RBS 2013 Annual Report Download - page 416

Download and view the complete annual report

Please find page 416 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

406 -

407

407 -

408

408 -

409

409 -

410

410 -

411

411 -

412

412 -

413

413 -

414

414 -

415

415 -

416

416 -

417

417 -

418

418 -

419

419 -

420

420 -

421

421 -

422

422 -

423

423 -

424

424 -

425

425 -

426

426 -

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Notes on the consolidated accounts

414

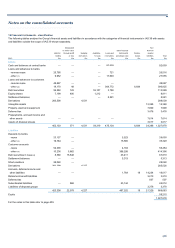

11 Financial instruments - valuation continued

The Group uses consensus prices for the source of independent pricing

for some instruments. The consensus service encompasses the equity,

interest rate, currency, commodity, credit, property, fund and bond

markets, providing comprehensive matrices of vanilla prices and a wide

selection of exotic products. Markets and Non-Core contribute to

consensus pricing services where there is a significant interest either

from a positional point of view or to test models for future business use.

Data sourced from consensus pricing services is used for a combination

of control processes including direct price testing, evidence of

observability and model testing. In practice this means that the Group

submits prices for all material positions for which a service is available.

Data from consensus services are subject to the same level of quality

review as other inputs used for IPV process.

In order to determine a reliable fair value, where appropriate,

management applies valuation adjustments to the pricing information

gathered from the above sources. The sources of independent data are

reviewed for quality and are applied in the IPV processes using a

formalised input quality hierarchy. These adjustments reflect the Group's

assessment of factors that market participants would consider in setting a

price. Furthermore, on an ongoing basis, the Group assesses the

appropriateness of any model used. To the extent that the price provided

by internal models does not represent the fair value of the instrument, for

instance in highly stressed market conditions, the Group makes

adjustments to the model valuation to calibrate to other available pricing

sources.

Where unobservable inputs are used, the Group may determine a range

of possible valuations derived from differing stress scenarios to determine

the sensitivity associated with the valuation. When establishing the fair

value of a financial instrument using a valuation technique, the Group

considers adjustments to the modelled price which market participants

would make when pricing that instrument. Such adjustments include the

credit quality of the counterparty and adjustments to compensate for

model limitations.

Valuation reserves

When valuing financial instruments in the trading book, adjustments are

made to mid-market valuations to cover bid-offer spread, liquidity and

credit risk. The valuation framework used to determine the fair value of

uncollateralised derivative exposures was refined during the year in line

with market developments. The weightings applied to the expected

losses and gains in the credit valuation adjustments (CVA) and own

credit adjustments (OCA) calculations have been removed. Funding

valuation adjustments (FVA) now reflect the counterparty contingent

nature of the exposures. FVA is also now considered the primary

adjustment applied to liabilities; the extent to which OCA and FVA

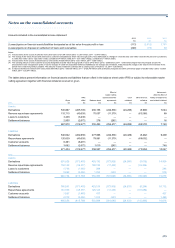

overlap is eliminated from OCA. The following table shows CVA and

other valuation reserves.

Credit valuation adjustments

Credit valuation adjustments represent an estimate of the adjustment to

fair value that a market participant would make to incorporate the

counterparty credit risk inherent in derivative exposures.

2013 2012 2011

£m £m £m

Credit valuation adjustments

- monoline insurers and credit derivative product companies (CDPC) 99 506 2,232

- other counterparties 1,667 2,308 2,254

1,766 2,814 4,486

Other valuation reserves

- bid-offer 513 625 806

- funding valuation adjustment 424 475 552

- product and deal specific 745 763 1,040

- other 8 134 306

1,690 1,997 2,704

Valuation reserves 3,456 4,811 7,190

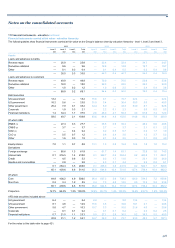

The table below analyses CVA relating to other counterparties by rating and sector.

2013

Ratings: £m

A

AA 104

A

A to AA+ 13

A

to AA- 168

BBB- to A- 446

Non-investment grade 936

1,667

Sector:

Banks 89

Other financial institutions 199

Corporate 1,126

Government 253

1,667