RBS 2013 Annual Report Download - page 212

Download and view the complete annual report

Please find page 212 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

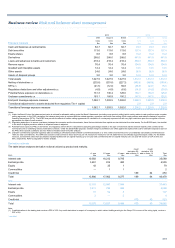

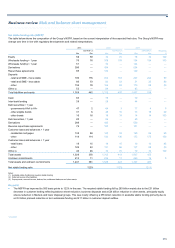

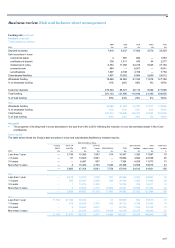

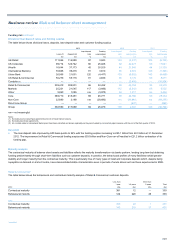

Business review Risk and balance sheet management

210

Liquidity and funding risk

Definition

Liquidity and funding risk is the risk that the Group is unable to meet its

financial obligations, including financing wholesale maturities or customer

deposit withdrawals, as and when they fall due.

The risk arises through the maturity transformation role that banks

perform. It is dependent on company specific factors such as maturity

profile, composition of sources and uses of funding, the quality and size

of the liquidity portfolio as well as broader market factors, such as

wholesale market conditions alongside depositor and investor behaviour.

Overview

• During 2013 the Group’s deposit surplus continued to build and

liquidity reserves were maintained at strong levels, further

strengthening the balance sheet. This allowed the Group to easily

absorb the minimal outflows following the announcement of the S&P

credit rating downgrade (A-/A-2 from A/A-1, with a negative outlook)

in November 2013.

• Following the continued success of the Group’s Non-Core run-down

and the reduction in the size of the Markets business, the Group’s

loan:deposit ratio improved by 600 basis points in the year to 94%.

In response, the Group has been actively managing down excess

cash, through liability management exercises and deposit re-pricing.

• The Group’s credit profile improved significantly during the year,

evidenced by the narrowing of the credit spreads. The spread of the

most recent subordinated debt issue in December 2013 was 125

basis points lower than a comparable issuance in 2012.

• Continued reduction in the utilisation of wholesale funding and

improvements in the characteristics and behavioural properties of

the deposit base. Short-term wholesale funding excluding derivative

collateral (STWF) reduced by 22% in the year to £32.4 billion,

covered more than four times by the liquidity portfolio and the ratio

of customer deposits to total funding improved to 75% from 70%.

• Continued enablement of new unencumbered assets as pre-

positioned collateral for various central bank liquidity facilities.

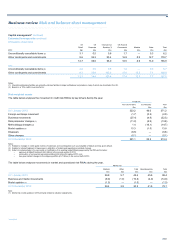

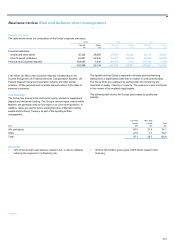

Liquidity risk

Policy, framework and governance

The Group’s liquidity policy reflects internal appetite, best market practice

and complies with prevailing regulatory structures. These policies are

designed to address four broad issues which ensure that:

• The Group’s main legal entities maintain adequate liquid resources

at all times to meet liabilities as they fall due.

• The Group maintains an adequate liquid asset portfolio appropriate

to the business activities of the Group and its risk profile.

• The Group has in place robust strategies, policies, systems, and

procedures for identifying, measuring, monitoring and managing

liquidity risk.

• The Group has a comprehensive liquidity risk management

framework in place to ensure the Group maintains an appropriate

level of financial resources to meet its financial obligations as and

when they fall due.

The risk management framework identifies the sources of liquidity risk

and the steps the Group can take when these risks exceed certain

actively monitored limits. These actions include when and how to use the

Group’s liquidity reserves and what other adjustments to the Group’s

balance sheet should be undertaken to manage these risks within the

Group’s risk appetite.

The Group’s appetite for liquidity risk is set by the Board as a percentage

of the Individual Liquidity Adequacy Assessment (ILAA) stressed outflows

and then managed on a daily basis by various functions within the

business with liquidity risk controlled at legal entity, country, regional and

divisional levels.

In setting risk limits the Board takes into account the nature of the

Group’s various activities, the Group’s overall risk appetite, market best

practice and regulatory compliance.

The Group Asset and Liability Management Committee (GALCO) sets

and reviews the liquidity risk management framework and limits within the

risk appetite set by the Group Board. GALCO oversees the

implementation of liquidity management across the Group. Each

significant legal entity has a nominated Legal Entity Liquidity Risk Owner

who is responsible for managing the liquidity risk for their legal entity.

Group Treasury conducts the review, challenge and reporting of the

Group’s liquidity performance, while GALCO’s management of liquidity

risk is overseen by the Executive Risk Forum, Executive Committee and

the Group Board.