RBS 2013 Annual Report Download - page 338

Download and view the complete annual report

Please find page 338 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

336

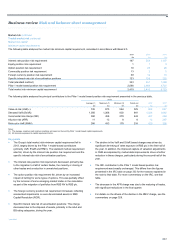

Market risk continued

Non-traded market risk continued

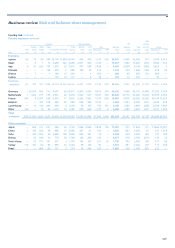

The following table shows the sensitivity of net interest income, over the

next 12 months, to an immediate upward or downward change of 100

basis points to all interest rates. In addition, the table includes the impact

of a gradual 400 basis point steepening (bear steepener) and a gradual

300 basis point flattening (bull flattener) of the yield curve for tenors

greater than a year.

The scenarios represent annualised interest rate stresses of a scale

deemed sufficient to trigger a modification in customer behaviour. The

asymmetry in the steepening and flattening scenarios reflects the

difference in the expected behaviour of interest rates as they approach

zero.

The reported sensitivities will vary over time due to a number of factors

such as market conditions and strategic changes to the balance sheet

mix and should not therefore be considered predictive of future

performance.

Euro Sterling US dolla

r

Othe

r

Total

2013 £m £m £m £m £m

+ 100 basis point shift in yield curves 59 416 175 31 681

− 100 basis point shift in yield curves (29) (333) (82) (15) (459)

Bear steepener 403

Bull flattener (273)

2012

+ 100 basis point shift in yield curves (29) 472 119 27 589

− 100 basis point shift in yield curves (20) (257) (29) (11) (317)

Bear steepener 216

Bull flattener (77)

2011

+ 100 basis point shift in yield curves (19) 190 59 14 244

− 100 basis point shift in yield curves 25 (188) (4) (16) (183)

Bear steepener 443

Bull flattener (146)

Key points

• The Group's interest rate exposure remains asset sensitive, such

that rising rates will have a positive impact on its net interest income.

• The Group’s increased sensitivity to parallel shifts in the yield curve

over a 12 month horizon primarily reflects the higher volume of

structural hedges maturing in 2014 relative to 2013. This reflects the

maturity profile of legacy hedges. If rates were to rise, these would

be reinvested at higher rates, with an upward impact on net interest

income. This increased sensitivity also reflects changes in

underlying pricing assumptions for customer loans and deposits.

• The increased sensitivity to the steepening and flattening scenarios

is also primarily driven by the maturity profile of structural hedges.

Structural hedging*

Banks generally have the benefit of a significant pool of stable, non and

low interest bearing liabilities, principally comprising equity and money

transmission accounts. These balances are usually hedged, either by

investing directly in longer-term fixed rate assets or by the use of interest

rate swaps, in order to provide a consistent and predictable revenue

stream.

The Group targets a weighted average life for these economic hedges.

This is accomplished using a continuous rolling maturity programme to

achieve the desired profile and is primarily managed by Group Treasury.

The maturity profile of the hedge aims to reduce the potential sensitivity

of income to rate movements. The structural hedging programme is

Group wide, capturing the position within the UK banking group and

regulated subsidiaries in other jurisdictions.