RBS 2013 Annual Report Download - page 265

Download and view the complete annual report

Please find page 265 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

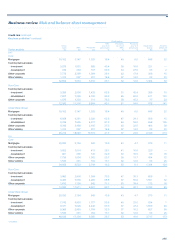

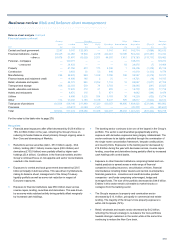

Business review Risk and balance sheet management

263

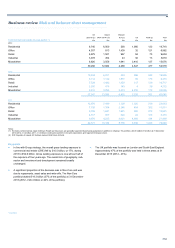

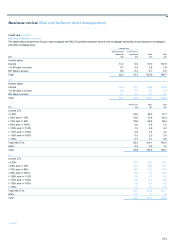

2013 2012

Bullet principal Conversion Proportion of Bullet principal Conversion Proportion of

repayment to amortising Total mortgage lending repayment to amortising Total mortgage lending

£bn £bn £bn % £bn £bn £bn %

UK Retail (1) 25.4 — 25.4 25.6 28.1 — 28.1 28.4

Ulster Bank 0.7 1.4 2.1 11.0 1.4 1.8 3.2 16.7

RBS Citizens 0.4 8.9 9.3 47.5 0.5 9.0 9.5 44.1

Wealth 6.0 — 6.0 69.0 5.7 0.1 5.8 66.0

Total 32.5 10.3 42.8 35.7 10.9 46.6

Note:

(1) UK Retail also has exposure of £7.7 billion to customers who have a combination of repayment types, capital repayments and interest only.

UK Retail

UK Retail’s interest only mortgages require full principal repayment

(bullet) at the time of maturity. Typically such loans have remaining terms

of between 15 and 20 years. Customers are reminded of the need to

have an adequate repayment vehicle in place during the mortgage term.

Of the bullet loans that matured in the six months to 30 June 2013, 53%

had been fully repaid by 31 December 2013. The unpaid balance totalled

£51 million, 96% of which continued to meet agreed payment

arrangements (including balances that have been restructured on a

capital and interest basis within eight months of the contract date;

customers are allowed eight months leeway for their investment plan to

mature and cashed in to repay the mortgage). Of the £51 million unpaid

balance, 56% of the loans had an indexed LTV of 70% or less with only

14% above 90%. Customers may be offered a short extension to the term

of an interest only mortgage or a conversion of an interest only mortgage

to one featuring repayment of both capital and interest, subject to

affordability and characteristics such as the customer’s income and

ultimate repayment vehicle. The majority of term extensions in UK Retail

are classified as forbearance.

Ulster Bank

Ulster Bank’s interest only mortgages require full principal repayment

(bullet) at the time of maturity; or payment of both capital and interest

from the end of the interest only period, typically seven years, so that

customers meet their contractual repayment obligations. For bullet

customers, contact strategies are in place to remind them of the need to

repay principal at the end of the mortgage term.

Of the bullet mortgages that matured in the six months to 30 June 2013

(£1.2 million), 20% had fully repaid by 31 December 2013 leaving

residual balances of £0.9 million, 78% of which were meeting the terms of

a revised repayment schedule. Of the amortising loans that matured in

the six months to 30 June 2013 (£65 million), 69% were either fully repaid

or meeting the terms of a revised repayment schedule.

*unaudited

Ulster Bank also offers temporary interest only periods to customers as

part of its forbearance programme. An interest only period of up to two

years is permitted after which the customer enters an amortising

repayment period following further assessment of the customer’s

circumstances. The affordability assessment conducted at the end of the

forbearance period takes into consideration the repayment of the arrears

that have accumulated based on original terms during the forbearance

period. The customer’s delinquency status does not deteriorate further

while forbearance repayments are maintained. Term extensions in

respect of existing interest only mortgages are offered only under a

forbearance arrangement.

RBS Citizens

RBS Citizens has a book of interest only bullet repayment HELOC loans

(£0.4 billion at 31 December 2013) for which repayment of principal is

due at maturity, and an interest only portfolio that comprises loans that

convert to amortising after an interest only period that is typically 10 years

(£8.9 billion at December 2013 of which £8.0 billion are HELOCs). The

majority of the bullet loans are due to mature between 2014 and 2015. Of

the bullet loans that matured in the six months to 30 June 2013, 50% had

fully repaid or are current as of 31 December 2013. The residual

balances (modified, delinquent, and charged-off) made up £21 million.

For those loans that convert to amortising, the typical uplift in payments is

currently 210% (average uplift calculated at £132 per month).

Delinquency rates have shown a modest increase in the over 30 days

arrears rate.