RBS 2013 Annual Report Download - page 251

Download and view the complete annual report

Please find page 251 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

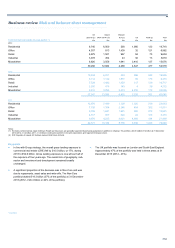

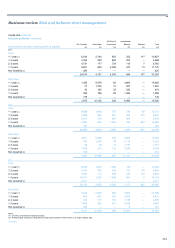

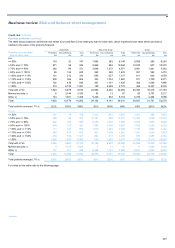

Business review Risk and balance sheet management

249

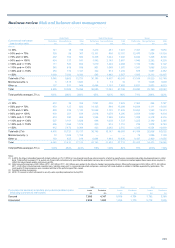

Key points

UK Retail

• At 31 December 2013, forbearance balances where the forbearance

treatment was provided in the last 24 months amounted to £2.0

billion. This represented a 14% reduction in the year.

• The flow of new forbearance of £380 million in the fourth quarter of

2013 continued on a downward trend compared with an average of

£456 million in the preceding four quarters. The full year flow for

2013 was £1.7 billion, a 15% reduction on the 2012 flow.

• 5.5% of total mortgage assets (£5.4 billion) were subject to a

forbearance arrangement agreed since January 2008. This

represented an increase from 4.9% on 2012 (£4.8 billion). The rise

was driven by an extension of the reporting definition to include

legacy conversions to interest only repayment in cases where

customers were previously on a combination of repayment types.

Excluding this change in definition, forbearance stock remained

stable.

• Approximately 84% of forbearance loans (2012 - 83%) were up to

date with payments compared with approximately 97% of assets not

subject to forbearance activity.

• The majority (90%) of UK Retail forbearance is permanent in nature

(term extensions, capitalisation of arrears, historic conversions to

interest only). Temporary forbearance comprises payment

concessions such as reduced or deferred payments with such

arrangements typically agreed for a period of three to six months.

• The most frequently occurring forbearance types were term

extensions (43% of forbearance loans at 31 December 2013),

interest only conversions (31%) and capitalisations of arrears (16%).

The growth of interest only stock reflected the extended definition

referred to above. The underlying level of transfers was negligible

and the remaining stock was the result of legacy policy. Conversions

to interest only have only been permitted on a very exceptional basis

since the fourth quarter of 2012 and have not been permitted for

customers in financial difficulty since 2009.

• The impairment provision cover on forbearance loans remained

significantly higher than that on assets not subject to forbearance.

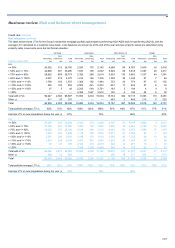

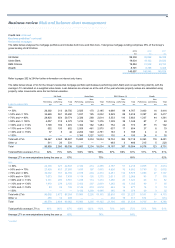

Ulster Bank

• At 31 December 2013, 14.6% of total mortgage assets (£2.8 billion)

were subject to a forbearance arrangement (agreed since early

2009), an increase from 10.4% (£2.0 billion) at 31 December 2012.

This reflected Ulster Bank’s proactive strategies to contact

customers in financial difficulty to offer assistance.

• Although the forbearance stock increased by 40% during the year,

the number of customers approaching Ulster Bank for assistance for

the first time remained broadly stable. This can be attributed to more

mortgages being put on to longer-term arrangements, and therefore

not exiting forbearance.

• The majority of forbearance arrangements were less than 90 days in

arrears (72%).

• The mix of forbearance treatments in Ulster Bank changed with an

increase in longer-term solutions. A total of 28% of forbearance

loans were subject to a permanent arrangement at 31 December

2013 (2012 - 15%). Capitalisations represented 17% and term

extensions represented 11% of the forbearance portfolio at 31

December 2013, increasing from 6% and 9% respectively.

• The remaining forbearance loans were temporary concessions

accounting for 72%. Short to medium-term concessions are offered

for periods of three months to five years and incorporate different

levels of repayment based on the customer’s ability to pay.

• Temporary interest only arrangements decreased during 2013 to

18% of forbearance loans at 31 December 2013 (2012 - 46%). This

reflected Ulster Bank’s strategy to transition customers in financial

difficulty to long-term arrangements.

• Payment concessions represented the remaining 54%, comprising:

deals where payments amortised the outstanding balance (41%); a

diminishing portfolio of deals that negatively amortised (10%); and

payment holidays (3%).

• The impairment provision cover on forbearance loans remained

significantly higher than that on assets not subject to forbearance.