending Commercial deposits Other Total income Analysis of impairments by sector Residential mortgages Home equity Corporate and commercial... -

Page 149

Business review 2013 US$bn 2012 US$bn 2011 US$bn 2013 £bn 2012 £bn 2011 £bn Capital and balance sheet Loans and advances to customers (gross) - residential mortgages - home equity - corporate and commercial - other consumer Loan impairment provisions Net loans and advances to customers ... -

Page 150

... range of commercial banking operations in Chicago including Asset-Based Lending, Asset Finance, Equipment Leasing, Commercial Real Estate, Treasury Solutions, Capital Markets, Sponsor Finance, Franchise Finance and the majority of its corporate banking business. (2) Source: SNL Financial. Based on... -

Page 151

Business review 2013 compared with 2012 Operating profit of £647 million ($1,012 million) was down £107 million ($184 million), or 14%. The operating environment and market conditions remained challenging, with intense competition for loans. An extended period of low short-term rates limited net ... -

Page 152

... RCR and related strategy. (2) The ongoing businesses include the Rates, Currencies, Asset backed products and credit markets areas. (3) Divisional return on equity is based on divisional operating profit after tax divided by average notional equity (based on 10% of the monthly average of divisional... -

Page 153

... repos) Bank deposits (excluding repos) Risk-weighted assets - credit risk - non-counterparty - counterparty - market risk - operational risk Total risk-weighted assets Income statement (ongoing business) Total income Direct expenses Indirect expenses Impairment (losses)/recoveries Operating profit... -

Page 154

... balance sheet and risk resources deployed by the business. Credit Markets reflected the previous year's de-risking of credit trading and witnessed a modest reduction in Debt Capital Markets income, although the business executed a number of significant transactions and retained its leading position... -

Page 155

... not repeated. Offsetting these costs, profits on Group Treasury available-for-sale bond disposals totalled £880 million compared with £516 million in 2011, as active management of the liquid assets portfolio as well as favourable market conditions enabled the Group to crystallise gains on some... -

Page 156

...of (loss)/income by business Banking & portfolios International businesses Markets Total income Loss from trading activities Monoline exposures Credit derivative product companies Asset-backed products (2) Other credit exotics Equities Banking book hedges Other 2013 £m 2012 £m 2011 £m (61) 55... -

Page 157

... derivatives) Risk elements in lending (1) Provision coverage (2) Customer deposits (1) Risk-weighted assets - credit risk - non-counterparty - counterparty - market risk - operational risk Total risk-weighted assets Gross customer loans and advances Banking & portfolios International businesses... -

Page 158

...represents loan impairment provisions as a percentage of risk elements in lending. (3) Disposals of £0.8 billion have been signed as at 31 December 2013 but are pending completion (2012 and 2011 - £0.2 billion). 2013 £bn 2012 £bn 2011 £bn Commercial real estate third party assets UK (excluding... -

Page 159

... Corporate Ulster Bank Mortgages Commercial real estate - investment - development Other corporate Other EMEA Total Ulster Bank US Retail & Commercial Auto and consumer Cards SBO/home equity Residential mortgages Commercial real estate Commercial and other Total US Retail & Commercial International... -

Page 160

... UK Corporate Ulster Bank Commercial real estate - investment - development Other corporate Other EMEA Total Ulster Bank US Retail & Commercial Auto and consumer Cards SBO/home equity Residential mortgages Commercial real estate Commercial and other Total US Retail & Commercial Markets Manufacturing... -

Page 161

... income of £407 million was driven by a 31% fall in interest earning assets driven by run-off and disposals. Headcount declined by 1,700, or 55% to 1,400 of which 1,000 relates to operations in India and Romania, reflecting divestment activity and runoff. 2012 compared with 2011 Third party assets... -

Page 162

... progress of RCR, including funding and capital employed and released. Furthermore, a Board Oversight Committee ('BOC') has been set up reporting directly to the Group Board, to report on adherence to asset management principles and recommend changes to strategy where appropriate. The BOC comprises... -

Page 163

...£11 billion. Capital deductions comprised expected losses less impairment provisions (31 December 2013 - £1,774 million; 30 June 2013 - £6,047 million) and allocation of defined pension fund deficit (31 December 2013 - £58 million; 30 June 2013 - £38 million). Additional details are set out on... -

Page 164

Business review RBS Capital Resolution continued The impact of the revised strategy on key metrics of the Group are set out below. Group £bn RCR £bn Rest of the Group £bn Funded assets Non-Core Ulster Bank UK Corporate International Banking Markets Other divisions 28.0 28.0 105.0 48.5 212.8 317... -

