RBS 2013 Annual Report Download - page 240

Download and view the complete annual report

Please find page 240 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

238

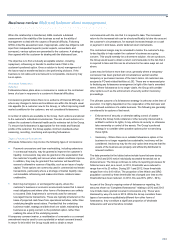

Credit risk continued

Risk mitigation continued

Lending

The types of collateral the Group takes to mitigate the credit risk arising

from wholesale lending varies according to the nature of the counterparty

and its assets. The most common types are:

• Commercial real estate - The market value of the collateral typically

exceeds the loan amount at origination date. The market value is

defined as the estimated amount for which the asset could be sold in

an arm’s length transaction by a willing seller to a willing buyer. In

Ireland and, to a lesser extent, the UK, a lack of market data has

made estimating the value of property difficult and so causes the

Group to use a range of other types of information to value such

collateral, including expert judgement and indices. For further

information, regarding the Group’s commercial real estate portfolio

refer to pages 252 to 257.

• Residential property - The Group takes collateral in the form of

residential property to mitigate the credit risk arising from mortgages

and home equity lending. The Group values residential property

during the loan underwriting process by either appraising properties

individually or using statistically valid models. The Group updates

residential property values quarterly using the relevant residential

property index, namely the Halifax Quarterly Regional House Price

Index in the UK, the Case-Shiller Home Price Index in the US, the

Central Statistics Office Residential Property Price Index in the ROI,

and the Nationwide House Price Index in Northern Ireland.

• Physical assets - These may include stock, plant, equipment,

machinery, vehicles, ships and aircraft. Such assets are suitable

collateral only if the Group can identify, locate, and segregate them

from other assets on which it does not have a claim. The Group

values physical assets in a variety of different ways, depending on

the type of asset concerned and may rely on balance sheet

valuations in certain cases. In the US, the Group also takes

collateral in the form of motor vehicles to mitigate the credit risk

arising from automobile lending. The Group values new vehicles at

cost and used ones at the relevant average trade-in value.

• Receivables - These are amounts owed to the Group’s

counterparties by their own customers. The Group values them after

taking into account the quality of its counterparty’s receivable

management processes and excluding any that are past due.

All collateral is assessed case-by-case to ensure that it will retain its

value independently of the provider. The Group monitors the value of the

collateral and, if there is a shortfall, will seek additional collateral.

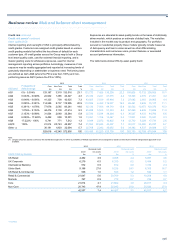

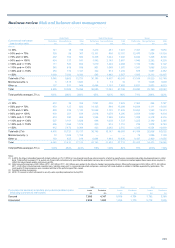

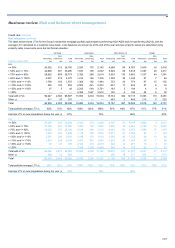

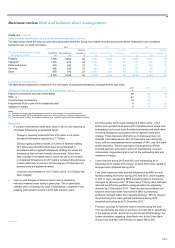

The table below analyses commercial real estate (Core and Non-Core) lending by loan-to-value ratio, which represents loan value before provisions

relative to the value of the property financed.

Ulster Bank Rest of the Group Group

Performing Non-performing Total Performing Non-performing Total Performing Non-performing Total

Commercial real estate

loan-to-value ratio £m £m £m £m £m £m £m £m £m

2013

<= 50% 124 23 147 7,884 262 8,146 8,008 285 8,293

> 50% and <= 70% 271 55 326 9,962 582 10,544 10,233 637 10,870

> 70% and <= 90% 282 89 371 3,699 1,272 4,971 3,981 1,361 5,342

> 90% and <= 100% 86 154 240 865 368 1,233 951 522 1,473

> 100% and <= 110% 121 212 333 690 627 1,317 811 839 1,650

> 110% and <= 130% 238 366 604 333 1,334 1,667 571 1,700 2,271

> 130% and <= 150% 102 438 540 267 1,161 1,428 369 1,599 1,968

> 150% 319 6,738 7,057 150 2,629 2,779 469 9,367 9,836

Total with LTVs 1,543 8,075 9,618 23,850 8,235 32,085 25,393 16,310 41,703

Minimal security (1) 6 3,144 3,150 54 13 67 60 3,157 3,217

Other (2) 144 1,351 1,495 5,230 933 6,163 5,374 2,284 7,658

Total 1,693 12,570 14,263 29,134 9,181 38,315 30,827 21,751 52,578

Total portfolio average LTV (3) 121% 376% 335% 61% 149% 84% 65% 261% 142%

For the notes to this table refer to the following page.