RBS 2013 Annual Report Download - page 418

Download and view the complete annual report

Please find page 418 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

408 -

409

409 -

410

410 -

411

411 -

412

412 -

413

413 -

414

414 -

415

415 -

416

416 -

417

417 -

418

418 -

419

419 -

420

420 -

421

421 -

422

422 -

423

423 -

424

424 -

425

425 -

426

426 -

427

427 -

428

428 -

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Notes on the consolidated accounts

416

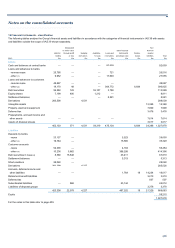

11 Financial instruments - valuation continued

Bid-offer, liquidity and other reserves

Fair value positions are adjusted to bid or offer levels, by marking

individual cash positions directly to bid or offer or by taking bid-offer

reserves calculated on a portfolio basis for derivatives exposures. The

bid-offer approach is based on current market spreads and standard

market bucketing of risk.

Risk data are used as the primary sources of information within bid-offer

calculations and are aggregated when they are more granular than

market standard buckets. Bid-offer adjustments for each risk factor

(including delta (the degree to which the price of an instrument changes

in response to a change in the price of the underlying), vega (the degree

to which the price of an instrument changes in response to the volatility in

the price of the underlying), correlation (the degree to which prices of

different instruments move together)) are determined by aggregating

similar risk exposures arising on different products. Additional basis bid-

offer reserves are taken where these are charged in the market. Risk

associated with non-identical underlying exposures is not netted down

unless there is evidence that the cost of closing the combined risk

exposure is less than the cost of closing on an individual basis.

Bid-offer spreads vary by maturity and risk type to reflect different

spreads in the market. For positions where there is no observable quote,

the bid-offer spreads are widened in comparison to proxies to reflect

reduced liquidity or observability. Bid-offer methodologies may also

incorporate liquidity triggers whereby wider spreads are applied to risks

above pre-defined thresholds.

As permitted by IFRS 13, netting is applied on a portfolio basis to reflect

the value at which the Group believes it could exit the portfolio, rather

than the sum of exit costs for each of the portfolio’s individual trades. This

is applied where the asset and liability positions are managed as a

portfolio for risk and reporting purposes. For example, netting is applied

where long and short risk in two different maturity buckets can be closed

out in a single market transaction at less cost than by way of two

separate transactions (calendar netting). This reflects the fact that to

close down the portfolio, the net risk can be settled rather than each long

and short trade individually.

Vanilla risk on exotic products is typically reserved as part of the overall

portfolio based calculation e.g. delta and vega risk on exotic products are

included within the delta and vega bid-offer calculations. Aggregation of

risk arising from different models is in line with the Group's risk

management practices; the model review control process considers the

appropriateness of model selection in this respect.

Product related risks such as correlation risk, attract specific bid-offer

reserves. Additional reserves are provided for exotic products to ensure

overall reserves match market close-out costs. These market close-out

costs inherently incorporate risk decay and cross-effects (taking into

account how changes in one risk factor may affect other inputs rather

than treating all risk factors independently) that are unlikely to be

adequately reflected in a static hedge based on vanilla instruments.

Where there is limited bid-offer information for a product, the pricing

approach and risk management strategy are taken into account when

assessing the reserve.

The discount rates applied to derivative cash-flows in determining fair

value reflect any underlying collateral agreements. Collateralised

derivatives are generally discounted at the relevant OIS rates at an

individual trade level. Uncollateralised derivatives are discounted with

reference to funding levels by applying a funding spread over benchmark

interest rates on a portfolio basis (funding valuation adjustment).

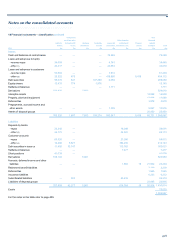

Funding valuation adjustment (FVA)

Funding valuation adjustments represent an estimate of the adjustment to

fair value that a market participant would make to incorporate funding

costs and benefits that arise in relation to uncollateralised derivative

exposures.

Funding levels are applied to estimated potential future exposures, the

modelling of which is consistent with the approach used in the calculation

of CVA relating to Other counterparties. The counterparty contingent

nature of the exposures is now reflected in the calculation.

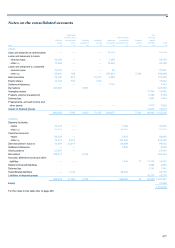

Amounts deferred on initial recognition

On initial recognition of financial assets and liabilities valued using

valuation techniques incorporating information other than observable

market data, any difference between the transaction price and that

derived from the valuation technique is deferred. Such amounts are

recognised in profit or loss over the life of the transaction; when market

data becomes observable; or when the transaction matures or is closed

out as appropriate. At 31 December 2013, net gains of £205 million (2012

- £153 million; 2011 - £161 million) were carried forward. During the year,

net gains of £134 million (2012 - £39 million; 2011 - £89 million) were

deferred and £82 million (2012 - £47 million; 2011 - £95 million)

recognised in the income statement.

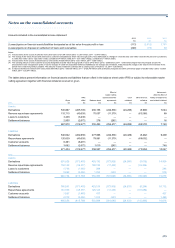

Own credit

The Group takes into account the effect of its own credit standing when

valuing financial liabilities recorded at fair value in accordance with IFRS.

Own credit spread adjustments are made when valuing issued debt held

at fair value, including issued structured notes, and derivatives. An own

credit adjustment is applied to positions where it is believed that

counterparties would consider the Group's creditworthiness when pricing

trades.

For issued debt and structured notes this adjustment is based on debt

issuance spreads above average inter-bank rates (at a range of tenors).

Secondary senior debt issuance spreads are used in the calculation of

the own credit adjustment applied to senior debt.

The fair value of the Group's derivative financial liabilities has also been

adjusted to reflect the Group's own credit risk (DVA). Expected gains are

applied to estimated potential future negative exposures, the modelling of

which is consistent with the approach used in calculation of CVA relating

to Other counterparties. Expected gains are determined from market

implied probabilities of default and recovery levels. Weightings that were

previously applied in the expected gains calculation were removed during

the period in line with market developments. FVA is also now considered

the primary adjustment applied to derivative liabilities; the extent to which

DVA and FVA overlap is eliminated from DVA.

The own credit adjustment for fair value does not alter cash flows, is not

used for performance management, is disregarded for regulatory capital

reporting processes and will reverse over time as the liabilities mature.