Page 165

Business review Estimated funded assets (third party assets excluding derivatives or TPA) and RWAe of RCR Analysis of the funded assets and RWAe of RCR at 31 December 2013 and the related position at 30 June 2013 (the starting point for the identification of the portfolios of RCR), are set out ... -

Page 166

... agreements and stock lending Customer accounts Debt securities in issue Settlement balances Short positions Derivatives Accruals, deferred income and other liabilities Retirement benefit liabilities Deferred tax Insurance liabilities Subordinated liabilities Liabilities of disposal groups Total... -

Page 167

... within Markets and Group Treasury in holdings of UK and Eurozone government securities and financial institution bonds. Equity shares decreased by £6.4 billion, 42%, to £8.8 billion due to the targeted run-down of Markets' equities business. Movements in the value of derivative assets, down... -

Page 168

...Group's defined benefit pension schemes, primarily arising from significant reductions in the real discount rates in the Sterling, Euro and US dollar currency zones. These were partially offset by the £0.6 billion excess of employer contributions paid over the current year pension charge. Insurance... -

Page 169

...cash flows from operating activities Net cash flows from investing activities Net cash flows from financing activities Effects of exchange rate changes on cash and cash equivalents Net (decrease)/increase in cash and cash equivalents *Restated - see page 102. 2013 £m 2012* £m 2011* £m (30,631... -

Page 170

... regulatory purposes. 2013 £m 2012 £m 2011 £m 2010 £m 2009 £m Capital base Tier 1 capital Tier 2 capital Less: supervisory deductions Total regulatory capital Risk-weighted assets Credit risk - non-counterparty - counterparty Market risk Operational risk Asset Protection Scheme relief 291,100... -

Page 171

...items £m Managed £m Statutory £m Net interest income Non-interest income Total income Operating expenses Operating profit before impairment losses Impairment losses Operating loss Own credit adjustments Payment Protection Insurance costs Interest Rate Hedging Products redress and related costs... -

Page 172

... Operating profit/(loss) Own credit adjustments Payment Protection Insurance costs Interest Rate Hedging Products redress and related costs Regulatory and legal actions Integration and restructuring costs Gain on redemption of own debt Write-down of goodwill Asset Protection Scheme Amortisation... -

Page 173

... £m Managed £m Statutory £m Net interest income Non-interest income Total income Operating expenses Operating profit before impairment losses Impairment losses Operating profit/(loss) Own credit adjustments Payment Protection Insurance costs Sovereign debt impairment and related interest rate... -

Page 174

... tax Other financial assets Prepayments, accrued income and other assets Assets of disposal groups Total assets Liabilities Bank deposits Repos Deposits by banks Customer deposits Repos Customer accounts Debt securities in issue Settlement balances Short positions Derivatives Accruals, deferred... -

Page 175

Business review 2013 Balance sheet £m Disposal groups (1) £m Gross of disposal groups £m Balance sheet £m 2012 Disposal groups (2) £m Gross of disposal groups £m Balance sheet £m 2011 Disposal groups (3) £m Gross of disposal groups £m Selected financial data Gross loans and advances to ... -

Page 176

Business review Risk and balance sheet management Risk and balance sheet management 175 Risk governance 183 Risk appetite 192 Capital management 209 Liquidity and funding risk 227 Credit risk 268 Balance sheet analysis 318 Market risk 341 Country risk 354 Other risks 174 -

Page 177

Business review Risk and balance sheet management Risk governance 176 176 177 177 178 179 181 Governance structure Risk management Conduct and Regulatory Affairs Business model Risk events and lessons learned Top and emerging risk scenarios Stress testing 175 -

Page 178

.... The Group Chief Risk Officer reports directly to the Group Chief Executive and the Board Risk Committee, with a right of access to the Chairman of the Board Risk Committee. RBS Risk Management is designed to align as closely as possible with the customer-facing businesses and support functions... -

Page 179

... to interest rate and foreign exchange risk. Markets also helps customers structure securitisation transactions and issue debt. In addition, Ulster Bank and Citizens Bank, offer loan and investment products, as well as transactional services, to individuals and corporations. The customers of Ulster... -

Page 180

Business review Risk and balance sheet management Risk governance* continued Business model continued Over the last few years, the Group has either exited or sold a number of businesses in order to align its cost structure with its smaller scope and scale. In addition, it is reducing costs through ... -

Page 181

... in the Group. A rate setting review board was also created to oversee the submission process. For more information on LIBOR related settlements, refer to page 477. Payment Protection Insurance Since the judicial review decision in 2011, the Group has worked closely with both the Financial Conduct... -

