RBS 2013 Annual Report Download - page 233

Download and view the complete annual report

Please find page 233 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

231

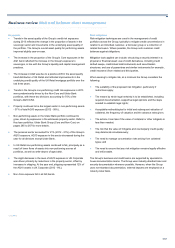

Loss given default (LGD)

LGD models estimate the amount that cannot be recovered in the event

of customer default. When estimating LGD, the Group’s models assess

both borrower and facility characteristics, as well as various credit risk

mitigants. The cost of collections and a time discount factor for the delay

in cash recovery are also incorporated.

Changes to credit models

The Group reviews and updates models on an ongoing basis, reflecting

more recent data, changes to products and portfolios, and updated

regulatory requirements. Extensive changes were made to wholesale

models in 2012 and 2013. This process continues with further changes,

notably in banks and corporate exposure classes, planned for 2014.

As in 2012, the impact of the model changes implemented in 2013 largely

affected the lower risk segments of the Group’s portfolios, mostly to

customers bearing the equivalent of investment-grade ratings.

Model changes affect year-on-year comparisons of risk measures in

certain disclosures. Where meaningful, the Group in its commentary has

differentiated between instances where movements in risk measures

reflect the impact of model changes, and those that reflect movements in

the size of underlying credit portfolios or their credit quality.

Economic capital

The credit economic capital model is an extensive framework that allows

for the calculation of portfolio credit loss distributions and associated

metrics over a given risk horizon for a variety of business purposes.

The model takes into account migration risk (risk that credit assets will

deteriorate in credit quality across multiple years), factor correlation

(the assumption that groups of obligors share a common factor) and

contagion risk (for example, the risk that the weakening of the sovereign’s

creditworthiness has a significant impact on the creditworthiness of a

business operating in that country).

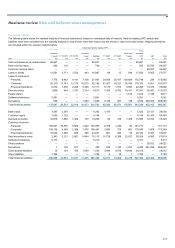

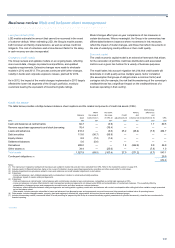

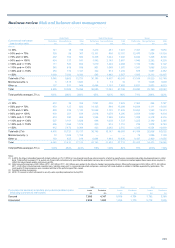

Credit risk assets*

The table below provides a bridge between balance sheet captions and the related components of credit risk assets (CRA).

Methodology

Within Not within Netting differences

Balance the scope of the scope Credit and and

sheet market risk (1) of CRA (2) adjustments (3) collateral (4) reclassifications (5) CRA

2013 £bn £bn £bn £bn £bn £bn £bn

Cash and balances at central banks 82.7 — (3.9) — — 1.7 80.5

Reverse repurchase agreements and stock borrowing 76.4 — (76.4) — — — —

Loans and advances 418.4 — (3.0) 25.2 (28.4) (7.5) 404.7

Debt securities 113.6 (56.7) (56.9) — — — —

Equity shares 8.8 (7.2) (1.6) — — — —

Settlement balances 5.6 (5.6) — — — — —

Derivatives 288.0 — — 1.8 (242.8) 9.9 56.9

Other assets (6) 34.4 — (25.6) — — (7.8) 1.0

Total assets 1,027.9 (69.5) (167.4) 27.0 (271.2) (3.7) 543.1

Contingent obligations (7) 29.9

573.0

Notes:

(1) The exposures in regulatory trading book businesses are subject to market risk and are hence excluded from CRA. Refer to the market risk section on page 318.

(2) Includes cash in ATMs and branches, items in the course of collection, reverse repurchase agreements, securities and other assets (refer to note below).

(3) Includes impairment loss provisions related to loans and advances and credit valuation adjustment on derivatives.

(4) Comprises:

- Loans and advances: cash collateral pledged with counterparties in relation to net derivative liability positions.

- Derivatives: impact of master netting arrangements.

(5) Comprises:

- Cash and balances at central banks: notice balances with central banks included in loans and advances, reclassified as central bank exposure in CRA.

- Loans and advances: includes offset related to cash management pooling arrangements not allowed under IFRS and reclassification of central bank balances. This is partially offset by

reclassification of disposal groups and prepayments, accrued income and other assets as customer balances.

- Derivatives: reflects difference between netting arrangements and netting within regulatory model sets, and balances with central counterparties after netting but before variation margin presented

net on the balance sheet.

- Other assets: includes amounts reclassified to loans and advances from disposal groups and prepayments, accrued income and other assets and residual value of operating leases.

(6) Other assets: includes intangible assets, property, plant and equipment, deferred tax, prepayments and accrued income and assets of disposal groups.

(7) Includes documentary credits (commercial letters of credit providing for payment by the Group to a named beneficiary against presentation of specified documents), classified as commitments for

financial reporting.

*unaudited