RBS 2013 Annual Report Download - page 232

Download and view the complete annual report

Please find page 232 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

230

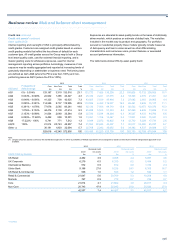

Credit risk continued

Risk management* continued

Retail

Retail lending entails making a large number of small value loans. To

ensure that it makes these lending decisions consistently, the Group

analyses the historical debt servicing behaviour of customers, including

their behaviour with respect to their other lenders. The Group then uses

the results of these analyses to set its lending rules, developing different

rules for different products. The resulting credit decision making process

is then largely automated, with customers receiving a credit score that

reflects the outcome of a comparison of their credit profile with the rule

set. However, in the case of relatively high value, complex personal or

small business loans, including some residential mortgage lending,

specialist credit managers make the final lending decisions.

Controls and assurance

The Group’s credit control and assurance framework has three key

components: credit policy; policy compliance assurance; and

independent assurance. These apply to both wholesale and retail credit

risk at both portfolio and individual customer level.

The first component is the Group Credit Policy Standard, which is part of

the Group Policy Framework. It sets out the rules the Group’s businesses

must follow to ensure that credit risks are identified and effectively

managed through the credit lifecycle.

The second component is a policy assurance activity that GCR

undertakes to provide the GCCO with evidence of the effectiveness of

credit risk management controls in place across the Group. The results of

these reviews are presented to the Group Credit Risk Committee on a

regular basis in support of the self-certification that GCR must complete

from time to time.

The third component of the Group’s credit assurance framework is the

Credit Quality Assurance (CQA) function. CQA independently reviews the

Group’s lending activities to identify control breaches, assess portfolio

quality and recommend process improvements. These findings are

escalated to senior management and plans to address shortcomings are

recorded and tracked in the Group’s operational risk system. CQA’s

activities are overseen by GAC and the results of its reviews are regularly

shared with the Group’s main regulators.

Risk measurement*

The Group uses a range of measures for credit risk exposures. The

internal measure used, unless otherwise stated, is credit risk assets

(CRA) consisting of:

• Lending exposure - measured using drawn balances and includes

cash balances at central banks and loans and advances to banks

and customers (including overdraft facilities, instalment credit and

finance leases).

*unaudited

• Counterparty exposures - measured using marked-to-market value

of derivatives after the effect of enforceable netting agreements and

regulatory approved models but before the effect of collateral.

Counterparty exposures include rate risk management, which

includes exposures arising from foreign exchange transactions,

interest rate swaps, credit default swaps and options. Exposures are

mitigated by off-setting in-the-money and out-of-the-money

transactions where such transactions are governed by legally

enforceable netting agreements and exposures are calculated by

regulatory approved models. Exposures are shown before deducting

collateral.

• Contingent obligations - measured using the value of the committed

amount and including primarily letters of credit and guarantees.

CRA exclude issuer risk (primarily debt securities) and securities

financing, repurchase and reverse repurchase arrangements. CRAs take

account of regulatory netting although, in practice, obligations are settled

under legal netting arrangements that provide a right of legal set-off but

do not meet the offset criteria under IFRS.

Credit risk models

The Group uses credit risk models in the credit approval process,

ongoing credit risk management, monitoring and reporting and portfolio

analytics. These may be divided into three categories:

Probability of default (PD)

PD models assess the probability of a customer failing its credit

obligations over a one year period.

• Wholesale models - A number of credit grading models are in place

that consider risk characteristics relevant to different customer

types. These models use a combination of quantitative inputs, such

as recent financial performance, and qualitative inputs such as

management performance or sector outlook. As part of the credit

assessment process, the Group assigns each customer an internal

credit grade based on its PD.

• Retail models - Each customer account is scored and models are

used to assign a PD. Inputs vary across portfolios and include both

internal account and customer level data, as well as data from credit

bureaus. This score is used to support automated credit decision

making through the use of a statistically derived scorecard.

Exposure at default (EAD)

EAD models provide estimates of the level of use of a credit facility at the

time of a customer's default, recognising that customers may make

further drawings on unused credit facilities prior to default. Regulatory

requirements determine that EAD is always equal to or higher than

current utilisation. Exposure can be reduced by a netting agreement,

subject to meeting standards of legal enforceability.