RBS 2013 Annual Report Download - page 314

Download and view the complete annual report

Please find page 314 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

304 -

305

305 -

306

306 -

307

307 -

308

308 -

309

309 -

310

310 -

311

311 -

312

312 -

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

312

Balance sheet analysis continued

REIL, provisions and AFS reserves continued

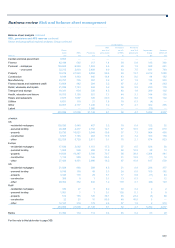

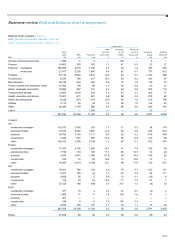

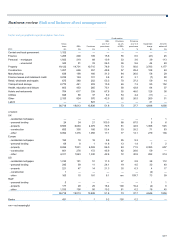

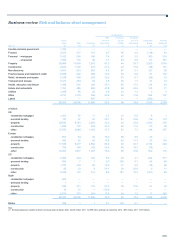

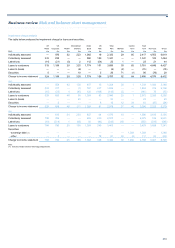

Potential problem loans

Potential problem loans (PPL) are loans for which an impairment event has taken place but no impairment loss is expected. This category is used for

advances which are not past due 90 days or revolving credit facilities where identification as 90 days overdue is not feasible.

2013 2012 2011

£m £m £m

Potential problem loans 789 807 739

Both REIL and PPL are reported gross and take no account of the value of any security held which could reduce the eventual loss should it occur, nor of

any provision marked. Therefore impaired assets which are highly collateralised, such as mortgages, will have a low coverage ratio of provisions held

against the reported impaired balance.

Past due analysis

The table below shows loans and advances to customers that were past due at the balance sheet date but are not considered impaired.

2013 2012 2011

Core Non-Core Total Core Non-Core Total Core Non-Core Total

£m £m £m £m £m £m £m £m £m

Past due 1-29 days 4,587 178 4,765 5,349 250 5,599 5,722 724 6,446

Past due 30-59 days 1,212 48 1,260 1,062 55 1,117 1,556 171 1,727

Past due 60-89 days 792 30 822 1,151 26 1,177 975 107 1,082

Past due 90 days or more 1,945 276 2,221 2,215 426 2,641 1,794 542 2,336

8,536 532 9,068 9,777 757 10,534 10,047 1,544 11,591

Past due analysis by sector*

Personal 4,982 190 5,172 5,198 303 5,501 6,819 741 7,560

Property and construction 1,075 298 1,373 1,475 388 1,863 1,126 651 1,777

Financial institution 366 2 368 92 11 103 83 6 89

Other corporate 2,113 42 2,155 3,012 55 3,067 2,019 146 2,165

8,536 532 9,068 9,777 757 10,534 10,047 1,544 11,591

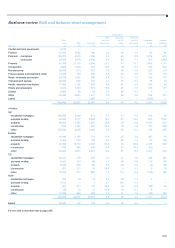

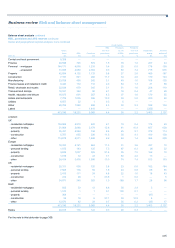

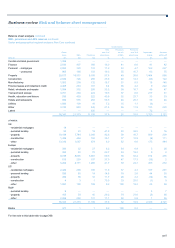

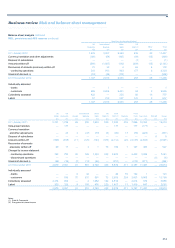

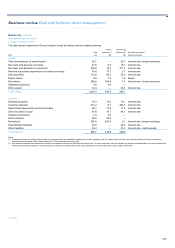

Impairment provisions flow statement

The movement in loan impairment provisions by division is shown in the table below.

UK UK International Ulster US Total Central Total

Retail Corporate Wealth Banking Bank R&C (1) R&C (1) Markets items Core Non-Core Group

£m £m £m £m £m £m £m £m £m £m £m £m

A

t 1 January 2013 2,629 2,432 109 391 3,910 285 9,756 305 1 10,062 11,200 21,262

Currency translation

and other adjustments 1 8 — (15) 51 31 76 5 — 81 28 109

Disposal of subsidiaries — — — — — — — — — — (77) (77)

A

mounts written-off (815) (772) (15) (281) (277) (284) (2,444) (46) — (2,490) (1,856) (4,346)

Recoveries of amounts

previously written-off 46 15 — 15 1 89 166 2 — 168 88 256

Charged to income statement

- continuing operations 319 1,188 29 219 1,774 151 3,680 21 65 3,766 4,646 8,412

Unwind of discount (2) (74) (38) (3) (4) (81) — (200) (1) — (201) (190) (391)

A

t 31 December 2013 2,106 2,833 120 325 5,378 272 11,034 286 66 11,386 13,839 25,225

Individually assessed

- banks — — — 1 — — 1 61 — 62 1 63

- customers — 1,462 109 207 2,078 60 3,916 214 66 4,196 12,650 16,846

Collectively assessed 1,929 1,096 — — 2,596 118 5,739 — — 5,739 565 6,304

Latent 177 275 11 117 704 94 1,378 11 — 1,389 623 2,012

2,106 2,833 120 325 5,378 272 11,034 286 66 11,386 13,839 25,225

For the notes to this table refer to page 314.

*unaudited