RBS 2013 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review

127

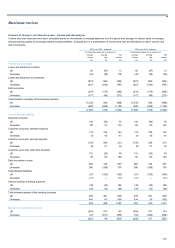

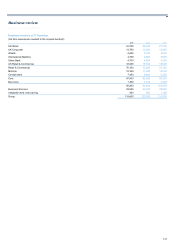

Impairment losses

Managed (1) Statutory

2013 2012 2011 2013 2012 2011

£m £m £m £m £m £m

New impairment losses 8,688 5,620 7,964 8,688 5,620 9,234

Less: recoveries of amounts previously written-off (256) (341) (527) (256) (341) (527)

Charge to income statement 8,432 5,279 7,437 8,432 5,279 8,707

Comprising:

Loan impairment losses 8,412 5,315 7,241 8,412 5,315 7,241

Securities

- sovereign debt impairment and related interest rate hedge

adjustments — — — — — 1,268

- other 20 (36) 196 20 (36) 198

Charge to income statement 8,432 5,279 7,437 8,432 5,279 8,707

Of which RCR related (2) 4,490 — — 4,490 — —

Notes:

(1) Managed basis excludes sovereign debt impairment and related interest rate hedge adjustments.

(2) Pertaining to the creation of RCR and related strategy.

RBS Capital Resolution ('RCR') was set up from 1 January 2014 and will

manage a pool of £29 billion of assets with particularly high capital

intensity or potentially volatile outcomes in stressed environments, aiming

to accelerate the run-down of these exposures over a three year period to

free up capital for the bank. This revised strategy to run down high risk

loans faster resulted in an increased impairment charge relating to

impaired or non-performing assets transferred to RCR, reflecting adverse

changes in our estimates of future cash flows. Further details about RCR

are set out on pages 160 to 163.

2013 compared with 2012 - managed and statutory

Group loan impairment losses rose by 58% to £8,412 million reflecting

the increased provisions recognised in connection with the creation of

RCR. Adjusting for this, impairment losses fell by £1,393 million (26%) to

£3,922 million, driven by significant improvements in Non-Core, Ulster

Bank and UK Retail, partially offset by increases in International Banking,

US Retail & Commercial and Markets.

Additional loan impairments arising from the RCR accelerated asset

recovery strategy totalled £4,490 million, of which £3,118 million related

to Non-Core, £892 million to Ulster Bank, £410 million to UK Corporate,

£52 million to International Banking and £18 million to Markets.

Excluding the impact of the creation of RCR, Core Ulster Bank loan

impairments fell by £482 million (35%) to £882 million, mainly as a result

of continued improvement in retail mortgage debt-flow and in recovery

trends. UK Retail loan impairments fell by £210 million (40%), primarily

from lower default levels.

Excluding the impact of the creation of RCR, Non-Core loan impairments

fell by £792 million to £1,528 million, reflecting the continued reduction in

the overall portfolio.

2012 compared with 2011 - managed and statutory

Loan impairment losses declined by £1,926 million to £5,315 million,

primarily driven by a £1,518 million fall in Non-Core impairments, mostly

in the Ulster Bank and commercial real estate portfolios.

Core loan impairments were down £408 million, or 12%, largely due to

lower default rates in UK Retail and an improved credit environment for

US Retail & Commercial, which helped drive impairment reductions of

£259 million and £165 million respectively. Core Ulster Bank impairments

stabilised, though still at a very high level (£1,364 million in 2012 versus

£1,384 million in 2011).

Loan impairments as a percentage of gross loans and advances

improved by 30 basis points, principally reflecting the improved credit

profile in Non-Core and the better US credit environment.

Loan impairment provisions rose to £21.3 billion, increasing coverage of

risk elements in lending to 52%, compared with 49% in 2011.