RBS 2013 Annual Report Download - page 358

Download and view the complete annual report

Please find page 358 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

360 -

361

361 -

362

362 -

363

363 -

364

364 -

365

365 -

366

366 -

367

367 -

368

368 -

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

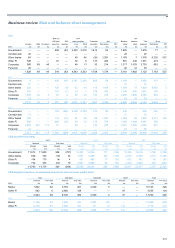

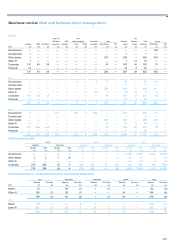

Business review Risk and balance sheet management

356

Other risks* continued

Conduct risk continued

Risk mitigation

Assurance and monitoring activities are essential to ensure that the

Group can demonstrate compliance with existing rules and regulations,

assess whether it is managing its conduct risks appropriately, and

determine whether key controls are effective. In 2013, the Group Conduct

and Regulatory Affairs assurance function provided Group-wide

assurance over specific compliance topics, as well as thematic process

reviews.

Pension risk

Definition

Pension risk is the risk arising from contractual or other liabilities to, or

with respect to, the Group’s pension schemes, whether established for its

employees or for those of a related company or otherwise. It also means

the risk that the Group may make payments or other contributions to, or

with respect to, a pension scheme because of a moral obligation, or

because it considers that it needs to do so for some other reason.

Sources of risk

The Group has exposure to pension risk through its defined benefit

schemes worldwide. The five largest schemes, which represent around

96% of the Group’s pension liabilities, are the Royal Bank of Scotland

Group Pension Fund (‘main scheme’), the Ulster Bank Pension Scheme

(Republic of Ireland), the Ulster Bank Pension Scheme, the Royal Bank

of Scotland Americas Pension Plan and the Royal Bank of Scotland

International Pension Trust. The main scheme is the principal source of

pension risk.

Pension scheme liabilities vary with changes in long-term interest rates

and inflation as well as with pensionable salaries, the longevity of scheme

members and changes in legislation. Meanwhile, pension scheme assets

vary with changes in interest rates, inflation expectations, credit spreads,

exchange rates and equity and property prices. The Group is exposed to

the risk that the market value of the schemes’ assets - together with

future returns and any additional future contributions - becomes

insufficient to meet liabilities as they fall due. In such circumstances, the

Group could be obliged (or may choose) to make additional contributions

to the schemes or be required to hold additional capital to mitigate this

risk.

Governance

The main scheme operates under a trust deed. The trustee is responsible

for the investment of the main scheme’s assets which are held separately

from the assets of the Group. The Group and the trustee must agree on

the plan to fund the main scheme. The corporate trustee, RBS Pension

Trustee Limited, is a wholly owned subsidiary of The Royal Bank of

Scotland plc. The trustee board currently comprises six directors selected

by the Group and three directors nominated by members.

*unaudited

The Pension Risk Committee, acting as a sub-committee of the Group

Asset and Liability Management Committee (GALCO), considers the

Group’s view of pension risk. The Pension Risk Committee considers

mechanisms that could potentially be used for managing risk within the

funds as well as financial strategy and employee welfare implications, It

also reviews actuarial assumptions from a sponsor perspective as

appropriate. The Pension Risk Committee is a key component of pension

risk management and serves as a formal link between the Group and the

Investment Executive, which acts on behalf of the trustee of the Group’s

largest pension schemes, where risk management, asset strategy and

financing issues are discussed. The Investment Executive also consults

with the Group to obtain its view on the appropriate level of risk within the

pension fund.

For further information on the Group’s risk governance, see page 176.

Risk management

Risk appetite and investment policy for the schemes are defined by the

trustee with quantitative and qualitative input from actuaries and

investment advisers.

As the sponsor of its defined benefit pension schemes, the Group

manages the risk it faces using a pension risk management framework.

This encompasses risk monitoring, modelling, stress testing and

reporting. As sponsor, the Group maintains an independent view of the

risk inherent in its pension funds. In addition to the scrutiny provided by

the Pension Risk Committee, the Group also achieves this through

regular pension risk monitoring and reporting to the Group Board, Group

Executive Committee and Group Board Risk Committee on the material

pension schemes that the Group has an obligation to support.

Risk measurement

Pension risk reporting is submitted to the Group Board monthly in the

RBS Risk Management Report. The report includes an assessment of

the sensitivities of the Group’s pension schemes to interest rates and

inflation, a breakdown of the assets by class, and measurement of the

overall deficit or surplus position based on the latest data.

Throughout 2013, various pension risk stress-testing initiatives were

undertaken, focused both on internally defined scenarios and on

scenarios to meet integrated PRA stress testing requirements.

Risk mitigation

The trustee has taken measures partially to mitigate inflation and interest

rate risks both by investing in suitable physical assets and by entering

into inflation and interest rate swaps. The main scheme also uses

derivatives to manage the allocation of the portfolio to different asset

classes and to manage risk within asset classes. The assets of the main

scheme, which represent 85% of Group pension plan assets at 31

December 2013, are invested in a diversified portfolio of quoted and

private equity, government and corporate fixed interest and index-linked

bonds, and other assets including property and hedge funds.