RBS 2013 Annual Report Download - page 434

Download and view the complete annual report

Please find page 434 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

424 -

425

425 -

426

426 -

427

427 -

428

428 -

429

429 -

430

430 -

431

431 -

432

432 -

433

433 -

434

434 -

435

435 -

436

436 -

437

437 -

438

438 -

439

439 -

440

440 -

441

441 -

442

442 -

443

443 -

444

444 -

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

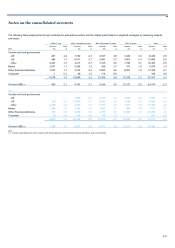

Notes on the consolidated accounts

432

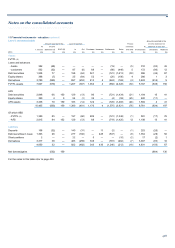

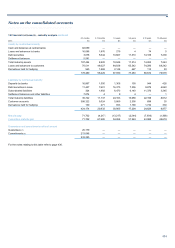

11 Financial instruments - valuation continued

2012 2012 2011 2011

Carrying value Fair value Carrying value Fair value

£bn £bn £bn £bn

Financial assets

Cash and balances at central banks 79.3 79.3 79.3 79.3

Loans and advances to banks 17.3 17.3 28.3 28.2

Loans and advances to customers 405.1 385.4 436.2 406.3

Debt securities 4.5 4.0 6.1 5.5

Settlement balances 5.7 5.7 7.8 7.8

Financial liabilities

Deposits by banks 34.5 34.5 51.3 50.7

Customer accounts 420.7 421.0 417.5 417.6

Debt securities in issue 60.1 59.8 115.4 112.7

Settlement balances 5.9 5.9 7.5 7.5

Notes in circulation 1.7 1.7 1.7 1.7

Subordinated liabilities 25.6 24.3 25.4 19.2

The fair value is the price that would be received to sell an asset or paid

to transfer a liability in an orderly transaction between market participants

at the measurement date. Quoted market values are used where

available; otherwise, fair values have been estimated based on

discounted expected future cash flows and other valuation techniques.

These techniques involve uncertainties and require assumptions and

judgments covering prepayments, credit risk and discount rates.

Furthermore there is a wide range of potential valuation techniques.

Changes in these assumptions would significantly affect estimated fair

values. The fair values reported would not necessarily be realised in an

immediate sale or settlement.

The fair values of intangible assets, such as core deposits, credit card

and other customer relationships are not included in the calculation of

these fair values as they are not financial instruments.

The assumptions and methodologies underlying the calculation of fair

values of financial instruments at the balance sheet date are as follows:

For certain short-term financial instruments: cash and balances at central

banks, items in the course of collection from other banks, settlement

balances, items in the course of transmission to other banks, customer

demand deposits and notes in circulation, fair value approximates to

carrying value.

Loans and advances to banks and customers

In estimating the fair value of loans and advances to banks and

customers measured at amortised cost, the Group’s loans are

segregated into appropriate portfolios reflecting the characteristics of the

constituent loans. Two principal methods are used to estimate fair value:

(a) Contractual cash flows are discounted using a market discount rate

that incorporates the current spread for the borrower or where this is

not observable, the spread for borrowers of a similar credit standing.

This method is used for portfolios where counterparties have external

ratings: large corporate loans in UK Corporate and institutional and

corporate lending in International Banking and Markets.

(b) Expected cash flows (unadjusted for credit losses) are discounted at

the current offer rate for the same or similar products. This approach

is adopted for lending portfolios in UK Retail, Ulster Bank, US Retail

& Commercial and Wealth and SME loans in UK Corporate reflecting

the homogeneous nature of these portfolios.

For certain portfolios where there are very few or no recent transactions,

such as Ulster Bank’s portfolio of lifetime tracker mortgages, a bespoke

approach is used based on available market data.

Debt securities

Fair values are determined using discounted cash flow valuation

techniques.

Deposits by banks and customer accounts

Fair values of deposits are estimated using discounted cash flow

valuation techniques.

Debt securities in issue and subordinated liabilities

Fair values are determined using quoted prices where available or by

reference to valuation techniques, adjusting for own credit spreads where

appropriate.