Page 182

... of 2013, it was subject to shareholder litigation, securities related litigation, various class actions claims, including those related to LIBOR and foreign exchange trading, and mass consumer claims such as those related to Payment Protection Insurance and interest rate hedging products. This risk... -

Page 183

... to embed stress testing as a key risk management technique into mainstream risk reporting, capital planning and business processes at divisional, legal entity and Group levels. The Executive Risk Forum (refer to Risk governance on page 176 for further information) is the main body overseeing the... -

Page 184

... to senior management semi-annually. Once simply conducted principally to meet regulatory requirements, it is now an integral part of enterprise risk management and used to assess the impact of business decisions on the Group's capital position. As part of the financial planning and strategy cycle... -

Page 185

...Strategic risk objectives Risk appetite measures - Divisional risk appetite statements - Risk control frameworks and limits Culture, values and remuneration - Objectives for risk culture - Risk culture policies - Training - Challenge mechanisms - Risk-based key performance indicators - Risk coverage... -

Page 186

... commercial strategies with the most effective use of financial resources, such as capital, funding and risk capacity. Risk appetite provides a solid platform that allows the Group to focus on its key business strengths and competitive advantages over the long term. The Board Risk Committee reviews... -

Page 187

... customers, employees, investors and the general public) and is closely aligned with key risk policies and controls (e.g. the Group Policy Framework, conduct risk and reputational risk). Risk control frameworks and limits - Risk control frameworks set detailed tolerances and limits for material risk... -

Page 188

... risk and uses both absolute and relative risk measures. Risk culture policies The Group's values - of "serving customers well", "working together", "doing the right thing" and "thinking long term" - act as a clear starting point for a strong and effective risk culture. A wide range of communication... -

Page 189

... Equity Tier 1 ratio of c.11% by the end of 2015 and 12% or above by the end of 2016. The timely run-down of RCR and the successful divestment of Citizens are key to the achievement of the Group's capital plans. Refer to the Capital management section on pages 192 to 208 for further information... -

Page 190

... Basel models. Refer to the Credit risk and Balance sheet analysis sections on pages 227 to 317 for further information. Market risk The risk of loss arising from fluctuations in interest rates, credit spreads, foreign currency rates, equity prices, commodity prices and other risk-related factors... -

Page 191

...International Banking, Ulster Bank (Ireland), Group Centre (mainly Treasury), US Retail & Commercial and Non-Core. It has the potential to affect parts of the Group's credit portfolio that are directly or indirectly linked to the country in question. How the Group manages risk and the focus in 2013... -

Page 192

...be used for managing pension risk and the financial strategy implications of the pension schemes as well as reviewing fund performance. The Committee reports to the Group Asset and Liability Committee on the material pension schemes that the Group is obliged to support. In 2013, various pension risk... -

Page 193

.... In 2013, the environmental, social and ethical risk management function was set up to address the reputational risk associated with the clients the Group chooses to do business with. It sets policy and provides guidance to avoid reputational risk relating to business engagements and lending to... -

Page 194

Business review Risk and balance sheet management Capital management 193 Definition 193 2013 overview 193 Regulatory developments 193 Governance 194 Economic capital 195 Capital resources 200 Estimated leverage ratio 202 Risk-weighted assets 205 Reconciliation between accounting and regulatory ... -

Page 195

... change. CAST reports through GALCO and comprises senior representatives from Risk Management, Group Finance and Group Treasury. Target capital ratios are set and monitored by the PRA for the Group. Management of capital is achieved by supervision of forecast capital and RWA over a five year time... -

Page 196

... through both internally and externally defined stress testing to identify potential changes in capital ratios in a range of scenarios. Basel II requires RWAs to be calculated for credit, market and operational risk with various approaches available to banks, with differing levels of sophistication... -

Page 197

... set out below. Current rules Capital Core Tier 1 Core Tier 1 (excluding Asset Protection Scheme (APS) in 2011) Tier 1 Total RWAs by risk Credit risk - non-counterparty - counterparty Market risk Operational risk APS relief 291.1 22.3 30.3 41.8 385.5 - 385.5 Risk asset ratios Core Tier 1 Core Tier... -

Page 198

Business review Risk and balance sheet management Capital management* continued Capital resources continued Current capital resources and CRR capital estimate A reconciliation between capital as reported under the current basis (Basel 2.5), transitional basis (PRA) and full basis (final CRR) is set... -

