RBS 2013 Annual Report Download - page 243

Download and view the complete annual report

Please find page 243 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

241

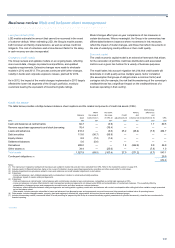

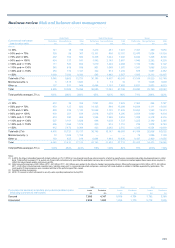

UK Retail Ulster Bank RBS Citizens (1)

Non- Non- Non-

Performing performing Total Performing performing Total Performing performing Total

Loan-to-value ratio £m £m £m £m £m £m £m £m £m

2011

<= 50% 21,537 285 21,822 2,568 222 2,790 4,745 49 4,794

> 50% and <= 70% 25,598 390 25,988 1,877 157 2,034 4,713 78 4,791

> 70% and <= 90% 33,738 671 34,409 2,280 223 2,503 6,893 125 7,018

> 90% and <= 100% 7,365 343 7,708 1,377 128 1,505 2,352 66 2,418

> 100% and <= 110% 3,817 276 4,093 1,462 130 1,592 1,517 53 1,570

> 110% and <= 130% 1,514 199 1,713 2,752 322 3,074 1,536 53 1,589

> 130% and <= 150% 60 15 75 2,607 369 2,976 626 28 654

> 150% — — — 2,798 748 3,546 588 27 615

Total with LTVs 93,629 2,179 95,808 17,721 2,299 20,020 22,970 479 23,449

Other (2) 567 13 580 — — — 681 23 704

Total 94,196 2,192 96,388 17,721 2,299 20,020 23,651 502 24,153

Total portfolio average LTV (3) 67% 80% 67% 104% 125% 106% 76% 91% 77%

A

verage LTV on new originations during the year (3) 63% 74% 63%

Notes:

(1) Includes residential mortgages and home equity loans and lines (refer to page 260 for a breakdown of balances).

(2) Where no indexed LTV is held.

(3) Average LTV weighted by value is calculated using the LTV on each individual mortgage and applying a weighting based on the value of each mortgage.

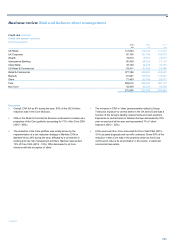

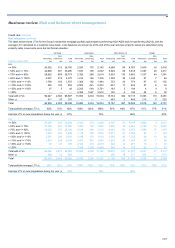

Counterparty credit risk

The Group mitigates counterparty credit risk arising from both derivatives

and repurchase agreements through the use of netting, collateral and the

use of market standard documentation.

The Group mitigates counterparty credit risk by netting amounts it owes

to a counterparty against amounts the same counterparty owes to it, in

accordance with relevant regulatory and internal policies. It generally

does so only if it has a netting agreement in place as well as a legal

opinion to the effect that the agreement is enforceable in the relevant

jurisdictions.

Collateral generally takes the form of cash. In the case of repurchase

agreements, collateral usually takes the form of debt and equity securities

at the outset but if the value of collateral falls relative to that of the

obligation, the Group may require additional collateral in the form of cash

(variation margin). Industry standard documentation, such as master

repurchase agreements and credit support annexes accompanied by

legal opinion, is used for financial collateral taken as part of trading

activities.

The Group limits counterparty credit exposures by setting limits which

take into account the potential adverse movement of a counterparty credit

exposure after adjusting the impact of netting and collateral where

applicable.

2013 2012 2011

Mitigation of counterparty credit risk £bn £bn £bn

Reverse repurchase agreements 76.5 104.8 100.9

Securities received as collateral (1) (76.4) (104.7) (98.9)

Derivative assets gross exposure 288.0 441.9 530.1

Counterparty netting (242.8) (373.9) (441.6)

Cash collateral held (24.3) (34.1) (37.2)

Securities received as collateral (6.0) (5.6) (5.3)

Note:

(1) In accordance with normal market practice, at 31 December 2013 £63.7 billion (2012 - £100.7 billion; 2011 - £95.4 billion) had been resold or re-pledged as collateral for the Group's own

transactions.