RBS 2013 Annual Report Download - page 214

Download and view the complete annual report

Please find page 214 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

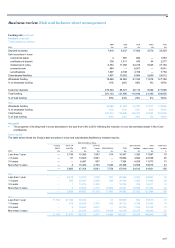

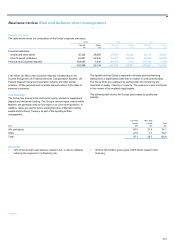

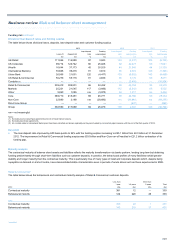

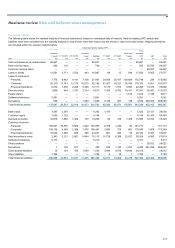

Business review Risk and balance sheet management

212

Liquidity risk continued

Stress testing and contingency planning*

Liquidity stress tests apply scenario-based behavioural and contractual

assumptions to cash inflows and outflows to assess the level of liquidity

reserves required under a particular scenario.

A stress event can occur when either firm-specific or market-wide factors

or a combination of both lead to depositors and investors to withdraw or

not to renew funding on maturity. This could be caused by many factors

including fears over the viability of the firm. Additionally, liquidity stress

can be brought on by customers choosing to draw down on loan

agreements and facilities.

Simulated liquidity stress testing is performed at least quarterly for each

division as well as the major operating subsidiaries in order to evaluate

the strength of the Group’s liquidity risk management.

Stress tests are designed to examine the impact of a variety of firm-

specific and market-wide scenarios on the future adequacy of the

Group’s liquidity reserves. Stress test scenarios are designed to take into

account the Group’s experiences during the financial crisis, recent market

conditions and events. These scenarios can be run at any time in

response to the emergence of firm-specific or market-wide risks that

could have a material impact on the Group’s liquidity position. In the past

these have included credit rating changes and political and economic

conditions changing in particular countries.

In determining the adequacy of the Group’s liquidity resources the Group

focuses on the outflows it anticipates as a result of any stress scenario

occurring. These outflows are measured over certain time periods which

extend from two weeks to three months. The Group is expected to be

able to withstand these stressed outflows through its own resources

(primarily through the use of the liquidity portfolio) without having to resort

to extraordinary central bank or governmental assistance.

The Group’s liquidity risk appetite is measured by reference to the

liquidity portfolio as a percentage of stressed contractual and behavioural

outflows under the worst of three severe stress scenarios, as prescribed

by the PRA. These are a market-wide stress, an idiosyncratic stress and

a combination of both. At 31 December 2013, the Group’s liquidity

portfolio was 145% of the worst case stress requirements.

*unaudited

Key liquidity risk stress testing assumptions

• Net wholesale funding - Outflows at contractual maturity of

wholesale funding, with no rollover/new issuance, prime brokerage,

100% loss of excess client derivative margin and 100% loss of

excess client cash.

• Secured financing and increased haircuts - Loss of secured funding

capacity at contractual maturity date and incremental haircut

widening, depending upon collateral type.

• Retail and commercial bank deposits - Substantial outflows as the

Group could be seen as a greater credit risk than competitors.

• Intra-day cash flows - Liquid collateral held against intra-day

requirement at clearing and payment systems is regarded as

encumbered with no liquidity value assumed. Liquid collateral is held

against withdrawal of unsecured intra-day lines provided by third

parties.

• Intra-group commitments and support - Risk of cash within

subsidiaries becoming unavailable to the wider Group and

contingent calls for funding on Group Treasury from subsidiaries and

affiliates.

• Funding concentrations - Additional outflows recognised against

concentration of providers of wholesale secured financing.

• Off-balance sheet activities - Collateral outflows due to market

movements, and all collateral owed by the Group to counterparties

but not yet called; anticipated increase in firm’s derivative initial

margin requirement in stress scenarios; collateral outflows

contingent upon a multi-notch credit rating downgrade of Group

firms; drawdown on committed facilities provided to corporates,

based on counterparty type, creditworthiness and facility type; and

drawdown on retail commitments.

• Franchise viability - Group liquidity stress testing includes additional

liquidity in order to meet outflows that are non-contractual in nature,

but are necessary in order to support valuable franchise businesses.

• Management action - Unencumbered marketable assets that are

held outside of the Core liquidity portfolio and are of verifiable

liquidity value to the firm, are assumed to be monetised (subject to

haircut/valuation adjustment).

The Group has a Contingency Funding Plan (CFP), which is updated at

least annually and as the balance sheet evolves and forms the basis of

analysis and actions to remediate adverse events as and if they arise.

The CFP provides a detailed description of the availability, size and

timing of all sources of contingent liquidity available to the Group in a

stress event. These are ranked in order of economic impact and

effectiveness to meet the anticipated stress requirement. The CFP

includes documented processes for actions that may be required to meet

the outflows and specifies roles and responsibilities for the effective

implementation of the CFP.