RBS 2013 Annual Report Download - page 333

Download and view the complete annual report

Please find page 333 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

331

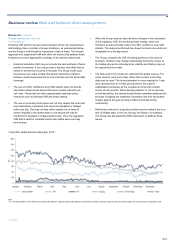

VaR back-testing*

For the Group’s trading book, a green model status was maintained

throughout 2013. For details of back-testing results for regulatory VaR,

refer to the table on page 327.

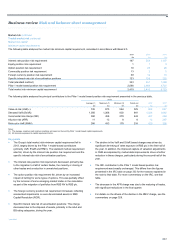

Regulatory SVaR*

The Group’s SVaR model has also been approved by the PRA for use in

the capital requirement calculation. The regulatory SVaR differs from

internal SVaR as it covers only regulator-approved products, locations

and legal entities.

Risks not in VaR (RNIVs)*

As discussed earlier, the Group has an established RNIV framework that

ensures that the risks not captured in VaR are adequately covered by its

capital.

The RNIV framework does not include tail event risks; these risks are

covered indirectly by the regulatory multiplier applied to VaR and directly

by relevant charges, e.g. IRC, APR and gap risk discussed below.

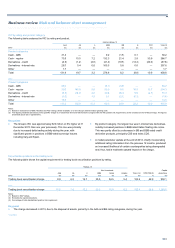

Gap risk*

Certain traded products are structured with buffers so that losses below a

certain level are borne by the Group’s counterparties. These products

may, however, exhibit large sudden market movements in excess of their

buffer, which may result in losses for the Group. The VaR model does not

fully capture the risk to the Group presented by these products. The gap

risk model takes into account the liquidity of the products and the likely

effectiveness of the buffer and produces an additional capital requirement

for the relevant products.

This risk is concentrated in the equities business in Markets. Markets’

exposure to gap risk was not material in 2013 as the portfolios

considered under this framework have been significantly reduced.

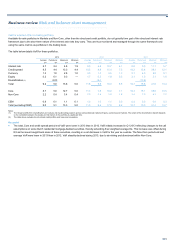

Incremental risk charge (IRC)*

The IRC model aims to quantify the impact of defaults and rating changes

on the market value of bonds, credit derivatives and other related

positions held in the trading book. It also captures basis risks between

different instruments, different product maturities and different but related

reference entities. Like the internal ratings-based approach for credit risk,

it is calculated over a one-year holding period at a 99.9% confidence

level.

*unaudited

The multivariate behaviour of positions is modelled via the relevant

reference entities using a single-factor model (Gaussian Copula), which

allows a more efficient calculation of the charge using numerical

integration.

The model is mainly driven by three-month transition, default and

correlation parameters. The portfolio impact of correlated defaults and

rating changes is assessed with reference to the resulting change in the

market value of positions, which is determined using stressed recovery

rates and modelled credit spread changes. Individual instrument

revaluation vectors are used to capture non-linear behaviour.

The model has different parameters for sovereign and corporate

exposures. The model reflects the overall liquidity of each position

referencing an entity, arising from product type, product maturity and

product concentration characteristics.

A constant level of risk is assumed and achieved by replacing positions

that default or migrate in one period with equivalent positions. The

average liquidity horizon at the year end was 3.7 months (2012 - 4.6

months).

All price risk (APR)*

The APR model determines the capital that should be held against all

material price risks, including those arising from defaults and credit rating

changes affecting securities in the hedged portfolio, using a 99.9%

confidence level over a one year time horizon.

This model is applied to the correlation trading portfolio subject to certain

eligibility criteria (principally that the underlying names be liquid corporate

CDS positions).

The most significant risks are credit spread risk, credit (base) correlation

risk, index basis risk, default risk and recovery rate risk. In addition,

losses due to both hedging costs and hedge slippage are modelled. The

overall APR capital charge is floored at 8% of the corresponding standard

rules charge for the same portfolio.

RBS no longer has market risk exposure to corporate CDOs in the

trading book. It has residual exposure to nth-to-default basket swaps,

many of which have matured. As a consequence, the APR charge for

RBS is small.