RBS 2013 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review

142

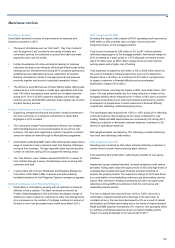

International Banking continued

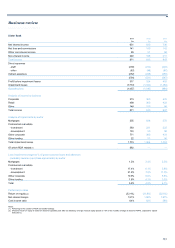

2013 compared with 2012

Operating profit, decreased by £315 million as lower income and higher

impairments, including £52 million in relation to the accelerated asset

recovery strategy associated with RCR, were only partially offset by lower

costs.

Income was 13% lower:

• Cash management was 22% lower reflecting a decline in three-

month LIBOR rates as well as increased funding costs of liquidity

buffer requirements.

• Loan portfolio decreased by 6%, in line with a smaller balance

sheet.

Expenses were down £77 million, or 5%, reflecting continued emphasis

on cost control and timely run-off of discontinued business.

Impairment losses were £118 million higher than in 2012, including two

large single-name provisions and £52 million in relation to the impact of

the accelerated RCR asset recovery strategy.

Third party assets were down 8% due to reductions in the loan portfolio

following increased levels of customer repayments partially offset by an

increase in Asia trade volume.

Customer deposits declined by 15% in line with a change in Group

funding strategy.

Risk-weighted assets decreased by 6% primarily as a result of

management action to mitigate credit model increases and a smaller

balance sheet.

Return on equity was 4% or 5% excluding the impact of the accelerated

RCR asset recovery strategy compared with 9% in 2012.

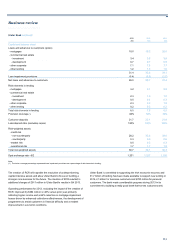

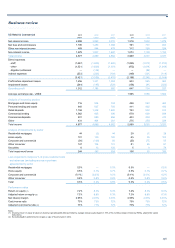

2012 compared with 2011

Operating profit decreased by £161 million as a decline in income was

only partially mitigated by lower expenses and impairment losses.

Income was 17% lower:

• Loan portfolio decreased by 32%, mainly due to a strategic

reduction in assets, in order to allocate capital more efficiently, and

the effect of portfolio credit hedging and lower corporate appetite for

risk management activities.

• Cash management was broadly in line with the previous year.

Deposit margins declined following reductions in both three month

LIBOR and five year fixed rates across Europe; however, this was

offset by lower liquidity costs due to the strategic initiative to reduce

short-term bank deposits.

• Trade finance increased by 6% as a result of increased activity,

particularly in Asia.

• The restructuring in 2012 led to a reduction in activities undertaken

in the division, which contributed to a decline in income.

Expenses declined by £215 million, reflecting planned restructuring

initiatives following the formation of the International Banking division.

Savings were achieved through headcount reduction, run-off of

discontinued businesses and a resulting decrease in infrastructure

support costs. Revenue-linked expenses also fell in line with the

decrease in income.

Impairment losses decreased by £57 million with the non-repeat of a

single name impairment.

Third party assets declined by 24%, with targeted reductions in the

lending portfolio following a strategic reduction in assets.

Customer deposits increased by 2%. Successful efforts to rebuild

customer confidence following the Moody’s credit rating downgrade and

the Group technology incident in June 2012 outweighed economic

pressures. This, coupled with the managed reduction in loans and

advances to customers, improved the loan:deposit ratio to 91%.

Bank deposits were down 51%, mainly as a result of lower short-term

balances, reflecting a strategic initiative to reduce liquidity outflow risk.

Risk-weighted assets increased by 20%, reflecting the impact of

regulatory uplifts partially offset by successful mitigation through balance

sheet reduction. Risk-weighted asset intensity in the loan book has

increased significantly given the uplifts, which will result in strategic

adjustments going forward.