RBS 2013 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

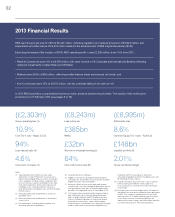

03

2013 Financial Results

Restructuring our balance sheet

Third party assets were reduced by £130 billion over the course of 2013, with

Markets down £72 billion and Non-Core down £29 billion. In the five years since the

end of 2008, the funded balance sheet has been reduced by £487 billion and total

assets by £1,191 billion.

The Core Tier 1 ratio was 10.9% at 31 December 2013. On a fully loaded Basel III

basis, the Common Equity Tier 1 ratio was 8.6%. The impact of the regulatory and

redress provisions booked in Q4 2013 was already reflected in our future capital

plan, and RBS continues to target a fully loaded Basel III Common Equity Tier 1 ratio

of c.11% by the end of 2015 and 12% or above by the end of 2016.

Continued improvement in credit quality, particularly in the UK Retail and Non-

Core portfolios, saw risk elements in lending fall by 4%. Reflecting the increased

impairments associated with the creation of RCR, provision coverage increased from

52% at end 2012 to 64% at end 2013.

RBS remains highly liquid, with short-term wholesale funding down £10 billion

to £32 billion at the end of 2013, covered more than four times by a £146 billion

liquidity portfolio.

Building a bank that is trusted

by its customers

RBS has announced a refreshed strategic

direction with the ambition of building a bank

that earns its customers’ trust by serving them

better than any other bank.

The bank will be structured around the needs

of its customers, with seven existing operating

divisions realigned into three businesses:

Personal & Business Banking, Commercial &

Private Banking and Corporate & Institutional

Banking.

Ulster Bank in Northern Ireland will benefit

from a closer integration with our personal,

business and commercial banking franchises

in Great Britain. We are continuing to explore

further opportunities in the Republic of Ireland

with a view to being a challenger to the

systemic banks.

To position RBS to deliver a sustainable

overall return on tangible equity of 12% plus

in the long term, we must achieve a significant

reduction in costs and complexity.

This simplification is intended to deliver

significant improvements to services delivered

to our customers while at the same time

helping to bring our cost base down from

£13.3 billion in 2013 to £8 billion in the medium

term(9).

Future performance will be reported against

customer and financial measures. Further

details are set out on page 10.

Operating results

RBS recorded an operating profit(1) of £2,520

million excluding the impact of the creation of

RCR which reduced income by £333 million

and increased impairments by £4,490 million.

Including these RCR-related impairment

and other losses of £4,823 million(10), RBS

recorded an operating loss of £2,303 million.

Group income, excluding the RCR impact,

was down 10% to £19,775 million, principally

reflecting a £1,161 million reduction in Markets

income, with expenses down 4% to £13,313

million.

Retail & Commercial operating profit,

excluding £1,385 million of impairments and

other losses related to the creation of RCR,

was down 4% to £4,078 million, with lower

income in UK Corporate and International

Banking offsetting improved impairments in

Ulster Bank and UK Retail.

Markets operating profit, excluding £18 million

of impairments related to the creation of RCR,

was down 58% to £638 million, reflecting its

smaller balance sheet and reduced risk levels.

Non-Core losses, excluding £3,420 million of

impairments and other losses related to the

creation of RCR, were down 27% to £2,107

million, with the cost base falling in line with

run-off.

Loss attributable to shareholders was £8,995

million, reflecting the charges relating to the

creation of RCR and legacy conduct litigation

and redress, the write-down of goodwill and

other intangible assets and deferred tax assets.

Tangible net asset value per ordinary and B

share was 363p at 31 December 2013.