RBS 2013 Annual Report Download - page 262

Download and view the complete annual report

Please find page 262 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

260

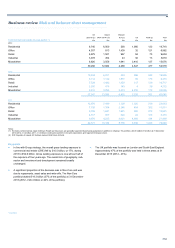

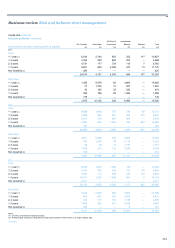

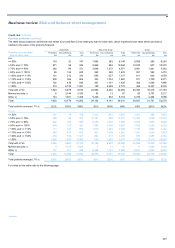

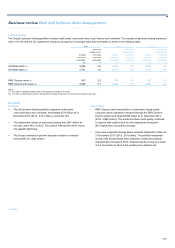

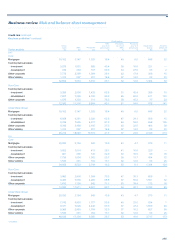

Credit risk continued

Key loan portfolios* continued

Ulster Bank

• Ulster Bank’s residential mortgage portfolio was £19.0 billion at 31

December 2013, with 88% in the Republic of Ireland and 12% in

Northern Ireland. At constant exchange rates, the portfolio

decreased 2.5% from 31 December 2012 as a result of amortisation

and limited growth due to low market demand.

• The assets included £2.2 billion (12%) of residential buy-to-let loans.

The interest rate product mix was approximately 68% on tracker rate

products, 23% on variable rate products and 9% on fixed rate.

Interest only represented 11% of the total portfolio.

• The average individual LTV on new originations was 73% in 2013,

(2012 - 74%); the volume of new business remained very low. The

maximum LTV available to Ulster Bank customers was 90% with the

exception of a specific Northern Ireland scheme which permits LTVs

of up to 95% (although Ulster Bank’s exposure is capped at 85%

LTV).

• The portfolio average indexed LTV fell 4% during 2013 and reflected

positive house price index trends over the last 12 months.

• Refer to the Ulster Bank Group (Core and Non-Core) section on

pages 265 to 267 for commentary on mortgage REIL and

impairments.

*unaudited

RBS Citizens

• RBS Citizens residential real estate portfolio was £19.6 billion at 31

December 2013 (2012 - £21.5 billion). The Core business comprised

91% of the portfolio. The real estate portfolio consisted of £5.9 billion

(£5.6 billion Core vs. £0.3 billion Non-Core) of first lien residential

mortgages (1% in second lien position) and £13.5 billion (£12.0

billion Core vs. £1.5 billion Non-Core) of home equity loans and lines

(first and second liens). Home equity Core consisted of 49% in first

lien position while Non-Core consisted of 95% in second lien

position.

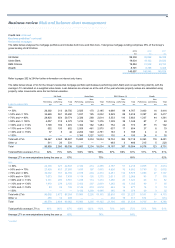

• RBS Citizens continued to focus on its ‘footprint states’ of New

England, Mid Atlantic and Mid West regions. At 31 December 2013,

the portfolio consisted of £16.4 billion (84% of the total portfolio)

within footprint.

• Of the total real estate portfolio of £1.8 billion in Non-Core, the

serviced-by-others (SBO) element was the largest component

(76%). The SBO book decreased from £1.8 billion at 31 December

2012 to £1.4 billion at 31 December 2013 and was closed to new

purchases in the third quarter of 2007. The arrears rate of the SBO

portfolio decreased from 1.9% at 31 December 2012 to 1.6% at 31

December 2013 reflecting portfolio liquidation as well as more

effective account servicing and collections. The charge-off rate also

continued to decrease (4.4% annualised at the fourth quarter of

2013 compared to 7.4% in 2012).

• The weighted average LTV of the portfolio decreased from 75% at

31 December 2012 to 67% at 31 December 2013, driven by

increases in the Case-Shiller Home Price Index from the third

quarter of 2012 to the fourth quarter of 2013. The weighted average

LTV of the portfolio, excluding SBO, was 64%.