RBS 2013 Annual Report Download - page 248

Download and view the complete annual report

Please find page 248 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

246

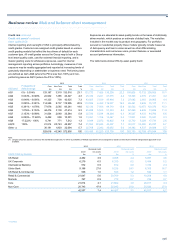

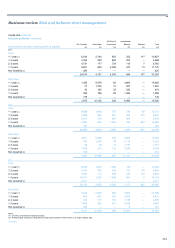

Credit risk continued

Early problem identification and problem debt management continued

Unsecured portfolios

For unsecured portfolios in UK Retail and Ulster Bank, forbearance

entails reduced or deferred payments. Arrangements to facilitate the

repayment of overdraft excesses or loan arrears can be agreed

dependent on affordability. Where repayment arrangements are not

affordable debt consolidation loans can be provided to customers in

collections.

In RBS Citizens, granting of forbearance is predominantly restricted to

short-term (1-3 months) loan extensions to alleviate the financial burden

caused by temporary hardship. Such extensions are offered only if a

customer has demonstrated a capacity and willingness to pay. The

number and frequency of extensions granted to a customer are limited.

Additionally, for loans secured by vehicles and credit cards, RBS Citizens

may offer temporary interest rate modifications, but no principal

reductions. Forbearance may also be offered to student loan customers

consistent with the policy guidelines of the US Office of the Comptroller of

the Currency.

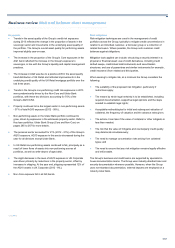

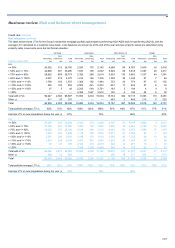

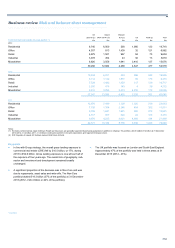

• For unsecured portfolios in UK Retail, £121 million of balances (1%

of the total unsecured balances) were subject to forbearance at

2013 year end.

• For unsecured portfolios in Ulster Bank, £16 million (3.8% by value)

of the population was subject to forbearance at 31 December 2013.

• For unsecured portfolios in RBS Citizens, £135 million (1.7% of the

unsecured balances) were subject to forbearance at 2013 year end

(includes auto and recreational vehicle marine portfolios and

excludes small business loans as these are included as part of

wholesale reporting).

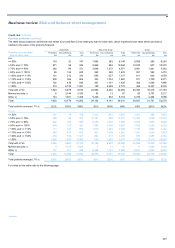

Monitoring of forbearance

Forbearance loans may be performing or non-performing. The granting of

forbearance does not change the delinquency status of the loan unless

the arrangement involves a capitalisation of all existing arrears of

principal and interest, in which case the loan becomes up-to-date.

Loans granted forbearance are included in the non-performing book:

when 90 days past due; or if the forbearance arrangement is a payment

concession that involves a reduction in contractually required cash flows

i.e. the forgiveness of interest. Such loans are classified as impaired. In

RBS Citizens, all loans subject to forbearance are included in the non-

performing book.

There are instances when loans subject to forbearance are transferred

from the non-performing book to the performing book. In UK Retail, when

arrears are capitalised, a loan is transferred to the performing book once

the borrower has met the revised payment terms for at least six months

and is expected to continue to do so. In addition, a small portfolio of loans

past due 90 days are managed by UK Retail’s collections function.

Loans in this portfolio may also be transferred to the performing book if

the customer makes payments that reduce arrears below 90 days.

In Ulster Bank, if a customer makes payments that reduce loan arrears

below 90 days, the loan is transferred to the performing book. In addition,

where a customer meets the original payment terms for six months and is

expected to continue to do so, capitalisation may be agreed. In these

cases the loan is also transferred to the performing book.

Mortgages granted forbearance are reviewed regularly to ensure that

customers are meeting the agreed terms. Key metrics have been

developed to record the proportion of loans that fail to meet the agreed

terms over time, as well as the proportion of loans that return to

performing with no arrears. Retail forbearance loans can be modified

more than once.

Twelve month default rates are calculated for all mortgage forbearance

types. In 2013, the average twelve month default rates were 8% for UK

Retail, 18% for Ulster Bank and 13% for RBS Citizens.