RBS 2013 Annual Report Download - page 252

Download and view the complete annual report

Please find page 252 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

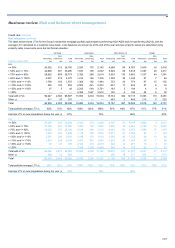

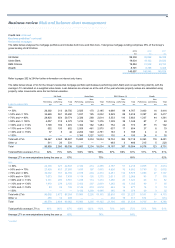

Business review Risk and balance sheet management

250

Credit risk continued

Early problem identification and problem debt management continued

Recoveries

Once a loan has been identified as impaired it is managed by divisional

recoveries functions. Their goal is to collect the total outstanding and

reduce the Group’s loss by maximising cash recovery while treating

customers fairly. Where an acceptable repayment arrangement cannot

be agreed with the customer, litigation may be considered. In UK Retail

and Northern Ireland, no repossession procedures are initiated until at

least six months following the emergence of arrears. In the Republic of

Ireland, new regulations prohibit taking legal action for an extended

period. Additionally, certain forbearance options are made available to

customers managed by the recoveries function.

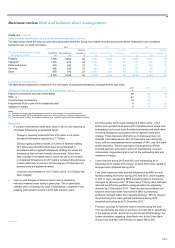

Group impairment loss provisioning

Impaired definition

A financial asset is impaired if there is objective evidence that an event or

events since initial recognition of the asset, has adversely affected the

amount or timing of future cash flows from it. The loss is measured as the

difference between the carrying value of the loan and the present value of

estimated future cash flows discounted at the loan’s original effective

interest rate.

For both wholesale and retail exposures, days-past-due measures are

typically used to identify evidence of impairment. In both corporate and

retail portfolios, a period of 90 days past due is used. In sovereign

portfolios, the period used is 180 days past due. Other factors are

considered including: the borrower’s financial condition; a forbearance

event; a loan restructuring; the probability of bankruptcy; or any evidence

of diminished cash flows.

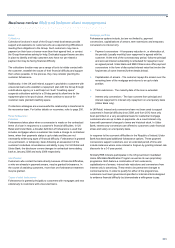

Provisioning methodology

If there is objective evidence that an impairment loss has been incurred,

the amount of the loss is measured as the difference between the asset

carrying amount and the present value of the estimated future cash flows

discounted at the financial asset’s original effective interest rate. The

current net realisable value of the collateral will be taken into account in

determining the need for a provision. No impairment provision is

recognised in cases where amounts due are expected to be settled in full

on realisation of the security. The Group uses one of the following three

different methods to assess the amount of provision required: individual;

collective; and latent.

Individually assessed provisions

Loans and securities above a defined threshold deemed to be individually

significant are assessed on a case-by-case basis. Assessments of future

cash flows take into account the impact of any guarantees or collateral

held. Projections of cash flow receipts are based on the Group’s

judgement and facts available at the time. Projected cash flows are

reviewed on subsequent assessment dates as new information becomes

available.

Collectively assessed provisions

Provisions on impaired credits below an agreed threshold are assessed

on a portfolio basis, reflecting the homogeneous nature of the assets.

The Group segments wholesale and retail portfolios according to product

type, such as credit cards, personal loans and mortgages. The approach

taken to assess impaired assets in collections differs from the

approach taken to assess those in recoveries (refer to page 245 for

further details on collections and refer to above for recoveries).

Provisions are determined based on a quantitative review of the relevant

portfolio. They take account of the level of arrears, the value of any

security, and historical and projected cash recovery trends over the

recovery period. The provisions also incorporate any adjustments that

may be deemed appropriate given current economic conditions. Such

adjustments may be determined based on a review of the latest cash

collections profile and operational processes used in managing

exposures.

Latent loss provisions

In the performing portfolio, latent loss provisions are held against losses

incurred but not identified before the balance sheet date. Latent loss

provisions reflect PDs and LGDs as well as emergence periods. The

emergence period is defined as the period between the occurrence of the

impairment event and a loan being identified and reported as impaired.

Emergence periods are estimated at a portfolio level and reflect the

portfolio product characteristics such as coupon period and repayment

terms, and the duration of the administrative process required to report

and identify an impaired loan as such. Emergence periods vary across

different portfolios from 2 to 225 days. They are based on actual

experience within the particular portfolio and are reviewed regularly.

The Group’s retail businesses segment their performing loan books into

homogeneous portfolios such as mortgages, credit cards or unsecured

loans, to reflect their different credit characteristics. Latent provisions are

computed by applying portfolio level LGDs, PDs and emergence periods.

The wholesale calculation is based on similar principles but there is no

segmentation into portfolios. PDs and LGDs are calculated on an

individual basis.

Refer to pages 299 to 317 for analysis of impaired loans, related

provisions and impairments.