RBS 2013 Annual Report Download - page 247

Download and view the complete annual report

Please find page 247 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

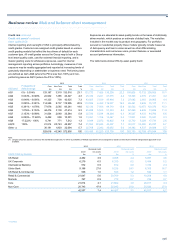

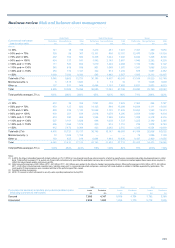

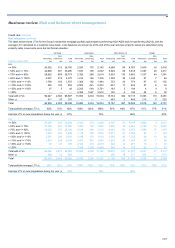

Business review Risk and balance sheet management

245

Retail

Collections

Collections functions in each of the Group’s retail businesses provide

support and assistance to customers who are experiencing difficulties in

meeting their obligations to the Group. Such customers may miss a

payment on their loan or borrow more than their agreed limit, or contact

the Group themselves asking for help. Dedicated support teams are also

in place to identify and help customers who have not yet missed a

payment but may be facing financial difficulty.

The collections function may use a range of tools to initiate contact with

the customer, establish the cause of their financial difficulty and support

them where possible. In the process, they may consider granting the

customer forbearance.

Additionally, in the UK and Ireland, support is provided to customers with

unsecured loans who establish a repayment plan with the Group through

a debt advice agency or a self-help tool. Such “breathing space”

suspends collections activity for a 30-day period to allow time for the

repayment plan to be put in place. Arrears continue to accrue for

customer loans granted breathing space.

If collections strategies are unsuccessful the relationship is transferred to

the recoveries team. For further details on recoveries, refer to page 250.

Retail forbearance

Definition

Forbearance takes place when a concession is made on the contractual

terms of a loan in response to a customer's financial difficulties. In UK

Retail and Ulster Bank, a broader definition of forbearance is used that

includes mortgages where a customer has made a change to contractual

terms, when their payments status is up-to-date and they are not

necessarily evidencing signs of financial difficulty. Forbearance is granted

on a permanent, or temporary, basis following an assessment of the

customer's individual circumstances and ability to pay. For UK Retail and

Ulster Bank, the disclosure covers changes in contractual terms dating

back to January 2008 and early 2009 respectively.

Identification

Customers who contact the bank directly because of financial difficulties,

or who are already in payment arrears, may be granted forbearance. In

the course of assisting customers, more than one forbearance treatment

may be granted.

Types of retail forbearance

Forbearance is granted principally to customers with mortgages and less

extensively to customers with unsecured loans.

Mortgage portfolios

Forbearance options include, but are not limited to, payment

concessions, capitalisations of arrears, term extensions and temporary

conversions to interest only.

• Payment concessions - A temporary reduction in, or elimination of,

the periodic (usually monthly) loan repayment is agreed with the

customer. At the end of the concessionary period, forborne principal

and accrued interest outstanding is scheduled for repayment over

an agreed period. Ulster Bank and RBS Citizens also offer payment

concessions in the form of discounted interest rates that involve the

forgiveness of some interest (further details below).

• Capitalisation of arrears - The customer repays the arrears over the

remaining term of the mortgage and returns to an up-to-date

position.

• Term extensions - The maturity date of the loan is extended.

• Interest only conversions - The loan converts from principal and

interest repayment to interest only repayment on a temporary basis

(Ulster Bank only).

In UK Retail, interest only conversions have not been used to support

customers in financial difficulty since 2009, and from 2012 have only

been permitted on a very exceptional basis for residential mortgage

customers who are up to date on payments. As a result interest only

loans with permanent changes to terms are historical stock. In Ulster

Bank, interest only conversions are offered to customers under financial

stress and solely on a temporary basis.

In response to the economic difficulties in the Republic of Ireland, Ulster

Bank has developed additional forbearance options. These payment

concessions support customers over an extended period of time and

include instances where some interest is forgiven by granting interest rate

discounts for a 3-5 year period.

Similarly RBS Citizens participates in the US government mandated

Home Affordable Modification Program as well as its own proprietary

programme. Both feature a combination of term extensions,

capitalisations of arrears, interest rate reductions and conversions from

interest only to amortising. These tend to be permanent changes to

contractual terms. In order to qualify for either of the programmes,

customers must meet government-specified or internal criteria designed

to evidence financial difficulty but demonstrate a willingness to pay.