RBS 2013 Annual Report Download - page 525

Download and view the complete annual report

Please find page 525 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

515 -

516

516 -

517

517 -

518

518 -

519

519 -

520

520 -

521

521 -

522

522 -

523

523 -

524

524 -

525

525 -

526

526 -

527

527 -

528

528 -

529

529 -

530

530 -

531

531 -

532

532 -

533

533 -

534

534 -

535

535 -

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

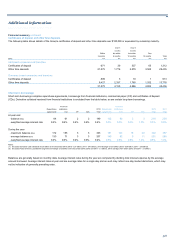

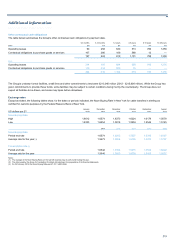

Additional information

523

Risk factors

Set out below are certain risk factors which could adversely affect the

Group's future results, its financial condition and prospects and cause

them to be materially different from what is expected. The factors

discussed below and elsewhere in this report should not be regarded as

a complete and comprehensive statement of all potential risks and

uncertainties facing the Group.

The Group’s ability to implement its new strategic plan and achieve its

capital goals depends on the success of the Group's plans to refocus on

its core strengths and the timely divestment of RBS Citizens

Since the beginning of the global economic and financial crisis in 2008

and as a result of the changed global economic outlook, the Group has

been engaged in a financial and core business restructuring which has

been focused on achieving appropriate risk-adjusted returns under these

changed circumstances, reducing reliance on wholesale funding and

lowering exposure to capital-intensive businesses. A key part of the

restructuring programme announced in February 2009 was to run down

and sell the Group’s non-core assets and businesses with a continued

review of the Group’s portfolio to identify further disposals of certain non-

core assets and businesses. Assets identified for this purpose and

allocated to the Group’s Non-Core division totalled £258 billion, excluding

derivatives, at 31 December 2008. By 31 December 2013, this total had

reduced to £28.0 billion (31 December 2012 - £57.4 billion), excluding

derivatives, as further progress was made in business disposals and

portfolio sales during the course of 2013. This balance sheet reduction

programme has been implemented alongside the disposals under the

State Aid restructuring plan approved by the EC. During 2012 the Group

implemented changes to its wholesale banking operations, including the

reorganisation of its wholesale businesses and the exit and downsizing of

selected existing activities (including cash equities, corporate banking,

equity capital markets, and mergers and acquisitions).

During Q3 2013, the Group worked with HM Treasury as part of its

assessment of the merits of creating an external “bad bank” to hold

certain assets of the Group. Although the review concluded that the

establishment of an external “bad bank” was not in the best interests of

all stakeholders, the Group committed to take a series of actions to

further de-risk its business and strengthen its capital position.

These actions include:

• The formation of the Capital Resolution Group (CRG), which is

made up of four pillars: exiting the assets in RBS Capital Resolution

(RCR), delivering the initial public offerings (IPO) for both RBS

Citizens and Williams & Glyn and optimising the Group’s shipping

business;

• The creation of RCR to manage the run-down of problem assets,

which totalled £29 billion at the end of 2013, with the goal of

removing 55-70% of these assets over the next two years with a

clear aspiration to remove all these assets from the balance sheet in

three years; and

• Lifting the Group’s capital targets including by:

° accelerating the divestment of RBS Citizens, the Group’s US

banking subsidiary, with a partial IPO now planned for 2014, and

full divestment of the business intended by the end of 2016; and

° intensifying management actions to reduce risk weighted assets.

Since the end of Q3 2013, the Group has been conducting a review of its

activities which has resulted in additional changes to the Group’s

strategic goals. It is now intended to further simplify and downsize the

Group with an increased focus on service to its customers. As part of

simplifying the Group, the current divisional structure will be replaced by

three new customer segments, covering Personal & Business,

Commercial & Private Banking and Corporate & Institutional Banking. As

part of this reorganisation of the business, the intention will be to remain

in businesses where the Group can be number one for its customers. For

those businesses where that is not the case, the Group will either fix,

close or dispose of such businesses. This reorganisation, together with

investment in technology and more efficient support functions are

intended to deliver significant improvements in the Group’s Return on

Equity and costs: income ratio in the longer term.

Implementation of the Group’s new strategic plan will require significant

restructuring of the Group at the same time that it will also be

implementing structural changes to comply with the Financial Services

(Banking Reform) Act 2013 (the “Banking Reform Act” 2013) and its ring-

fencing requirements. The level of structural change intended to be

implemented within the Group over the medium term taken together with

the overall scale of change to make the Group a smaller, more focused

financial institution, are likely to be disruptive and increase operational

risks for the Group. There can be no assurance that the Group will be

able to successfully implement this new strategy together with other

changes required of the Group in the time frames contemplated or at all.

The Group’s ability to dispose of businesses, including RBS Citizens and

the EC mandated branch divestment now known as Williams & Glyn, and

assets and the price achieved for such disposals will be dependent on

prevailing economic and market conditions, which remain volatile. As a

result there is no assurance that the Group will be able to sell or run

down (as applicable) the businesses it has planned to sell or exit or asset

portfolios it is seeking to sell either on favourable economic terms to the

Group or at all. Material tax or other contingent liabilities could arise on

the disposal or run-down of assets or businesses and there is no

assurance that any conditions precedent agreed will be satisfied, or

consents and approvals required will be obtained in a timely manner, or

at all. There is consequently a risk that the Group may fail to complete

such disposals within time frames envisaged by the Group, its regulators

and the EC.

The Group may be exposed to deteriorations in businesses or portfolios

being sold between the announcement of the disposal and its completion,

which period may be lengthy and may span many months. In addition,

the Group may be exposed to certain risks, including risks arising out of

ongoing liabilities and obligations, breaches of covenants,

representations and warranties, indemnity claims, transitional services

arrangements and redundancy or other transaction related costs.

The occurrence of any of the risks described above could negatively

affect the Group’s ability to implement its new strategic plan and achieve

its capital targets and could have a material adverse effect on the

Group’s business, results of operations, financial condition and cash

flows. There can also be no assurance that if the Group is able to

execute its strategic plan that the new strategy will ultimately be

successful or beneficial to the Group.