RBS 2013 Annual Report Download - page 215

Download and view the complete annual report

Please find page 215 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

213

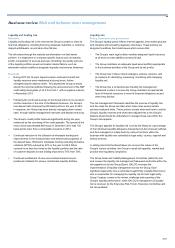

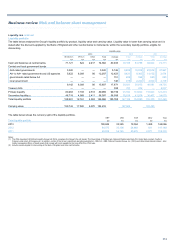

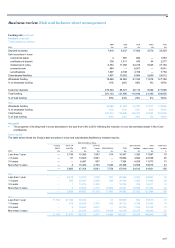

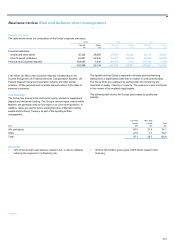

Liquidity reserves

Liquidity risks are mitigated by the Group’s centrally managed liquidity

portfolio. The size of the portfolio is determined under the Group’s

liquidity risk management framework with reference to the Group’s risk

appetite.

The majority of the portfolio is centrally managed by Group Treasury,

ring-fenced from the Markets trading book, and is the ultimate

responsibility of the Group Treasurer. This portfolio is held in the PRA

regulated UK Defined Liquidity Group (UK DLG) comprising the Group’s

five UK banks: The Royal Bank of Scotland plc, National Westminster

Bank Plc, Ulster Bank Limited, Coutts & Company and Adam &

Company.

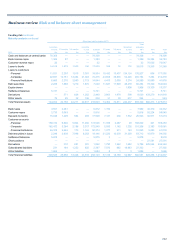

Certain of the Group's significant operating subsidiaries - RBS N.V., RBS

Citizens Financial Group, Inc. and Ulster Bank Ireland Limited - hold

locally managed portfolios of liquid assets that comply with local

regulations but differ from PRA rules. These portfolios are the

responsibility of the local Treasurer who reports to the Group Treasurer.

The UK DLG liquidity portfolio accounted for c.88% of the Group’s total

liquidity portfolio, this portion is available to meet liquidity needs as they

arise across the Group. The remaining liquidity reserves are held locally

within non-UK bank subsidiaries, the majority of this portion is restricted

by regulatory requirements and therefore assumed to be restricted and

only be available for use locally.

Separately from the liquidity portfolio, the Group holds high quality assets

to meet payment systems collateral requirements, these assets are not

freely available to other areas of the Group.

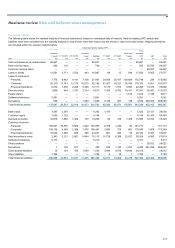

The Group categorises its liquidity portfolio, including its locally managed

liquidity portfolios, into primary and secondary liquid assets.

Primary liquid assets generally comprise eligible liquid assets, such as

cash and balances at central banks, treasury bills and other high quality

government and US agency bonds.

Secondary liquid assets comprise other assets that are eligible as

collateral for local central bank liquidity facilities but do not meet the core

local regulatory definition. These assets include own-issued

securitisations or whole loans that are retained on balance sheet and pre-

positioned with a central bank so that they may be converted into

additional sources of liquidity at very short notice.

The composition of the liquidity portfolio is influenced by quality of

counterparty, maturity mix and currency mix. The PRA rules dictate

certain minimum quality standards for the UK DLG liquidity portfolio. The

liquidity value of the portfolio is determined with reference to current

market prices and the haircuts necessary to generate cash from the

asset.

The Group in consultation with the PRA and subject to the requirements

of the PRA’s ILG can change the composition of its liquidity portfolio. The

change in composition may relate to market specific factors, changes in

internal liquidity risk mix or regulatory guidance.

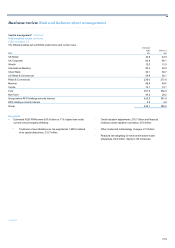

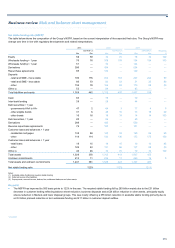

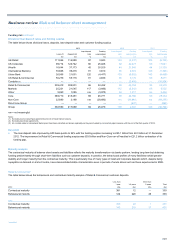

Liquidity metrics*

The table below sets out the key liquidity and related metrics monitored by the Group.

2013 2012

% %

Stressed outflow coverage (1) 145 128

Liquidity coverage ratio (LCR) (2) 102 >100

Net stable funding ratio (NSFR) (2) 122 117

Notes:

(1) The Group’s liquidity risk appetite is based on the internal Individual Liquidity Adequacy Assessment which is measured by reference to the liquidity portfolio as a percentage of stressed outflows

under the worst of three severe stress scenarios of a market-wide stress, an idiosyncratic stress and a combination of both. Liquidity risk adequacy is determined by surplus of liquid assets over three

months stressed outflows under the worst case stresses. This assessment is performed in accordance with PRA guidance.

(2) In January 2013, the Basel Committee on Banking Supervision issued its revised draft guidance for calculating LCR which is currently expected to come into effect from January 2015 on a phased

basis. Pending the finalisation of the technical standards, the Group monitors the LCR and NSFR based on its interpretations of the expected final rules.

*unaudited