RBS 2013 Annual Report Download - page 336

Download and view the complete annual report

Please find page 336 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

334

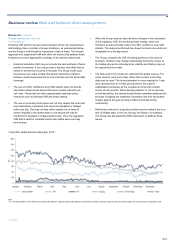

Market risk continued

Non-traded market risk

Risk management

The governance framework, risk management principles and appetite

and limit framework applicable to the Group’s management of market risk

are covered by the discussion on pages 176. More specific information

on the Group’s management of non-traded market risk is provided below.

The Group manages non-traded market risk, separately for the three key

categories: non-traded interest rate risk; non-traded foreign exchange

risk; and non-traded equity risk.

Non-traded market risk positions are reported on a regular basis to

divisional Asset and Liability Management Committees (ALCOs) and

monthly to the Group Balance Sheet Management Committee (BSMCo),

Group Asset and Liability Committee (GALCO) and the Group Board,

with the exception of equity positions, which are reported quarterly to

GALCO.

Interest rate risk

Non-traded interest rate risk (NTIRR) factors are grouped into the

following categories:

• Repricing risk, which arises when asset and liability positions either

mature (in the case of fixed-rate positions) or their interest rates

reset (in the case of floating-rate positions) at different dates. These

mismatches may give rise to net interest income and economic

value volatility as interest rates vary.

• Yield curve risk, which arises from unanticipated changes in the

shape of the yield curve, such that rates at different maturity points

may move differently. Such movements may give rise to interest

income and economic value volatility.

• The two risk factors above incorporate the duration risk arising from

the reinvestment of maturing swaps hedging the Group’s net free

reserves (or net exposure to equity and other low fixed-rate or non-

interest-bearing liability balances including, but not limited to, current

accounts).

• Basis risk, which arises when related instruments with the same

tenor are valued using different reference yield curves. Changes in

the spread between the different reference curves can result in

unexpected changes in the valuation of or income difference

between assets, liabilities or derivative instruments. This occurs, for

example, in the Group's retail and commercial portfolios, when

products valued on the basis of the Bank of England base rate are

funded with LIBOR-linked instruments.

• Optionality risk, which arises when customers have the right to

terminate, prepay or otherwise alter a transaction without penalty,

resulting in a change in the timing or magnitude of the cash flows of

an asset, liability or off-balance sheet instrument. This risk primarily

arises in the US mortgage business in Citizens Financial Group

where long-term fixed-rate loans are the norm and prepayment

penalties are rare.

Due to the long-term nature of many non-trading book portfolios and their

varied interest rate repricing characteristics and maturities, it is likely that

net interest income will vary from period to period, even if interest rates

remain the same. New business originated in any period will alter the

interest rate sensitivity of the Group if the resulting portfolio differs from

portfolios originated in prior periods, depending on the extent to which

exposure has been hedged.

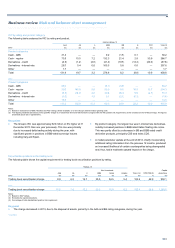

The Group’s policy is to manage the interest rate sensitivity within risk

limits that are approved by the ERF and endorsed by GALCO before

being cascaded to divisions through divisional ALCOs. These include, in

particular, interest rate sensitivity and VaR limits.

In order to manage exposures within these limits, the Group aggregates

its interest rate positions and hedges them externally using cash and

derivatives - primarily interest rate swaps.

This task is primarily carried out by Group Treasury, to which all divisions

except US Retail & Commercial and Markets transfer most of their

NTIRR. On a monthly basis, the Group’s main exposures and limit

utilisations are reported to the BSMCo, GALCO and the Group Board.

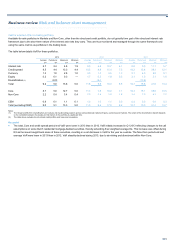

Foreign exchange risk

The Group’s only material non-traded open currency positions are the

structural foreign exchange exposures arising from its investments in

foreign subsidiaries and associates and their related currency funding.

These exposures are assessed and managed by Group Treasury under

delegated authority from GALCO. Group Treasury seeks to limit the

potential volatility impact on the Group’s Core Tier 1 ratio from exchange

rate movements to pre-defined risk appetite levels set by GALCO. The

sensitivity of the Group’s Core Tier 1 capital to exchange rates is updated

and reported to GALCO quarterly.

Foreign exchange exposures arising from customer transactions or profit

and losses are sold down by divisions and businesses on a regular basis

in line with Group policy.

Equity risk

Non-traded equity risk is the potential variation in the Group’s income and

reserves arising from changes in non-trading book equity valuations. Any

such risk is identified prior to any investments and then mitigated through

a framework of controls.

Investments, acquisitions or disposals of a strategic nature are referred to

the Group Acquisitions and Disposals Committee (ADCo). Once

approved by ADCo for execution, such transactions are referred for

approval to the Group Board, Group Executive Committee (ExCo), Group

Finance Director or as otherwise required. Decisions to acquire or hold

equity positions in the non-trading book that are not of a strategic nature,

such as customer restructurings, are taken by authorised persons with

delegated authority under the Group credit approval framework.

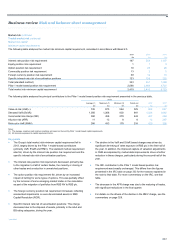

Risk measurement

Interest rate risk

NTIRR can be measured from either an economic value-based or

earnings-based perspective (or both). Value-based approaches measure

the change in value of the balance sheet assets and liabilities over a

longer timeframe, including all cash flows. Earnings-based approaches

measure the potential short-term (generally one year) impact on the

income statement of charges in interest rates.