Page 199

Business review Risk and balance sheet management 2013 Current basis (Basel 2.5) £m Transitional basis (PRA) £m Full basis (final CRR) £m Current basis (Basel 2.5) £m 2012 Transitional basis (draft CRR) £m Full basis (draft CRR) £m 2011 Current basis (Basel 2.5) £m Shareholders' equity (... -

Page 200

... ended 31 December 2013. Supervisory Core Tier 1 £m Other Tier 1 £m Tier 2 £m deductions £m Total £m At 1 January 2013 Attributable loss net of movements in fair value of own credit Share capital and reserve movements in respect of employee share schemes Ordinary shares issued Foreign exchange... -

Page 201

Business review Risk and balance sheet management The table below analyses the movement in CET1 and Tier 2 capital on a FLB3 basis during the year ended 31 December 2013. CET1 £m Tier 2 £m Total £m At 1 January 2013 Attributable loss net of movements in fair value of own credit Share capital ... -

Page 202

.... The estimated leverage ratio, based on the Basel Committee on Banking Supervision (BCBS) proposal issued in January 2014, is detailed below. 2013 2012 Leverage % Exposure £bn Tier 1 capital £bn Leverage % Estimated leverage ratio CRR basis: Transitional measure Full end point measure Basel III... -

Page 203

... review Risk and balance sheet management 2013 CRR Basel III basis £bn BCBS basis £bn CRR basis £bn basis £bn 2012 Basel III basis £bn BCBS basis £bn Exposure measure Cash and balances at central banks Debt securities Equity shares Derivatives Loans and advances to banks and customers... -

Page 204

Business review Risk and balance sheet management Capital management* continued Estimated leverage ratio continued Off-balance sheet items UK Retail £bn UK Corporate £bn International Banking (1) £bn US Retail & Commercial £bn Markets £bn Other £bn Total £bn 2013 Unconditionally ... -

Page 205

Business review Risk and balance sheet management The table below analyses RWA movements by division during the year. US R&C (1) £bn UK Retail UK Corporate Wealth £bn IB (1) Ulster Bank £bn £bn Markets £bn Other £bn Core £bn Non-Core £bn RFS MI £bn Total £bn Total RWAs At 1 ... -

Page 206

Business review Risk and balance sheet management Capital management* continued Risk-weighted assets continued FLB3 and Basel 2.5 The following tables set out RWAs under future and current rules. Estimated FLB3 £bn Basel 2.5 £bn 2013 UK Retail UK Corporate Wealth International Banking Ulster ... -

Page 207

... Accounting of insurance and associates/ Regulatory balance sheet other entities (1) other entities (2) consolidation £m £m £m £m Assets Cash and balances at central banks Loans and advances to banks Loans and advances to customers Debt securities Equity shares Settlement balances Derivatives... -

Page 208

... 2013 Balance Consolidation sheet differences (1) £bn £bn Regulatory consolidation £bn Total EAD £bn Cash and balances at central banks Reverse repurchase agreements and stock borrowing Loans and advances Debt securities Equity shares Settlement balances Derivatives Intangible assets... -

Page 209

Business review Risk and balance sheet management RWA density The table below analyses EAD, RWAs and related RWA density by sector cluster. EAD OffEAD post CRM (1) Non-CCR credit risk £m CCR (2) £m Total £m Drawn balance £m On-balance sheet EAD £m Undrawn Undrawn EAD £m £m Offbalance sheet ... -

Page 210

Business review Risk and balance sheet management Capital management* continued RWA density continued EAD EAD post CRM (1) 2012 Non-CCR £m CCR (2) £m Total £m Drawn balance £m Undrawn £m Offbalance sheet £m RWAs £m EAD post CRM RWA density (3) % Sovereign Central banks Central government ... -

Page 211

... 217 - Wholesale funding 218 - Total funding by currency 218 - Notes issued 219 - Deposits and repos 219 - Firm financing 220 - Divisional loan:deposit ratios and funding surplus 220 - Maturity analysis 223 - Encumbrance 226 - Summary of assets available as collateral (on and off-balance sheet) 209 -

Page 212

... levels. In setting risk limits the Board takes into account the nature of the Group's various activities, the Group's overall risk appetite, market best practice and regulatory compliance. The Group Asset and Liability Management Committee (GALCO) sets and reviews the liquidity risk management... -

Page 213

...including the CFO and Group Treasurer. Liquidity risks are reviewed daily at a significant legal entity level and performance reported at least monthly to legal entity, divisional and Group Asset and Liability Management Committees. Any breach of internal metric limits will set in motion a series of... -

Page 214