RBS 2013 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review

137

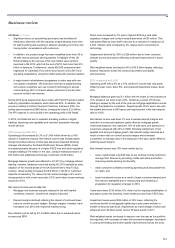

As well as delivering a range of lending initiatives, UK Corporate

continued to develop new propositions for its customers. Following a

successful pilot UK Corporate launched a leading business-to-business

online community platform, Bizcrowd, to support independent needs

matching. By the end of 2013 Bizcrowd had over 27,000 users and is

now helping to bring businesses together across the UK.

During the course of 2013 UK Corporate’s Business Banking Enterprise

Programme helped over 40,000 entrepreneurs through over 1,000

events. Through its combination of nationwide start-up surgeries, mobile

business schools and business academies, the programme offers

support and advice to aspiring entrepreneurs, new start-up businesses

and established SMEs looking to grow. Combined with UK Corporate’s

skills-based volunteering scheme, a programme offering all employees

five days to volunteer with a charitable organisation, UK Corporate

continued to deliver on its on-going commitment to communities.

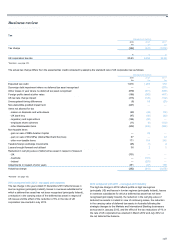

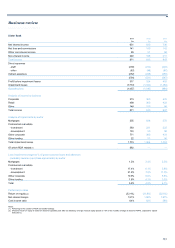

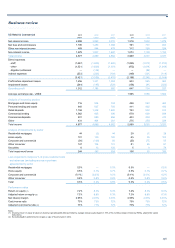

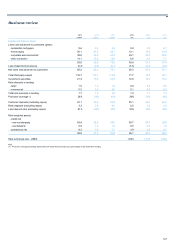

2013 compared with 2012

The business delivered a return on equity of 11.0% excluding the impact

of increased impairment losses related to the creation of RCR, primarily

property and shipping exposures, which reduced return on equity by

3.1%.

Net interest income was 3% lower at £2,874 million, as increased income

from re-pricing initiatives was offset by the lower rate environment

impacting deposit returns, the non-repeat of 2012 deferred income

recognition revisions (£58 million) and reduced lending volumes, as loan

repayments coupled with run-off in property and shipping sectors

outpaced new lending.

Non-interest income reduced 9% to £1,593 million, primarily from lower

Markets revenue share income, a decline in operating lease income

(offset by an associated reduction of operating lease depreciation in

expenses), lower lending fees and higher derivative close-out costs

associated with impaired assets.

Expenses, increased 6% to £2,219 million, primarily as a result of

remediation provisions of £68 million, an increased share of branch

network costs and an uplift in investment spend. This was offset by the

reduction in operating lease depreciation, a decline in Markets revenue

share related costs and lower staff incentive expenditure.

Whilst full year impairments include the additional impact of increased

impairment losses related to the creation of RCR (£410 million),

underlying impairments improved by £60 million, or 7%, to £778 million

due to lower individual and collectively assessed provisions in the SME

business, partially offset by higher individual cases in the mid-to-large

corporate business.

Risk-weighted assets were broadly in line with 2012 at £86.1 billion as

reduced asset volumes and movements into default offset increases

resulting from the implementation of risk model changes.

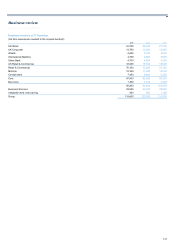

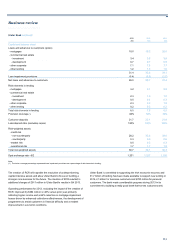

2012 compared with 2011

With economic factors continuing to suppress business confidence, 2012

saw lower income and operating profit. Nonetheless, the business

delivered a return on equity of 14.5%, slightly below the prior year and

comfortably ahead of the cost of capital.

Operating profit decreased by 7%, with income down 3% and increased

impairments, up 6%, partially offset by a 3% decrease in costs.

Net interest income was 4% lower, reflecting a 3% fall in lending volumes

as loan repayments outstripped new lending, deposit margin

compression due to strong competition and the continuation of low yields

on current accounts. This was partially offset by improved asset margins

and a 1% increase in deposit volumes.

Non-interest income was broadly in line with 2011, with stable income

from transaction services, asset finance, Markets revenue share and

other lending fees.

Total costs were down 3% due to tight control over direct discretionary

expenditure combined with lower indirect costs as a result of operational

savings, partially offset by increased investment expenditure.

Core lending balances were up £200 million, excluding the property,

housebuilding and construction sectors. The loan:deposit ratio decreased

by 400 basis points, principally reflecting deposit growth and portfolio de-

risking, particularly in commercial real estate. The Group took part in a

number of Government initiatives, seeking responsibly to stimulate

additional credit demand in the face of continued customer deleveraging

and low business confidence levels.

Impairments increased by 6% with lower specific provisions, mainly in the

SME business, more than offset by reduced levels of latent provision

releases across the division (£44 million in 2012 versus £226 million in

2011). Impairments as a percentage of loans and advances edged up

modestly to 80 basis points.

Risk-weighted assets increased by 9% as regulatory changes to capital

models during H2 2012 totalling £15 billion (primarily the implementation

of the market-wide slotting approach on real estate and increases to

default risk weights in other models) were partly offset by a fall in funded

assets.

Not reflected in operating results was UK Corporate’s £350 million share

of the provision for interest rate swap redress which relates to prior

periods, mainly pre-2008.