RBS 2013 Annual Report Download - page 231

Download and view the complete annual report

Please find page 231 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

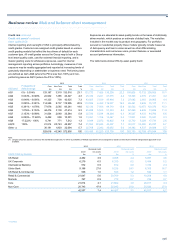

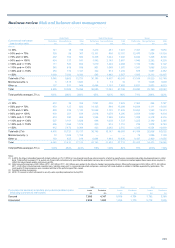

Business review Risk and balance sheet management

229

Risk management*

Product/asset class concentration framework

The Group manages certain lines of business where the nature of credit

risk assumed could result in a concentration or a heightened risk in some

other form. This includes specific credit risk types such as settlement or

wrong-way risk and products such as long-dated derivatives or

securitisations. These product and asset classes may require formal

policies and expertise as well as tailored monitoring and reporting

measures. In some cases specific limits and thresholds are deployed to

ensure that the credit risk inherent in these lines of business and

products is adequately controlled. Product and asset classes are

reviewed regularly. The reviews consider the risks inherent in each

product or asset class, the risk controls applied, monitoring and reporting

of the risk, the client base, and any emerging risks to ensure risk appetite

remains appropriate.

Sector concentration

Exposures are assigned to, and reviewed in the context of, a defined set

of industry sectors. Risk appetite and portfolio strategies are set at either

the sector or sub-sector level, depending on where exposures may result

in excessive concentration, or where trends in both external factors and

internal portfolio performance give cause for concern. Regular formal

reviews are undertaken at Group or divisional level depending on

materiality. Reviews may include an assessment of the Group’s franchise

in a particular sector, an analysis of the outlook, identification of key

vulnerabilities or stress testing.

As a result of the reviews carried out in 2013, the Group further reduced

its risk appetite in the corporate sectors of commercial real estate and

retail. For further details on sector-specific strategies, exposure reduction

and key credit risks, refer to pages 252 to 267.

Single name concentration

A single name concentration (SNC) framework addresses the risk of

outsized exposure to a borrower or borrower group. The framework

includes elevated approval authority, additional reporting and monitoring,

and the requirement for plans to address exposures in excess of appetite.

Several credit risk mitigation techniques are available to reduce single

name concentrations. If the Group decides that its exposure is too high, it

may decide to sell excess exposures. Alternatively, it may decide to take

additional security or guarantees such as cash, bank or government

guarantees or enter into credit default swaps. Credit risk mitigants must

be effective in terms of legal certainty and enforceability. In addition,

maturity or expiry dates must be the same, or later, than the underlying

obligations.

Aggregate SNC exposures remain outside of the Group’s longer-term

appetite. However, material reductions have been achieved since the

framework was introduced. This trend continued during the year, with a

21% decrease in the number of excesses since December 2012.

Country concentration

The country concentration framework is described in the Country risk

section on pages 341 to 353.

*unaudited

Retail

A product and asset class framework exists to control credit risk for retail

businesses. It sets limits that measure and control the asset quality of

each key business area, the portfolios in that business and the new

business being originated. The actual performance of each portfolio is

tracked relative to these limits and action taken where necessary.

Credit risk assessment

Wholesale

The credit risk function assesses, approves and manages the credit risk

associated with a borrower or group of related borrowers.

The GCCO has established a framework of individual delegated

authorities, which are set out in the Group Credit Risk Policy. The

framework requires at least two individuals to approve each credit

decision, one from the business and one from the credit risk function.

Both must hold appropriate delegated authority, which is dependent on

their experience and expertise. Only a small number of senior executives

hold the highest authority provided under the framework. While both

parties are accountable for the quality of each decision taken, the credit

risk approver holds ultimate sanctioning authority.

In all circumstances the risks associated with any proposal to provide,

increase, review or change the terms or conditions of credit facilities must

be assessed prior to a credit decision being made. Assessments of credit

risk must, at a minimum, specifically address the following elements:

• The amount, terms, tenor, structure, conditions, purpose and

appropriateness of all credit facilities;

• Compliance with applicable Group and/or divisional credit policies;

• The customer’s ability to meet obligations, based on an analysis of

financial information and a review of payment and covenant

compliance history;

• The source of repayment and the customer’s risk profile, including

sector analysis and sensitivity to economic and market

developments, and credit risk mitigation;

• Refinancing risk - that is the risk of loss arising from the failure of a

customer to settle an obligation on expiry of a facility through the

drawdown of another credit facility provided by the Group or by

another lender;

• Consideration of all other risks such as environmental, social and

ethical, regulatory and reputational risks; and

• The portfolio impact of the transaction, including the impact on any

credit risk concentration limits or agreed divisional risk appetite.

At a minimum, credit relationships are reviewed and re-approved

annually. The renewal process addresses borrower performance,

including reconfirmation or adjustment of risk parameter estimates; the

adequacy of security; compliance with terms and conditions; and

refinancing risk.