RBS 2013 Annual Report Download - page 192

Download and view the complete annual report

Please find page 192 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

190

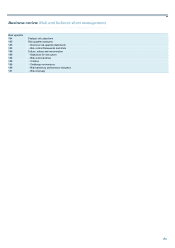

Risk appetite*: Risk coverage continued

Risk type Definition Features How the Group manages risk and the focus in 2013

Pension risk The risk to a firm caused by its

contractual or other liabilities to,

or with respect to, its pension

schemes, whether established

for its employees or for those of

a related company or

otherwise. It also means the

risk that the firm will make

payments or other contributions

to, or with respect to, a pension

scheme because of a moral

obligation, or because the firm

considers that it needs to do so

for some other reason.

Arises from: Variation in value of

pension scheme assets and liabilities

owing to changes to life expectancy,

interest rates, inflation, credit spreads,

and equity and property prices.

Character and impact: Pension

schemes’ funding positions can be

volatile due to the uncertainty of future

investment returns and the projected

value of schemes’ liabilities. The Group

might have to make financial

contributions to, or with respect to, its

pension schemes.

It has the potential to adversely affect

the Group’s funding and capital

requirements.

The Group’s Pension Risk Committee considers the

Group’s view of pension risk, mechanisms that could be

used for managing pension risk and the financial strategy

implications of the pension schemes as well as reviewing

fund performance. The Committee reports to the Group

Asset and Liability Committee on the material pension

schemes that the Group is obliged to support.

In 2013, various pension risk stress testing initiatives were

undertaken, focused both on internally defined scenarios

and on scenarios designed to meet integrated PRA stress

testing requirements.

Refer to the Pension risk section on pages 356 and 357 for

further information.

Operational risk The risk of loss resulting from

inadequate or failed processes,

people, systems or from

external events.

Arises from: The Group’s day-to-day

operations and is relevant to every

aspect of the Group’s business.

Character and impact: May be financial

in nature (characterised by either

frequent small losses or infrequent

material losses), or may lead to direct

customer and/or reputational impact

(for example, a major IT systems

failure or fraudulent activity).

It has the potential to affect the

Group’s profitability and capital

requirements directly, as well as

stakeholder confidence.

Operational risk is managed by the Operational Risk

Executive Committee. It is responsible for identifying and

managing emerging operational risks, and for reviewing

and monitoring operational risk profile strategies and

frameworks, ensuring they are in line with risk appetite.

In 2013, the focus was on continued implementation and

embedding of risk assessments across the Group,

including the strengthening of links between risk

assessments and other elements of the Group operational

risk framework. In addition, risk assessments were

increasingly used to identify single points of failure.

Refer to the Operational risk section on pages 358 to 360

for further information.

Regulatory risk The risk of material loss or

liability, legal or regulatory

sanctions, or reputational

damage, resulting from the

failure to comply with (or

adequately plan for changes to)

relevant official sector policy,

laws, regulations, or major

industry standards, in any

location in which the Group

operates.

Arises from: The Group’s regulatory,

business or operating environment,

and in how it responds to these.

Character and impact: The

crystallisation of regulatory risk can

result in adverse impacts on the

Group’s customers, strategy, business,

financial condition or reputation, for

instance, through the failure to provide

appropriate protections to customers,

or from regulatory enforcement or

other interventions.

It has the potential to adversely impact

the Group’s customers, strategy,

business, financial condition or

reputation.

The management of regulatory (as well as conduct) risk is

overseen by the Conduct and Regulatory Affairs function.

The Group’s existing Compliance and Regulatory Affairs

teams were brought together in the second half of 2013,

following the creation of the role of Group Head of Conduct

and Regulatory Affairs. The Conduct and Regulatory

Affairs function has responsibility for setting Group-wide

policy and standards, providing advice to the business and

ensuring controls are effective for managing regulatory

affairs, compliance and financial crime risks across all

businesses.

Other enhancements were also made during 2013

included the creation of a more centralised approach to

assurance activities and the introduction of a new ‘Centres

of Excellence’ model for the management of regulatory

developments, bringing together divisional and functional

resources to manage issues more effectively.

Refer to the Regulatory risk section on page 360 and 361

for further information.

*unaudited