RBS 2013 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review

139

2013 saw a major shake-up of the UK financial advice landscape with the

implementation of the Retail Distribution Review (RDR). Clients

welcomed Coutts’ new fully compliant advice-led model where Coutts

requires its advisers to achieve the more stringent Level 6 rating, in

excess of the FCA’s minimum Level 4 requirement. Coutts has received a

number of industry accolades for its levels of service, such as ‘UK Private

Bank of the Year’ (The Banker Global Private Banking Awards). Total

assets under advice grew to approximately £3 billion over the year.

Following the deposit re-pricing strategy implemented in the second half

of 2013 deposit margins have significantly improved. Lending volumes

have remained resilient despite pay-downs in line with best-advice policy

under RDR. In addition, a new international trust strategy was

announced, strengthening the client offering by positioning it as a market-

leading, client-centric trust business. This was achieved by the creation of

a centre of excellence in Jersey, accompanied by withdrawal from the

Cayman Islands and restructuring of the Geneva trust business.

Work continued on streamlining client-facing processes and driving

increased benefits from the division’s global technology platform,

including significant enhancements to Coutts’ online and digital client

channels. A streamlining of the London property footprint from 11

buildings to 2 was also concluded, alongside further office rationalisation

in the International business.

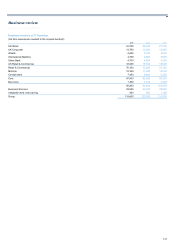

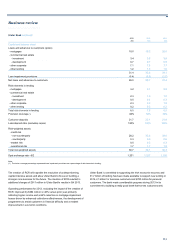

2013 compared with 2012

Operating profit was 9% lower at £221 million, driven by lower income

partially offset by a decrease in expenses and impairment losses.

Income declined by 7% to £1,093 million, with the reduction in net interest

income reflecting the lower spread earned on deposits as a result of

lower Group funding requirements.

Non-interest income fell by 7% to £419 million due to the disposal of the

Latin American, Caribbean and African businesses for a profit of £15

million in H1 2012 together with a decline in fee income in the

International business.

Expenses were 4% lower at £843 million as a result of reduced

headcount, tight discretionary cost management and the non-recurrence

of two regulatory fines totalling £26 million incurred during 2012. This was

partially offset by a one-off UK tax treaty charge in the International

business.

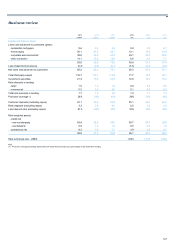

Client assets and liabilities managed by the division declined by 2%, with

a £1.7 billion reduction in deposits following re-pricing initiatives in the UK

in line with the wider Group funding strategy. Assets under management

increased by 3% due to positive market movements. Lending was 2%

lower, reflecting increased levels of repayments in the UK.

Impairments were £17 million lower at £29 million, largely reflecting a

small number of specific impairments.

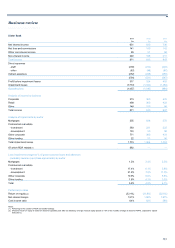

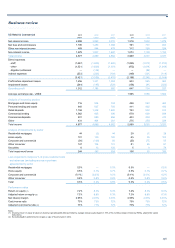

2012 compared with 2011

Operating profit increased by £1 million to £243 million driven by higher

income partially offset by increased expenses and impairment losses.

Total income increased by £66 million, with net interest income up £75

million, largely driven by improvements in margins and strong divisional

treasury income, particularly during H1 2012.

Non-interest income fell by 2% as the gain from the disposal of the Latin

American, Caribbean and African businesses was more than offset by a

decline in fee income in the UK and lower investment volumes, driven by

continued economic uncertainty.

Expenses were £44 million or 5% higher at £881 million, with significant

investment in change programmes, including the development of new

products and services capability and the implementation of RDR in the

UK.

Expenses also increased as a result of client redress following a past

business review into the sale of the ALICO Enhanced Variable Rate Fund

announced in November 2011 and a Financial Services Authority fine of

£8.75 million relating to Anti Money Laundering control processes.

Client assets and liabilities fell by 1% with a £2 billion decrease in assets

under management, primarily reflecting low margin client outflows of £1.4

billion and the impact of client transfers following the disposal of the Latin

American, Caribbean and African businesses. This fall was partially offset

by increases in lending and deposit volumes.

Impairment losses were £46 million, up £21 million, largely reflecting a

small number of large specific impairments.