RBS 2013 Annual Report Download - page 213

Download and view the complete annual report

Please find page 213 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

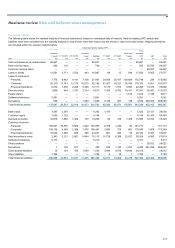

Business review Risk and balance sheet management

211

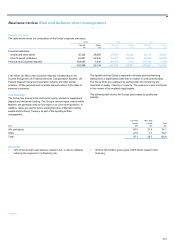

Regulatory oversight*

The Group operates in multiple jurisdictions and is subject to a number of

regulatory regimes.

The Group’s principal regulator, the PRA, has a comprehensive set of

liquidity policies, the cornerstone of which is Policy Statement (PS) 09/16.

In order to comply with the PRA regulatory process, the Group:

• At least annually, completes and keeps updated an ILAA;

• Undertakes the Focused Liquidity Review process which is a

comprehensive review of the Group’s ILAA, liquidity policies and

operational capacity and capability. This in turn leads to the Group

and the PRA agreeing the parameters of Group’s Individual Liquidity

Guidance (ILG) which influences the overall size of the Group’s

liquidity portfolio.

In addition, the Group’s US operations meet liquidity requirements set out

by the Federal Reserve Board, the Office of the Comptroller of the

Currency, the Federal Deposit Insurance Corporation and the Financial

Industry Regulatory Authority. In the Netherlands, RBS N.V. is subject to

the De Nederlandsche Bank liquidity oversight regime. In the Republic of

Ireland, Ulster Bank Ireland Limited is subject to oversight from the

Central Bank of Ireland.

In January 2013, the Basel Committee on Banking Supervision (BCBS)

issued its revised draft guidance for calculating the liquidity coverage

ratio (LCR), which is currently expected to come into force from 1

January 2015 on a phased basis. Pending the finalisation of the

definitions, the Group monitors the LCR and the net stable funding ratio

(NSFR) in its internal reporting framework based on its interpretation and

expectation of the final rules. On this basis, as of 31 December 2013, the

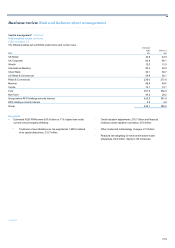

Group’s LCR was 102% and the NSFR 122%.

At present there is a broad range of interpretations on how to calculate

both the NSFR and the LCR due to the lack of commonly agreed

technical standards. The Group continues to assess the impact of these

consultations and actively communicates with regulators and industry

groups. Assumptions will be refined as regulatory interpretations evolve.

Under the EU Capital Requirements Regulation to implement the

recommended guidance of Basel 3, the European Banking Authority

(EBA) is tasked with issuing a set of technical standards for implementing

the LCR within the EU, to be ratified by the European Commission before

30 June 2014. The LCR metric will come into effect as a minimum

standard from 1 January 2015.

The PRA has issued a statement proposing to retain the existing ILG

framework until 31 December 2014, whilst the EBA’s implementation of

the LCR is finalised.

Several regulatory regimes outside the EU where the Group operates

have also published consultation papers with guidance for

implementation of the LCR, including the Joint Banking Supervisors of

the US. We anticipate further consultations for LCR standards to be

published across other jurisdictions in which the Group operates during

the course of 2014. Additionally, the BCBS has issued a proposal for

revising the guidance on NSFR, expected to be finalised in 2014.

*unaudited

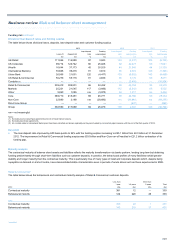

Measurement and monitoring

In implementing the Group’s liquidity risk management framework, a suite

of tools are used to monitor, limit and stress test the risks within the

balance sheet. The limits control the amount and composition of funding

sources, asset and liability mismatches and funding concentrations, in

addition to the level of liquidity risk.

To foster appropriate pricing behaviour, decision making and balance

sheet composition Group Treasury uses transfer pricing of liquidity and

funding costs, limits and parameters. This ensures liquidity and funding

risk is reflected in the measurement of divisional business performance

and ensures divisions are being correctly incentivised to source the most

appropriate mix of funding.

The Board’s determination and quantification of the appetite for liquidity

risk is primarily determined by reference to the ILAA which includes a

comparison of the size of liquidity portfolio to an assessment of stressed

outflows. The ILAA also informs the Board and PRA of the Group’s

liquidity risks, their mitigation and about the current and future liquidity

profile.

Within the liquidity portfolio the Group holds cash at central banks, high

quality government securities and collateral eligible for use in central

bank operations, such as the Bank of England’s Discount Window

Facility.

In determining what assets should be held within the liquidity portfolio, the

liquidity risk management framework dictates minimum internal quality

criteria, level of currency diversification and maturity mix. The liquidity

value of an asset is generally determined by reference to the haircut that

would be applied by a central bank operation or in a private repurchase

agreement.

The Group actively monitors a range of market-wide and firm-specific

early warning indicators of emerging liquidity stresses. Indicators include

such areas as customer deposit outflows, market funding costs and

movements in the Group’s credit default swap premiums. Early warning

indicators and regulatory metrics are reported daily to senior

management, including the CFO and Group Treasurer.

Liquidity risks are reviewed daily at a significant legal entity level and

performance reported at least monthly to legal entity, divisional and

Group Asset and Liability Management Committees. Any breach of

internal metric limits will set in motion a series of actions and escalations

that could lead to activation of the Group’s Contingency Funding Plan.

In November 2013, the Group’s credit rating was downgraded by

Standard & Poor’s. Prior to this event, the Group undertook an intensive

internal review of the magnitude of a rating downgrade on customer and

counterparty behaviours and these included stress testing and scenario

modelling. This analysis was also shared with the PRA. Following the

downgrade by Standard & Poor’s, there was minimal impact on customer

or counterparty behaviour, the primary reason for deposit withdrawals

was due to contractual downgrade triggers or the rating no longer

meeting the customer or counterparty’s investment requirements.