RBS 2013 Annual Report Download - page 337

Download and view the complete annual report

Please find page 337 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

335

The Group uses both approaches to quantify its interest rate risk: VaR as

its value-based approach and sensitivity of net interest income (NII) as its

earnings-based approach.

These two approaches provide different yet complementary views of the

impact of interest rate risk on the balance sheet at a point in time. The

scenarios employed in the NII sensitivity approach incorporate business

assumptions and simulated modifications in customer behaviour as

interest rates change. In contrast, the VaR approach assumes static

underlying positions and therefore does not provide a dynamic

measurement of interest rate risk. In addition, while the NII sensitivity

calculations are measured to a 12-month horizon and thus provide a

shorter-term view of the risks on the balance sheet, the VaR approach

can identify risks not captured in the sensitivity analysis, in particular the

impact of duration and repricing risk on earnings beyond 12 months.

Value-at-risk

The Group’s standard VaR metrics - which assume a time horizon of one

trading day and a confidence level of 99% - are based on interest rate

repricing gaps at the reporting date. Daily rate moves are modelled using

observations over the last 500 business days. These incorporate

customer products plus associated funding and hedging transactions as

well as non-financial assets and liabilities such as property, plant and

equipment, capital and reserves. Behavioural assumptions are applied as

appropriate.

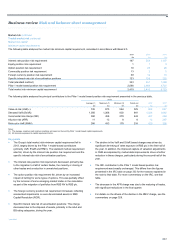

The table below shows the NTIRR VaR for the Group’s retail and

commercial banking activities at a 99% confidence level together with a

currency analysis of period end VaR.

Average Period end Maximum Minimum

£m £m £m £m

2013 45 51 57 30

2012 46 21 65 20

2011 63 51 80 44

2013 2012 2011

£m £m £m

Euro 4 19 26

Sterling 19 17 57

US dollar 44 15 61

Other 2 4 5

Key points

• Period end interest rate VaR was higher at 31 December 2013 than

at 31 December 2012. Average VaR was relatively unchanged.

• The overall year-on-year increase in VaR mainly reflected an

increase in the duration of the Group’s balance sheet - that is,

greater economic exposure to longer-term interest rates - as

described in more detail below.

• Euro VaR fell, reflecting action taken to reduce the Group’s

exposure to euro-denominated fixed-rate assets.

• US dollar VaR rose, reflecting action taken by US Retail &

Commercial to reduce earnings sensitivity to movements in short

term dollar interest rates.

• These movements remained well within the Group’s approved

market risk appetite.

Sensitivity of net interest income*

To analyse earnings sensitivities, forecasts are generated using implied

forward rates, projected new business volumes, mix and pricing

generated using business assumptions. Based on the balance sheet at

the most recent month end, two NII forecasts are calculated each month:

(i) a forecast for the current full year, which incorporates actuals on a

monthly basis as the year progresses; and (ii) a base-case 12 month

rolling forecast.

In addition, the 12 month rolling forecast is re-run using alternative rates

under various scenarios, incorporating changes in customer behaviour

and business assumptions as appropriate. Variances between these

scenarios are analysed to identify key drivers. These forecasts and

sensitivities form part of the information used by senior management to

manage the Group's NII targets.

This sensitivity analysis also incorporates assumptions relating to

optionality risk.