RBS 2013 Annual Report Download - page 323

Download and view the complete annual report

Please find page 323 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

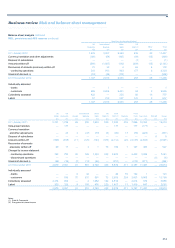

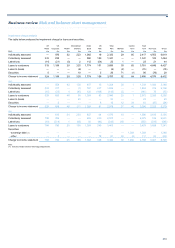

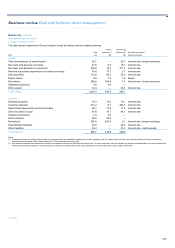

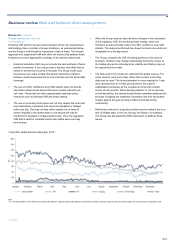

Business review Risk and balance sheet management

321

Governance structure

For general information on risk governance in the Group, see the Risk

governance section on pages 176.

The Group Chief Risk Officer (CRO) delegates responsibility for day-to-

day control of market risk to the traded and non-traded market risk

functions. Responsibility for controlling market risk in divisions is

delegated to divisional market risk functions, the heads of which are

accountable to divisional CROs, who in turn are accountable to the Group

CRO.

Risk management

Frameworks and processes common to both traded and non-traded

market risk management are described in this sub-section. Separate sub-

sections on traded and non-traded market risk follow, which provide more

detailed information specific to the management and measurement of

these two risk types.

Risk appetite and limit framework*

Market risk appetite is the level of market risk that the Group accepts

when pursuing its business objectives, taking into account both projected

and stressed scenarios. The Group has a comprehensive structure and

controls in place aimed at ensuring that this appetite is not exceeded.

The Group’s qualitative market risk appetite is set out in policy

statements. These define the governance, responsibilities, control

framework and requirements for the identification, measurement,

analysis, management and reporting of market risk arising from the

Group’s trading and non-trading activities. These policies are also

cascaded, as appropriate, to the Group’s legal entities, divisions and

businesses to ensure there is a consistent control framework throughout.

Group market risk limits that express its market risk appetite in

quantitative terms for trading and non-trading activities are proposed by,

respectively, the heads of traded and non-traded market risk. Once

approved by the ERF, these limits establish a set of comprehensive

boundaries within which business activities are conducted and monitored.

The heads of traded and non-traded market risk cascade the Group

market risk limits down to the legal entities and divisions. The divisional

market risk functions are responsible for cascading legal entity and

divisional market risk limits to lower levels as appropriate.

The limit framework comprises not only Group limits but also legal entity,

divisional and lower level limits and aims to capture all material market

risks arising from the Group’s activities.

The limit framework at the Group level comprises Value at Risk (VaR),

Stressed Value at Risk (SVaR), sensitivity and stress limits (for more

details on VaR and SVaR, see pages 323 and 328). The limit framework

at the divisional, legal entity and lower levels also comprises additional

metrics that are specific to the market risk exposures within its scope.

These additional metrics aim to control various risk dimensions such as

product type, exposure size, aged inventory, currency and tenor.

The limits are reviewed to reflect changes in risk appetite, business

plans, portfolio composition and the market and economic environments.

*unaudited

Limit breaches at the Group level require escalation by the head of traded

market risk or the head of non-traded market risk, as appropriate, to the

ERF and the Group CRO. Limit breaches at the divisional or legal entity

level require escalation by the head of the relevant divisional market risk

function to the head of traded market risk or the head of non-traded

market risk, as appropriate.

Valuation and independent price verification

Traders are responsible for marking-to-market their trading book

positions daily, ensuring that assets and liabilities in the trading book are

measured at their fair value. Any profits or losses on the revaluation of

positions are recognised daily.

Business unit controllers are responsible for ensuring that independent

price verification processes are in place covering all trading book

positions held by their business. Independent price verification is the key

control over front office marking of positions.

For more information on valuation controls, refer to page 412. The

validation of pricing models is discussed below.

Model validation

This sub-section discusses the independent model validation framework

governing both pricing models and risk models (including Value-at-Risk).

The Group uses a variety of models to manage and measure market risk,

as described below. These models comprise pricing models (used for

valuation of positions) and risk models (for risk measurement and capital

calculation purposes). They are developed in both divisional units and

Group functions and are subject to independent review and sign-off.

The Group has a dedicated independent model review and challenge

function - Group Risk Analytics (GRA) - which performs reviews of

relevant models in two instances: (i) for new models or amendments to

existing models and (ii) as part of its ongoing programme to assess the

performance of these models.

A new model is typically introduced when an existing model is no longer

fit for purpose or a new product requires a new methodology or model to

quantify the risk appropriately. Amendments are usually made when a

weakness is identified during use of a model or following analysis either

by the model developers in the divisions or by GRA.

GRA also reassesses the appropriateness of approved models following

significant market or regulatory developments or portfolio changes. The

mechanics of the review process are the same as those for new models.

Pricing models*

Pricing models are developed by a dedicated front office team, in

conjunction with the trading desk. They are used for the valuation of

positions for which prices are not directly observable and for the risk

management of the portfolio.

Any pricing models that are used as the basis for valuing books and

records are subject to approval and oversight by asset-level modelled

product review committees.