RBS 2013 Annual Report Download - page 239

Download and view the complete annual report

Please find page 239 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

237

Key points

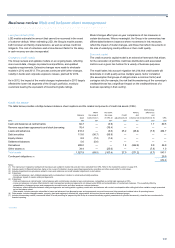

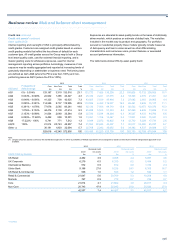

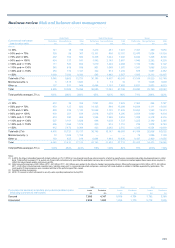

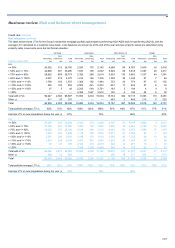

• Trends in the asset quality of the Group’s credit risk exposures

during 2013 reflected the change in the proportion of assets in the

sovereign sector and movements in the underlying asset quality of

the portfolio. The Group’s overall asset quality for performing assets

improved slightly year-on-year.

• The increase in the proportion of the Group’s Core exposures in the

AQ1 band reflected the increase in the Group’s exposure to

sovereigns, in line with the Group’s liquidity and capital management

practices.

• The increase in AQ4 was due to a positive shift in the asset quality

band distribution of UK Retail and reflected improvements in the

underlying credit quality of the UK Retail mortgage portfolio over the

last three years.

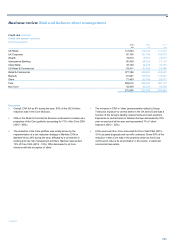

• Trends in the Group’s non-performing credit risk exposures in 2013

were predominantly driven by the Non-Core and Ulster Bank

portfolios, with these two divisions accounting for 70% of the

Group's AQ10 CRA.

• Property continued to be the largest sector in non-performing assets

- 57% of total AQ10 exposure (2012 - 58%).

• Non-performing assets in the Ulster Bank portfolio continued to

grow, driven by exposures in the wholesale property sector. Refer to

Key loan portfolios: Ulster Bank Group (Core and Non-Core) on

pages 265 to 267 for more details.

• The personal sector accounted for 21% (2012 - 21%) of the Group’s

AQ10 exposure. AQ10 exposure in this sector decreased during the

year for all divisions except Ulster Bank.

• In UK Retail non-performing assets continued to fall, principally as a

result of lower flows of assets into non-performing across all

portfolios, as well as write-downs of aged debt.

• The slight decrease in the level of AQ10 exposure in UK Corporate

was driven primarily by reductions in the property sector, offset by

increases in shipping. At the year end, shipping represented 12% of

the AQ10 assets in UK Corporate (2012 - 8%).

• Non-Core exposure fell in all AQ bands.

*unaudited

Risk mitigation

Risk mitigation techniques are used in the management of credit

portfolios across the Group, typically to mitigate credit concentrations in

relation to an individual customer, a borrower group or a collection of

related borrowers. Where possible, the Group nets customer credit

balances against obligations.

Mitigation tools applied can include: structuring a security interest in a

physical or financial asset; use of credit derivatives, including credit

default swaps, credit-linked debt instruments and securitisation

structures; and use of guarantees and similar instruments (for example,

credit insurance) from related and third parties.

When seeking to mitigate risk, at a minimum the Group considers the

following:

• The suitability of the proposed risk mitigation, particularly if

restrictions apply;

• The means by which legal certainty is to be established, including

required documentation, supportive legal opinions and the steps

needed to establish legal rights;

• Acceptable methodologies for initial and subsequent valuation of

collateral, the frequency of valuation and the advance rates given;

• The actions it can take if the value of collateral or other mitigants is

less than needed;

• The risk that the value of mitigants and counterparty credit quality

may deteriorate simultaneously;

• The need to manage concentration risks arising from collateral

types; and

• The need to ensure that any risk mitigation remains legally effective

and enforceable.

The Group’s business and credit teams are supported by specialist in-

house documentation teams. The Group uses industry-standard loan and

security documentation wherever possible. However, when the Group

uses non-standard documentation, external lawyers are employed on a

case-by-case basis.