RBS 2013 Annual Report Download - page 285

Download and view the complete annual report

Please find page 285 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

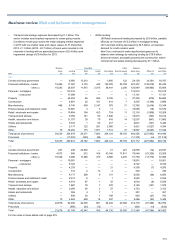

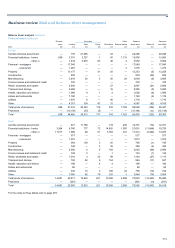

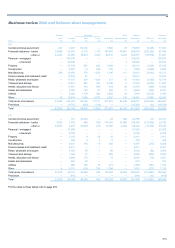

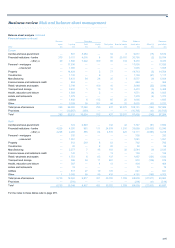

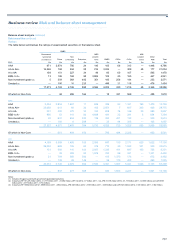

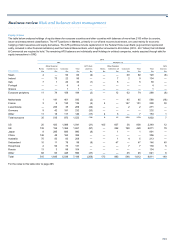

Business review Risk and balance sheet management

283

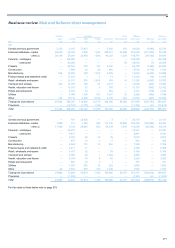

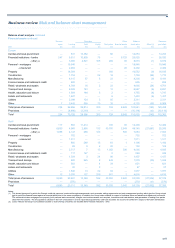

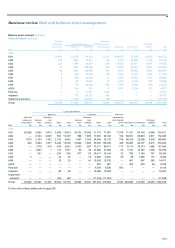

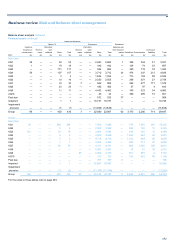

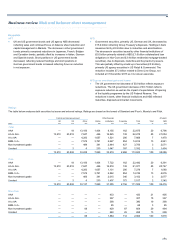

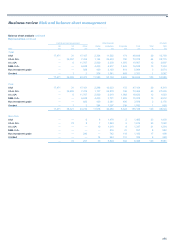

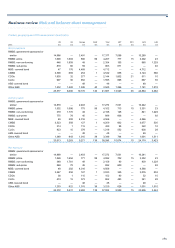

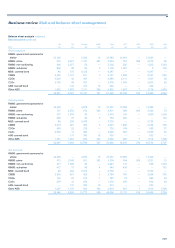

Cash and Settlement

balances at Loans and advances balances and other Contingent

central banks Banks (1) Customers financial assets Derivatives Commitments liabilities Total

2011 (2) £m £m £m £m £m £m £m £m

Non-Core

A

Q1 58 590 18,733 118 3,876 6,136 827 30,338

A

Q2 — 4 1,652 2677 865 32 3,232

A

Q3 167 14 3,471 —467 1,152 73 5,344

A

Q4 1 55 6,616 1946 1,263 192 9,074

A

Q5 — 5 7,145 —1,429 1,367 209 10,155

A

Q6 — 48 6,416 —234 1,035 28 7,761

A

Q7 — — 4,265 —1,597 1,649 88 7,599

A

Q8 — 10 2,014 —586 91 40 2,741

A

Q9 — — 4,491 48 558 517 45 5,659

A

Q10 — — 306 —708 1,080 41 2,135

Past due — — 1,544 — — — — 1,544

Impaired — 1 23,464 1 — — — 23,466

Impairment provision — (1) (11,486) (1) — — — (11,488)

Group 226 726 68,631 169 11,078 15,155 1,575 97,560

Notes:

(1) Excludes items in the course of collection from other banks of £1,454 million (2012 - £1,531 million; 2011 - £1,470 million).

(2) Excludes balances in relation to Direct Line Group (loans to banks: 2012 - £2,036 million; 2011 - £2,579 million and loans to customers: 2012 - £881 million; 2011 - £893 million).

(3) Exposures are allocated to asset quality bands on the basis of statistically driven models which produce an estimate of default rate. The variables included in the models vary by product and

geography. For portfolios secured on residential property these models typically include measures of delinquency and loan-to-value as well as other differentiating characteristics such as bureau

score, product features or associated account performance information.

Key points

• Underlying the balance sheet reduction in the year the overall asset

quality in the upper bands (AQ1-AQ5) remained broadly similar.

• Within cash and balances at central banks there has been an

increase in AQ1 of £2.3 billion due to additional funds deposited with

the Bank of England and the Federal Reserve. Additionally,

increases of £1.1 billion in AQ3 and AQ4 are due to deposits with

other central banks as part of the Group’s overall liquidity

management.

• Reverse repo balances decreased £28.4 billion due to reduced

trading volumes within Markets. However, AQ2 and AQ4-AQ7 have

increased £7.2 billion in bank reverse repurchase agreements as a

small number of counterparties moved bands, in addition to the

implementation of a strategy to develop relationships with newer,

lower-rated counterparties.

• Derivatives decreased across all asset quality bands reflecting risk

reduction within Markets and upwards shifts in major interest rate

yield curves.

• Core customer lending in AQ1-AQ3 increased to 22% from 18% at

31 December 2012 as recalibration of the UK Retail models using

updated data trends from the last three years resulted in £9.8 billion

moving from AQ5 to higher bands. In addition, mid corporate model

updates in UK Corporate and data quality improvements in Wealth

also led to improving trends.

• Core past due loans to customers decreased £1.2 billion, with a

reduction in Ulster Bank (£0.8 billion) and US Retail and Commercial

(£1.2 billion) being offset by increases in UK Retail (£1.2 billion) as

balances transferred from the impaired book.

• Impairment provisions increased £4.0 billion, mainly due to RCR and

related change in strategy (£4.5 billion) partly offset by a decrease in

UK Retail (£0.5 billion).