RBS 2013 Annual Report Download - page 330

Download and view the complete annual report

Please find page 330 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

328

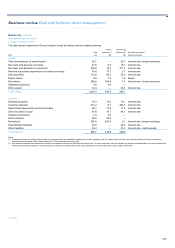

Market risk continued

Traded market risk continued

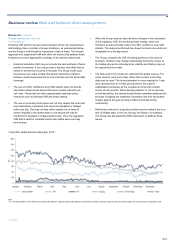

Stressed VaR (SVaR)*

As with VaR, the SVaR technique produces estimates of the potential

change in the market value of a portfolio, over a specified time horizon, at

a given confidence level. SVaR is a VaR-based measure using historical

data from a one-year period of stressed market conditions.

The risk system simulates 99% VaR on the current portfolio for each 260-

day period from 1 January 2005 to the current VaR date, moving forward

one day at a time. The SVaR is the worst VaR outcome of the simulated

results.

This is in contrast with VaR, which is based on a rolling 500-day historical

data set. For the purposes of both internal risk management and

regulatory SVaR calculation, a time horizon of ten trading days is

assumed with a confidence level of 99%.

Trading SVaR*

2013 2012

£m £m

Total Group 309 396

Core Markets 298 372

Non-Core 51 69

Key point

• The Group's period end SVaR declined in 2013 compared with

2012. This is consistent with the observed decrease in VaR during

2013 and is primarily driven by significant de-risking of interest rate

exposures and reduction in the asset-backed securities inventory.

Risks not in VaR (RNIVs)*

The RNIV approach is used for market risks that fall within the scope of

VaR and SVaR but that are insufficiently captured by the model

methodology, for example due to a lack of suitable historical data. The

RNIV framework has been developed to quantify these market risks and

to ensure that the Group holds adequate capital.

The need for an RNIV is typically identified in one of the following two

circumstances: (i) as part of the New Product Risk Assessment process,

when a risk manager assesses that the associated risk is not adequately

captured by the VaR model; or (ii) as a result of a recommendation made

by GRA or the model validation team when reviewing the VaR model.

The RNIVs provide a capital estimate of risks not captured in the VaR

model and are regularly reported and discussed with senior management

and the regulator. The methodology used in the RNIV calculation is

internally reviewed by the model-testing team. Where appropriate, risk

managers set sensitivity limits to control specific risk factors giving rise to

the RNIV. RNIVs form an integral part of the Group’s ongoing model and

data improvement efforts to capture all market risks in scope for model

approval in VaR and SVaR. Since the introduction of the RNIV

framework, the Group has made significant progress in transitioning

RNIVs into the VaR model.

The Group adopts two approaches for the quantification of RNIVs:

• A standalone VaR approach. Under this approach, two values are

calculated: (i) the VaR RNIV; and (ii) the SVaR RNIV.

• A stress-scenario approach. Under this approach, an assessment of

ten-day extreme, but plausible, market moves is used in

combination with position sensitivities to give a stress-type loss

number - the stressed RNIV value.

In 2013, for each legal entity covered by the PRA VaR model waiver,

RNIVs above a regulatory defined threshold were aggregated to obtain

the following three measures: (i) Total VaR RNIV; (ii) Total SVaR RNIV;

and (iii) Total stressed RNIV. In each of these categories, potential

diversification benefits between RNIVs are ignored.

The top ten RNIVs represent approximately two thirds of the total RNIV

capital requirement.

RNIVs are broadly classified as follows:

• Proxied sensitivities or risk factors: to cover instruments for which

market data is not available.

• Higher-order sensitivity terms: to account for the fact that the

Group’s VaR model is based on a P&L approximation function rather

than full repricing of deals.

• Interpolation and re-bucketing inaccuracy: to cover residual errors

resulting from the pre-processing of risk factors into a standard set

across tenors.

• Data selection bias: to cover the possibility of suboptimal data

sources being selected for risk factors.

• Static pricing parameters: to cover the possibility that suboptimal

assumed values are used for certain unobserved parameters

in pricing models.

• Missing basis risks: to cover cases where data sources are not

detailed enough to differentiate the risks of long and short pairs of

closely related instruments.

The most material of these are proxy or basis risks, followed by higher-

order sensitivity risks.

RNIVs that are related specifically to instruments that have level 3

valuation hierarchy assumptions (see pages 418 to 423) are mainly

included in the following categories: proxied sensitivities or risk factors;

higher-order sensitivity terms; and static pricing parameters.

*unaudited