RBS 2013 Annual Report Download - page 497

Download and view the complete annual report

Please find page 497 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

487 -

488

488 -

489

489 -

490

490 -

491

491 -

492

492 -

493

493 -

494

494 -

495

495 -

496

496 -

497

497 -

498

498 -

499

499 -

500

500 -

501

501 -

502

502 -

503

503 -

504

504 -

505

505 -

506

506 -

507

507 -

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Notes on the consolidated accounts

495

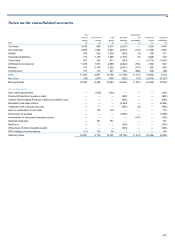

41 Related parties

UK Government

On 1 December 2008, the UK Government through HM Treasury became

the ultimate controlling party of The Royal Bank of Scotland Group plc.

The UK Government's shareholding is managed by UK Financial

Investments Limited, a company wholly owned by the UK Government.

As a result, the UK Government and UK Government controlled bodies

became related parties of the Group.

The Group enters into transactions with many of these bodies on an

arm’s length basis. The principal transactions during 2013, 2012 and

2011 were: Bank of England facilities and the issue of debt guaranteed

by the UK Government discussed below and the Asset Protection

Scheme which the Group exited on 18 October 2012 having paid total

premiums of £2.5 billion. In addition, the redemption of non-cumulative

sterling preference shares and the placing and open offer in April 2009

was underwritten by HM Treasury and, in December 2009, B shares were

issued to HM Treasury and a contingent capital agreement concluded

with HM Treasury (see Note 27). Other transactions include the payment

of: taxes principally UK corporation tax (page 404) and value added tax;

national insurance contributions; local authority rates; and regulatory fees

and levies (including the bank levy (page 393) and FSCS levies (page

473)); together with banking transactions such as loans and deposits

undertaken in the normal course of banker-customer relationships.

Bank of England facilities

The Group also participates in a number of schemes operated by the

Bank of England available to eligible banks and building societies.

• Open market operations - these provide market participants with

funding at market rates on a tender basis in the form of short and

long-term repos on a wide range of collateral and outright purchases

of high-quality bonds to enable them to meet the reserves that they

must hold at the Bank of England.

• The special liquidity scheme - this was launched in April 2008 to

allow financial institutions to swap temporarily illiquid assets for

treasury bills, with fees charged based on the spread between 3-

month LIBOR and the 3-month gilt repo rate. The scheme officially

closed on 30 January 2012.

At 31 December 2013, the Group had no amounts outstanding under

these facilities (2012 and 2011 - nil).

Members of the Group that are UK authorised institutions are required to

maintain non-interest bearing (cash ratio) deposits with the Bank of

England amounting to 0.11% of their eligible liabilities. They also have

access to Bank of England reserve accounts: sterling current accounts

that earn interest at the Bank of England Rate.

Government credit and asset-backed securities guarantee schemes

These schemes guarantee eligible debt issued by qualifying institutions

for a fee. The fee, payable to HM Treasury is based on a per annum rate

of 25 (asset-backed securities guarantee scheme) and 50 (credit

guarantee scheme) basis points plus 100% of the institution's median

five-year credit default swap spread during the twelve months to 1 July

2008. The asset-backed securities scheme closed to new issuance on 31

December 2009 and the credit guarantee scheme on 28 February 2010.

At 31 December 2013, the Group had no debt outstanding guaranteed by

the UK Government (2012 - nil; 2011 - £21.3 billion).

National Loan Guarantee Scheme

The Group participated in the National Loan Guarantee Scheme (NLGS),

providing loans and facilities to eligible customers at a discount of one

percent. It did not issue any guaranteed debt under the scheme and

consequently, it was not committed to providing a particular volume of

reduced rate facilities. At 31 December 2013 the Group had no amounts

outstanding under the scheme (2012 - £898 million). The NLGS was

superseded by the Funding for Lending Scheme.

The Funding for Lending Scheme

The Funding for Lending Scheme was launched in July 2012. Under the

scheme UK banks and building societies are able to borrow UK treasury

bills from the Bank of England in exchange for eligible collateral during

the drawdown period (1 August 2012 to 31 January 2014). Borrowing is

limited to 5% of the participant’s stock of loans to the UK non-financial

sector as at 30 June 2012, plus any expansion in lending from that date

to the end of 2013. Eligible collateral comprises all collateral eligible for

the Bank of England’s discount window facility. The term of each

transaction is four years from the date of drawdown. The price for

borrowing UK treasury bills under the scheme depends on the

participant’s net lending to the UK non-financial sector between 30 June

2012 and the end of 2013. If lending is maintained or expanded over that

period, the fee is 0.25% per year on the amount borrowed. If lending

declines, the fee increases by 0.25% for each 1% fall in lending, up to a

maximum fee of 1.5%. As at 31 December 2013, the Group had no

amounts outstanding under the scheme (2012 - £749 million).

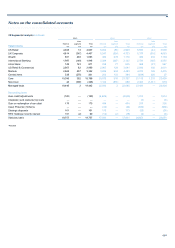

Other related parties

(a) In their roles as providers of finance, Group companies provide

development and other types of capital support to businesses. These

investments are made in the normal course of business and on arm's

length terms. In some instances, the investment may extend to

ownership or control over 20% or more of the voting rights of the

investee company. However, these investments are not considered

to give rise to transactions of a materiality requiring disclosure under

IAS 24.

(b) The Group recharges The Royal Bank of Scotland Group Pension

Fund with the cost of administration services incurred by it. The

amounts involved are not material to the Group.

(c) In accordance with IAS 24, transactions or balances between Group

entities that have been eliminated on consolidation are not reported.

(d) The captions in the primary financial statements of the parent

company include amounts attributable to subsidiaries. These

amounts have been disclosed in aggregate in the relevant notes to

the financial statements.