RBS 2013 Annual Report Download - page 246

Download and view the complete annual report

Please find page 246 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

244

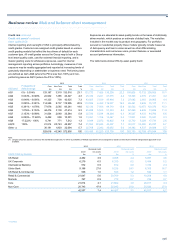

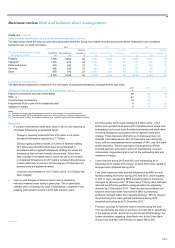

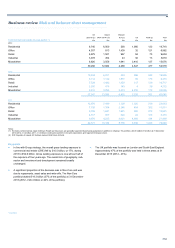

Credit risk continued

Early problem identification and problem debt management continued

The table below shows the value of loans (excluding loans where the Group has initiated recovery procedures) where forbearance was completed

during the year, by sector and types.

2013 2012 2011

Provision Provision Provision

Performing Non-performing coverage (1) Performing Non-performing Coverage (1) Performing Non-performing Coverage (1)

Wholesale forbearance during

the year by sector £m £m % £m £m % £m £m %

Property 1,759 4,802 60 3,365 3,899 16 2,166 3,215 25

Transport 1,016 229 34 1,174 130 23 771 670 10

Retail and leisure 455 390 37 732 113 34 331 433 10

Services 405 234 77 324 51 30 177 94 3

Other 670 510 27 1,575 550 40 773 731 47

4,305 6,165 55 7,170 4,743 20 4,218 5,143 25

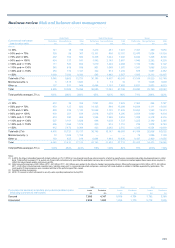

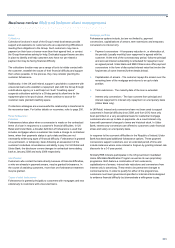

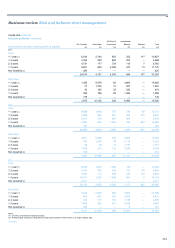

Forbearance arrangements

The table below analyses the incidence of the main types of wholesale forbearance arrangements by loan value.

2013 2012 2011

Wholesale forbearance during the year by arrangement type (2) % % %

Payment concessions and loan rescheduling 78 49 92

Other (3) 31 14 9

Covenant-only concessions 16 30 —

Forgiveness of all or part of the outstanding debt 9 21 33

Variation in margin 2 6 12

Notes:

(1) Provision coverage reflects impairment provision as a percentage of non-performing loans.

(2) The total exceeds 100% as an individual case can involve more than one type of arrangement.

(3) The main types of ‘other’ concessions include formal ‘standstill’ agreements and release of security.

Key points

• A number of refinements have been made in 2013 to the reporting of

wholesale forbearance as explained below:

° Change in reporting thresholds from £10 million to £3 million,

increased forbearance reported by £1.7 billion.

° During ongoing portfolio reviews, a number of facilities totalling

£2.3 billion were identified which were being managed in

accordance with an agreed forbearance strategy but where the

forbearance had not been formally documented. These have

been included in the tables above, which has led to an increase

in completed forbearance for 2013 and a corresponding decrease

in loans which are “in process” for the purpose of forbearance (in

process loans are explained below).

° Covenant only forbearance of £1.7 billion (2012 - £3.5 billion) has

been included.

• Year-on-year analysis of forborne loans may be skewed by

individual material cases during a given year. This is particularly

relevant when comparing the value of forbearance completed in the

property and transport sectors in 2013 with previous years.

*unaudited

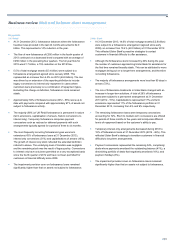

• At 31 December 2013, loans totalling £9.4 billion (2012 - £13.7

billion) were granted credit approval for forbearance but where such

forbearance had not yet been formally documented and which were

not being managed in accordance with an agreed forbearance

strategy. These loans are referred to as in process and are not

included in the tables above. 84% of these were non-performing

loans, with an associated provision coverage of 44%, and 16% were

performing loans. The principal types of arrangements offered

included payment concessions and loan rescheduling, covenant

concessions, forgiveness of all or part of the outstanding debt and

variations in margin.

• Loans forborne during 2012 and 2013 and outstanding at 31

December 2013 totalled £18.4 billion, of which £8.0 billion related to

arrangements completed during 2012.

• Core bank customers were granted forbearance by GRG on loan

facilities totalling £6.9 billion during 2012 and 2013, which equates

to 23% of loans managed by GRG (excluding loans to customers

managed by recovery units). Of these loans, 15% by value had been

returned to performing portfolios managed within the originating

divisions by 31 December 2013. There are also loans that are not

forborne which have been returned from GRG to performing

portfolios managed within the originating divisions. 79% by value of

the performing Core loans granted forbearance during 2012

remained performing as at 31 December 2013.*

• Provision coverage for forborne loans increased during the year.

This was primarily the result of provisions in Ulster Bank, specifically

in the property sector, and driven by the Group’s RCR strategy. For

further information regarding Ulster Bank refer to the Ulster Bank

Group (Core and Non-Core) section on pages 265 to 267.