RBS 2013 Annual Report Download - page 196

Download and view the complete annual report

Please find page 196 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

194

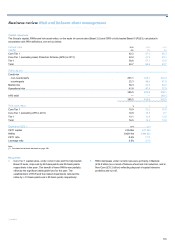

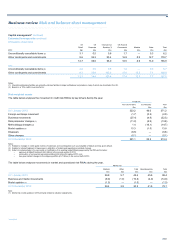

Capital management* continued

Governance continued

Determining appropriate capital

The Group’s own determination of sufficient capital is derived from the

desired credit rating, risk appetite and reflects the current and emerging

regulatory requirements of the Group. It is evaluated through both

internally and externally defined stress testing to identify potential

changes in capital ratios in a range of scenarios.

Basel II requires RWAs to be calculated for credit, market and operational

risk with various approaches available to banks, with differing levels of

sophistication. The minimum capital requirement is calculated as 8% of

RWAs.

The Group identifies the management and recovery actions that could be

applied in stress environments. These form an important part of the

capital management approach and the contingency planning

arrangements, complementing the established buffers.

Monitoring and maintenance

Based on these determinations, which are continually reassessed, the

Group aims to maintain capital adequacy, both at Group level and in each

regulated entity.

The Group operates a rigorous capital planning process aimed at

ensuring the capital position is controlled within the agreed parameters.

This incorporates regular re-forecasts of the capital positions of the

regulated entities and the overall Group. In the event that the projected

position might deteriorate beyond acceptable levels, the Group would

issue further capital and/or revise business plans accordingly.

Stress testing approaches are used to determine the level of capital

required to ensure the Group expects to remain adequately capitalised.

Minimising surplus profits and capital

The Group has a process in place which requires surplus distributable

profits of all Group subsidiaries, after making allowance for sufficient

capital to support current and prospective growth in the following half-

year, to be repatriated by way of a dividend on a half yearly basis and

paid in cash before the period end. Surplus is defined as subsidiary

capital of more than £1 million in excess of the regulatory minimum for

UK banks and in accordance with the Group's policy, including capital

buffers, or the industry specific/overseas regulatory requirements.

However, fungibility of capital is subject to the approval of the local

regulator.

*unaudited

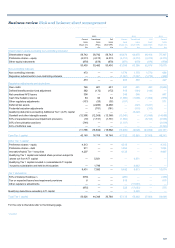

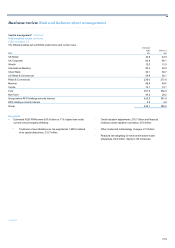

Capital allocation

Capital resources are allocated to the Group’s businesses based on key

performance parameters agreed by the Group Board in the annual

strategic planning process. Principal among these is a profitability metric,

which assesses the effective use of the capital allocated to the business.

Projected and actual return on equity is assessed against target returns

set by the Group Board. The allocations also reflect strategic priorities,

the intensity of regulatory capital use and the usage of other key Group

resources such as balance sheet liquidity and funding.

Economic profit is also planned and measured for each division during

the annual planning process. It is calculated by deducting the cost of

equity utilised in the particular business from its operating profit and

measures the value added over and above the cost of equity.

The Group aims to deliver sustainable returns across the portfolio of

businesses with projected business returns stressed to test key

vulnerabilities.

The divisions use return on capital metrics when making pricing decisions

on products and transactions, to ensure customer activity is appropriately

aligned with Group and divisional targets and allocations.

The PRA uses the risk asset ratio as a measure of capital adequacy in

the UK banking sector, comparing a bank’s capital resources with its

RWAs (the assets and off-balance sheet exposures are weighted to

reflect the inherent credit and other risks).

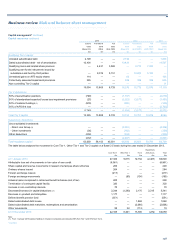

Economic capital

Economic capital is an internal measure of the risks to which the Group is

exposed and is used as a supplement to other risk and capital tools, such

as stress testing and regulatory capital. The measure includes risk

exposures for credit, market, business, operational, pension, fixed asset

and interest rate risk in the banking book. These models capture risks not

fully addressed within the Pillar 1 regulatory framework e.g.

concentration, pension, interest rate, business risk and diversification.

The characteristics of the models are consistent across risks, business

lines and throughout the economic cycle, but are also flexible to allow

outcomes to be employed for a number of purposes e.g. severity

level/confidence interval, time horizon and correlations. Models have

been developed internally but are subject to rigorous governance

including external benchmarking, independent validation and extensive

internal review and challenge. Models are regularly reviewed and

continue to be updated for new data sources and improvements in risk

modelling methodology.

The ability to change severity levels supports management of earnings

volatility and capital risk. Economic models are used in the Internal

Capital Adequacy Assessment Process, assessing risk profiles within the

risk appetite framework, functional risk management e.g. credit

exposures at both Group and business levels, assessing business line

profitability on a risk adjusted basis and the management and allocation

of capital.