RBS 2013 Annual Report Download - page 274

Download and view the complete annual report

Please find page 274 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

272

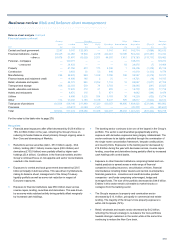

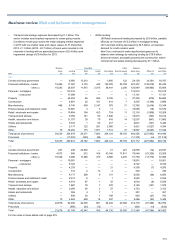

Balance sheet analysis continued

Financial assets continued

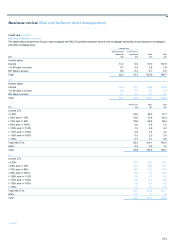

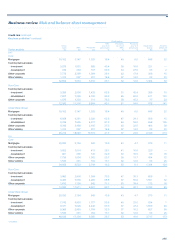

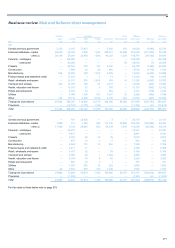

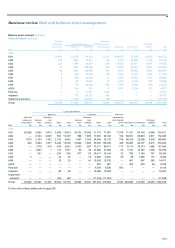

Reverse Securities Other Balance Exposure

repos Lending Debt Equity Derivatives financial assets sheet value Offset (1) post offset

2011 £m £m £m £m £m £m £m £m £m

Central and local government 2,247 9,742 125,543 — 5,541 641 143,714 (1,098) 142,616

Financial institutions - banks 39,345 44,080 16,940 2,218 400,261 79,396 582,240 (407,457) 174,783

- other (2) 58,478 51,870 60,628 2,501 98,255 7,451 279,183 (119,717) 159,466

Personal - mortgages — 149,273 — — — — 149,273 — 149,273

- unsecured — 34,424 — — — 52 34,476 (7) 34,469

Property — 81,058 573 175 4,599 1 86,406 (1,274) 85,132

Construction — 9,869 50 53 946 — 10,918 (1,139) 9,779

Manufacturing 254 28,639 664 1,938 3,786 306 35,587 (2,214) 33,373

Finance leases and instalment credit — 14,499 145 2 75 — 14,721 (16) 14,705

Retail, wholesale and repairs — 24,378 645 2,652 1,134 18 28,827 (1,671) 27,156

Transport and storage 436 22,058 539 74 3,759 — 26,866 (241) 26,625

Health, education and leisure — 17,492 310 21 885 — 18,708 (973) 17,735

Hotels and restaurants — 8,870 116 5 671 — 9,662 (184) 9,478

Utilities — 8,406 1,530 554 3,708 30 14,228 (450) 13,778

Other 174 33,490 3,785 5,136 6,437 595 49,617 (1,003) 48,614

Total gross of provisions 100,934 538,148 211,468 15,329 530,057 88,490 1,484,426 (537,444) 946,982

Provisions — (20,674) (2,388) (141) — — (23,203) n/a (23,203)

Total 100,934 517,474 209,080 15,188 530,057 88,490 1,461,223 (537,444) 923,779

For the notes to this table refer to page 278.

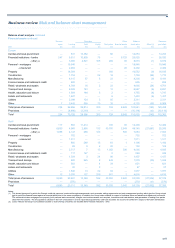

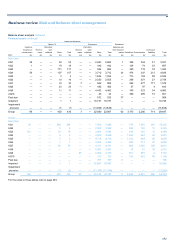

Key points

• Financial asset exposures after offset decreased by £129.4 billion or

16% to £684.3 billion in the year, reflecting the Group’s focus on

reducing its funded balance sheet primarily through ongoing sales in

Non-Core and downsizing of Markets.

• Reductions across securities (debt - £51.0 billion; equity - £6.4

billion), lending (£43.1 billion) reverse repos (£28.4 billion) and

derivatives (£153.9 billion) were partially offset by higher cash

holdings (£3.4 billion). Conditions in the financial markets and the

Group’s continued focus on risk appetite and sector concentrations

resulted in the trends seen.

• Exposures to central and local government decreased by £29.5

billion principally in debt securities. This was driven by Markets de-

risking its balance sheet, management of the Group Treasury

liquidity portfolio as well as some risk reduction in respect of

Eurozone exposures.

• Exposure to financial institutions was £59.4 billion lower across

reverse repos, lending, securities and derivatives. This was driven

by economy-wide subdued activity being partially offset marginally

by increased cash holdings.

• The banking sector continues to be one of the largest in the Group’s

portfolio. The sector is well diversified geographically and by

exposure with derivative exposures being largely collateralised. The

sector continues to be tightly controlled through the combination of

the single name concentration framework, bespoke credit policies

and country limits. Exposures to the banking sector decreased by

£14.8 billion during the year with decreases across, reverse repos

lending, securities and derivatives being partially offset by increased

cash holdings with central banks.

• Exposure to other financial institutions comprising traded and non-

traded products is spread across a wide range of financial

companies including insurance, securitisation vehicles, financial

intermediaries including broker dealers and central counterparties,

financial guarantors - monolines and credit derivative product

companies - and funds comprising unleveraged, hedge and

leveraged funds. The size of the portfolio decreased by £44.6 billion.

Entities in this sector remain vulnerable to market shocks or

contagion from the banking sector.

• The Group’s exposure to property and construction sector

decreased by £13.1 billion, principally in commercial real estate

lending. The majority of the Group’s Core property exposure is

within UK Corporate (72%).

• Retail, wholesale and repairs sector decreased by £4.2 billion,

reflecting the Group’s strategy to re-balance the Core portfolios

towards stronger customers in the sector while at the same time

continuing to reduce the Non-Core book.