RBS 2013 Annual Report Download - page 147

Download and view the complete annual report

Please find page 147 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review

145

Simplifying Banking

Ulster Bank delivered a number of improvements for personal and

business customers in 2013:

• The launch of initiatives such as “Get Cash”, “Pay Your Contacts”

and “Emergency Cash” provided a new range of simple and

convenient services for customers to access their cash and make

payments online and via mobile.

• Further development of online and mobile banking for business

customers focused on providing an efficient and effective day-to-day

banking service. Enhancements during 2013 included a speedy and

simplified account application process; registration for Anytime

Banking via telephone; ability to manage personal and business

accounts together and access to extended transaction history.

• The efficiency and effectiveness of Ulster Bank’s digital offering was

evidenced by a 55% increase in mobile app registrations and more

than 100 million transactions were carried out via digital channels

during 2013. Over 315,000 customers regularly use mobile app

banking services and 640,000 customers make regular use of online

Anytime banking services.

Supporting Enterprise and the Community:

• Supporting entrepreneurship and the growth of small businesses in

the local community is a long term commitment of Ulster Bank.

Highlights in 2013 included:

• The Community Impact Fund and Business Woman Can initiative

which facilitated women in local communities to set up their own

business. The bank also supported a number of projects in schools

across the island of Ireland through its MoneySense programme.

• Ulster Bank’s dedicated SME teams offer professional support and a

range of products to help customers meet their banking challenges

and grow their business. The agri–specialist team has introduced a

number of initiatives during 2013 to support the farming sector.

• The ‘One Week in June’ initiative raised £430,000 for a number of

Irish charities through a series of fundraising events involving both

customers and staff.

• In partnership with Concern Worldwide and Disasters Emergency

Committee, Ulster Bank ATMs, branches and online banking

facilitated donations to the Philippines Typhoon emergency appeals.

Helping Customers out of Financial Difficulty:

• Ulster Bank is committed to working with all customers in financial

difficulty to find a solution. The Bank continued to invest in its

Problem Debt Management Unit and further developed a range of

solutions to make it easier for customers to enter into arrangements.

As a consequence, the number of mortgage customers in arrears of

90 days or more has decreased every month since March 2013.

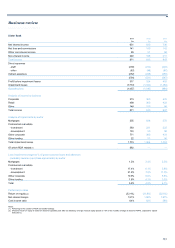

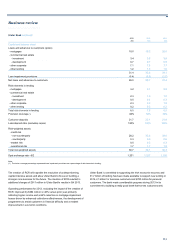

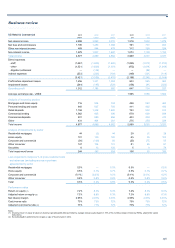

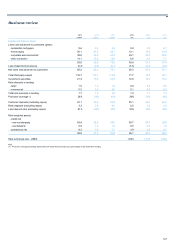

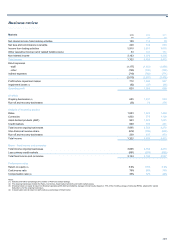

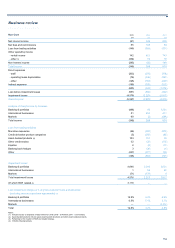

2013 compared with 2012

Excluding the impact of the creation of RCR, operating result improved by

£494 million or 48% primarily due to a higher income and lower

impairment losses on the mortgage portfolio.

Total income increased by £26 million or 3% to £871 million primarily

reflecting hedging gains on the mortgage portfolio. Net interest margin for

2013 increased by 3 basis points to 1.91% although net interest income

was £18 million lower at £631 million, largely driven by lower interest-

earning assets and a higher cost of funding.

Total expenses increased by £33 million or 6% to £554 million driven by

the costs of mandatory change programmes such as the Single Euro

Payment Area, £18 million, an investment of £10 million in programmes

to support customers in financial difficulty and an accelerated

depreciation charge of £12 million.

Impairment losses, excluding the impact of RCR, were £482 million, 35%

lower. This was predominantly due to a sharp reduction in losses on the

mortgage portfolio which reduced by £411 million or 64% due to a decline

in arrears levels driven by an improved collections performance and the

development of programmes to assist customers in financial difficulty,

coupled with stabilising residential property prices.

The loan:deposit ratio reduced from 130% to 120% during 2013 reflecting

continued customer deleveraging and low levels of demand for new

lending. Retail and SME deposit balances increased by 2% during 2013,

offset by a reduction in wholesale customer balances, resulting in a 2%

decline in total deposit balances.

Risk-weighted assets decreased by 15% reflecting a smaller performing

loan book and stabilising credit metrics.

2012 compared with 2011

Operating loss increased by £56 million primarily reflecting a reduction in

income driven by lower interest earning asset volumes.

Total expenses fell by £26 million, reflecting the benefits of cost saving

initiatives.

Impairment losses remained elevated, as weak underlying credit metrics

prevailed. Falling asset values throughout most of 2012 and high levels of

unemployment coupled with weak domestic demand continued to

depress the property market. The impairment charge for 2012 was driven

by a combination of new defaulting customers and deteriorating security

values. Risk elements in lending increased by £2 billion during the year

reflecting continued difficult conditions in both the commercial and

residential property sectors.

The loan to deposit ratio improved from 143% to 130%, driven by a

combination of deposit growth and a decrease in the loan book. At

constant currency, the loan book decreased by 2% as a result of natural

amortisation and limited new lending due to low levels of market demand.

Retail and SME deposits increased by 8%; however, this was partly offset

by outflows of wholesale balances driven by market volatility and the

impact of a rating downgrade in the second half of 2011.