RBS 2013 Annual Report Download - page 222

Download and view the complete annual report

Please find page 222 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

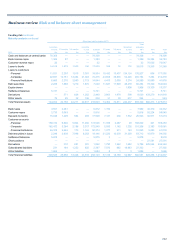

Business review Risk and balance sheet management

220

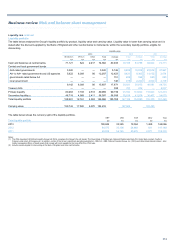

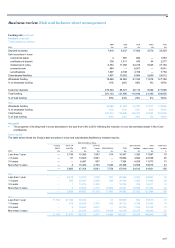

Funding risk continued

Divisional loan:deposit ratios and funding surplus

The table below shows divisional loans, deposits, loan:deposit ratios and customer funding surplus.

2013 2012 2011

Loan:deposit Funding Loan:deposit Funding Loan:deposit Funding

Loans (1) Deposits (2) ratio surplus/(gap) ratio (gap)/surplus ratio (gap)/surplus

£m £m % £m %£m % £m

UK Retail 111,046 114,889 97 3,843 103 (3,337) 106 (6,105)

UK Corporate 99,714 124,742 80 25,028 82 22,477 86 17,641

Wealth 16,644 37,173 45 20,529 44 21,945 44 21,330

International Banking 35,668 39,278 91 3,610 86 6,672 103 (1,366)

Ulster Bank 26,068 21,651 120 (4,417) 130 (6,683) 143 (9,489)

US Retail & Commercial 50,279 55,118 91 4,839 86 8,178 85 8,871

Conduits (3) — — — — —(2,458) — (10,504)

Retail & Commercial 339,419 392,851 86 53,432 88 46,794 95 20,378

Markets 25,231 21,545 117 (3,686) 112 (3,243) 85 5,522

Other 5,060 1,085 nm (3,975) 64 1,217 nm 2,464

Core 369,710 415,481 89 45,771 90 44,768 93 28,364

Non-Core 22,880 2,188 nm (20,692) nm (41,846) nm (64,235)

Direct Line Group — — —

—

—(881) — (893)

Group 392,590 417,669 94 25,079 100 2,041 108 (36,764)

nm = not meaningful

Notes:

(1) Excludes reverse repurchase agreements and net of impairment provisions.

(2) Excludes repurchase agreements.

(3) All conduits relate to International Banking and have been extracted and shown separately as they were funded by commercial paper issuance until the end of the third quarter of 2012.

Key point

• The loan:deposit ratio improved by 600 basis points to 94% with the funding surplus increasing to £25.1 billion from £2.0 billion at 31 December

2012. The improvement in Retail & Commercial funding surplus was £6.6 billion and Non-Core run-off resulted in £21.2 billion contraction of its

funding gap.

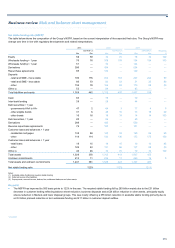

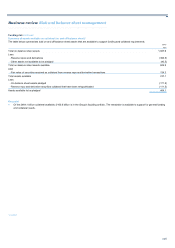

Maturity analysis

The contractual maturity of balance sheet assets and liabilities reflects the maturity transformation role banks perform, lending long-term but obtaining

funding predominantly through short-term liabilities such as customer deposits. In practice, the behavioural profiles of many liabilities exhibit greater

stability and longer maturity than the contractual maturity. This is particularly true of many types of retail and corporate deposits which, despite being

repayable on demand or at short notice, have demonstrated stable characteristics even in periods of acute stress such as those experienced in 2008.

Retail & Commercial*

The table below shows the behavioural and contractual maturity analysis of Retail & Commercial customer deposits.

Less than More than

1 year 1-5 years 5 years Total

2013 £bn £bn £bn £bn

Contractual maturity 381 12 — 393

Behavioural maturity 124 220 49 393

2012

Contractual maturity 380 20 1 401

Behavioural maturity 145 219 37 401

*unaudited