RBS 2013 Annual Report Download - page 325

Download and view the complete annual report

Please find page 325 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

323

Mitigation

To ensure approved limits are not breached and that the Group remains

within its risk appetite, triggers at Group, legal entity and divisional levels

have been set such that if exposures exceed a specified level, action

plans are developed by the front office, Market Risk and Finance.

Counterparty Exposure Management

Management of the over-the-counter derivative counterparty credit risk

and funding risk is carried out by the Counterparty Exposure

Management (CEM) desk in Markets. CEM actively manages risk

exposures and concentrations on behalf of both Markets and Non-Core.

The hedging transactions CEM enters into are booked in the trading book

and therefore contribute to the Group’s market risk VaR exposure and

capital.

Risk measurement

The Group uses a comprehensive and complementary set of

methodologies and techniques to measure traded market risk that

collectively ensure a complete approach to the measurement of material

market risks.

The Group's main measurement

methods are VaR and SVaR.

Risks that are not adequately

captured by these model

methodologies are captured by the

Risks Not in VaR (RNIV)

framework to ensure that the

Group is adequately capitalised for

market risk. In addition, stress

testing is used to identify any

vulnerabilities and potential losses

in excess of VaR and SVaR.

These methods have been designed to capture correlation effects and

allow the Group to form an aggregated view of its traded market risk

across risk types, markets and business lines while also taking into

account the characteristics of each risk type.

Each of these methodologies and techniques is discussed in more detail

below.

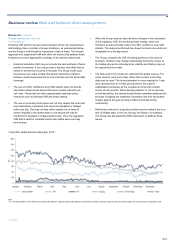

Value at-risk

VaR is a statistical estimate of the potential change in the market value of

a portfolio (and, thus, the impact on the income statement) over a

specified time horizon at a given confidence level.

For internal risk management purposes, the Group’s VaR assumes a

time horizon of one trading day and a confidence level of 99%. The

Group's VaR model is based on a historical simulation, utilising data from

the previous 500 days on an equally weighted basis.

The Group’s internal traded VaR model captures all trading book

positions including those approved by the regulator. In 2013,

improvements were made to the risk sensitivities associated with funding

valuation adjustments (FVAs), which resulted in a reduction in the hedge

portfolio. At the point of implementation, the impact on RBS plc was a £9

million decrease in 1-day 99% regulatory VaR and an associated £42

million decrease in regulatory SVaR. The current internal VaR

methodology does not include credit valuation adjustment (CVA) and

FVA exposures as these are out of scope of the measure, although the

Group is planning to include these in its internal VaR measure in 2014.

For an explanation of the distinction between internal VaR and regulatory

VaR, see page 330.

The RBS internal VaR model captures the impact on the income

statement of the following risk factors:

• Interest rate risk, which arises from the impact of changes in interest

rates and volatilities on cash instruments and derivatives. This

includes interest rate tenor basis risk and cross-currency basis risk.

• Credit spread risk, which arises from the impact of changes in the

credit spreads of sovereign bonds, corporate bonds, securitised

products and credit derivatives.

• Currency risk, which arises from the impact of changes in currency

rates and volatilities.

• Equity risk, which arises from the impact of changes in equity prices,

volatilities and dividend yields.

• Commodity risk, which arises from the impact of changes in

commodity prices and volatilities.

The risk factors presented above are sufficient to define the Group’s

overall market risk exposures. In addition, the following risks, which are

components of the above-mentioned risk factors, are also monitored by

individual businesses to identify and address any material concentrations:

• Basis risk, which is the risk that imperfect correlation between two

instruments in a hedging strategy creates the potential for excess

gains or losses, thus adding risk to the position;

• Prepayment risk, which is the risk associated with early unscheduled

return of principal on a fixed rate security; and

• Inflation risk, which is the risk of a decrease in the value of

instruments as a result of changes in inflation rates and associated

volatilities.