RBS 2013 Annual Report Download - page 302

Download and view the complete annual report

Please find page 302 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

292 -

293

293 -

294

294 -

295

295 -

296

296 -

297

297 -

298

298 -

299

299 -

300

300 -

301

301 -

302

302 -

303

303 -

304

304 -

305

305 -

306

306 -

307

307 -

308

308 -

309

309 -

310

310 -

311

311 -

312

312 -

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

300

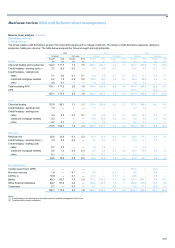

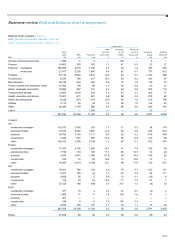

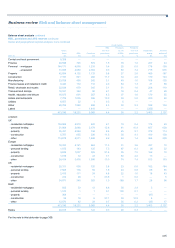

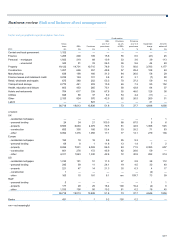

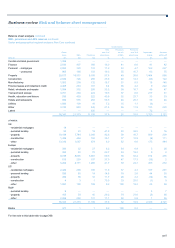

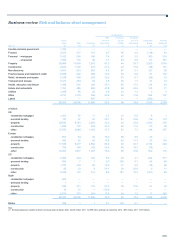

Balance sheet analysis continued

REIL, provisions and AFS reserves continued

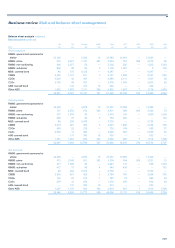

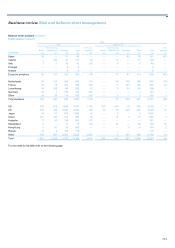

Credit metrics

REIL as a % Provisions

Gross loans to of gross loans as a % Impairment Amounts

Banks Customers REIL Provisions to customers of REIL charge written-off

2012 £m £m £m £m % % £m £m

UK Retail 695 113,599 4,569 2,629 4.0 58 529 599

UK Corporate 746 107,025 5,452 2,432 5.1 45 836 514

Wealth 1,545 17,074 248 109 1.5 44 46 15

International Banking 4,827 42,342 422 391 1.0 93 111 445

Ulster Bank 632 32,652 7,533 3,910 23.1 52 1,364 72

US Retail & Commercial 435 51,271 1,146 285 2.2 25 83 391

Retail & Commercial 8,880 363,963 19,370 9,756 5.3 50 2,969 2,036

Markets 16,805 29,787 396 305 1.3 77 25 109

Other 3,196 2,125 — 1 — — 1 —

Core 28,881 395,875 19,766 10,062 5.0 51 2,995 2,145

Non-Core 477 56,343 21,374 11,200 37.9 52 2,320 2,121

Direct Line Group 2,036 881 — — — — — —

Group 31,394 453,099 41,140 21,262 9.1 52 5,315 4,266

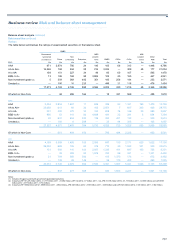

2011

UK Retail 628 110,659 4,599 2,679 4.2 58 788 823

UK Corporate 806 110,729 5,001 2,061 4.5 41 790 658

Wealth 2,422 16,913 211 81 1.2 38 25 11

International Banking 3,411 57,729 1,632 851 2.8 52 168 125

Ulster Bank 2,079 34,052 5,523 2,749 16.2 50 1,384 124

US Retail & Commercial 208 51,562 1,007 455 2.0 45 248 373

Retail & Commercial 9,554 381,644 17,973 8,876 4.7 49 3,403 2,114

Markets 29,991 31,490 414 311 1.3 75 — 23

Other 1,270 56 — — — — — —

Core 40,815 413,190 18,387 9,187 4.5 50 3,403 2,137

Non-Core 706 80,005 24,007 11,487 30.0 48 3,838 2,390

Direct Line Group 2,559 873 — — — — — —

Group 44,080 494,068 42,394 20,674 8.6 49 7,241 4,527

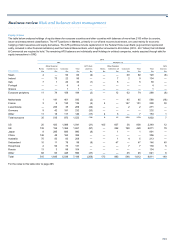

Key points

• The Group loan impairment charge for the year increased by 58%

(£3.1 billion) to £8.4 billion from £5.3 billion in 2012. The Core

charge increased 26% (£0.8 billion) to £3.8 billion and the Non-Core

charge increased by 100% (£2.3 billion) to £4.6 billion. £4.5 billion of

the impairment increase was in relation to the creation of RCR and

the related strategy, £1.4 billion in Core and £3.1 billion in Non-Core.

The underlying provision charge decreased £1.4 billion mainly in UK

Retail (£0.2 billion), Ulster Bank residential mortgages (£0.4 billion)

and Non-Core (£0.8 billion), largely due to run down and lower

single name charges in Non-Core.*

• REIL decreased by £1.7 billion to £39.4 billion during the year

mainly in Non-Core (£2.4 billion) and UK Retail (£1.0 billion) offset

by increases in UK Corporate (£0.8 billion) and Ulster Bank (£0.9

billion). REIL reductions in Non-Core primarily related to repayments

and write-offs in UK corporate and International Banking donated

portfolios.

*unaudited

• The RCR provision charge mainly related to loans already within

REIL resulting in an 12% increase in the provision coverage ratio to

64% from 52% at December 2012 while the REIL as a percentage of

total loans increased to 9.4% from 9.1% at 31 December 2012.*

• UK Retail REIL continued to decrease due to the write-off of aged

debt and the transfer of up-to-date mortgages to potential problem

loans. Provision coverage remained broadly stable at 59%.

• REIL in UK Corporate increased 14% mainly driven by individual

cases in the commercial real estate and shipping portfolios as credit

conditions remained difficult in these sectors. The impact of the RCR

related strategy resulted in a £0.4 billion provision increase in Q4

2013.*

• Ulster Bank REIL at £8.5 billion increased by 12% compared with 31

December 2012. The increase in REIL was largely in relation to

commercial real estate investment loans. RCR and related

provisioning in 2013 contributed £0.9 billion to the Core Ulster Bank

provision and has resulted in the provision coverage increasing from

52% to 64% in the year and in the fourth quarter.*