RBS 2013 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review

134

UK Retail continued

• Significant focus on streamlining processes has benefited all

distribution channels, with the capacity created allowing more time

for staff coaching and resulting in advisors spending more time and

having better conversations with customers.

• In addition, our product range has been simplified down from 56 to

46 with several products winning awards. A highlight of this UK

Retail strategy is the success of the new instant saver product

launched in Q4 2012, which at the end of 2013 had more than £10

billion in balances. Furthermore, nearly 800,000 customers have

registered for Cashback Plus online since launch in Q3 2013 and

are being rewarded for using their debit cards with selected retailers.

• A major branch refurbishment programme is under way with over

one quarter completed. 350 branches now have a digital banking

zone where customers can use in-branch technology to access

online banking. Wi-Fi in-branch allows customers to access their

account via their own devices.

During 2013 good progress has been made with FCA (Financial Conduct

Authority) reportable complaints, which declined 22%. In addition, the

provision relating to historic Payment Protection Insurance (PPI) mis-

selling was increased by £860 million, bringing the total to £3.0 billion.

The PPI expense is not included in the operating profit of UK Retail.

In 2014, UK Retail will aim to maintain a leading position in digital

banking, launching new capability and customer proposition through

mobile devices.

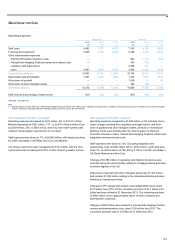

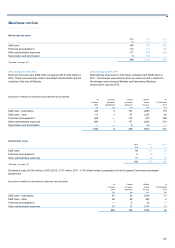

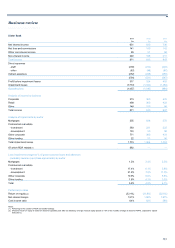

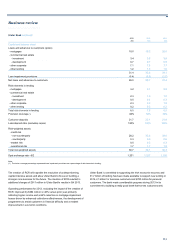

2013 compared with 2012

Operating profit increased by 3% to £1,943 million driven by a 39%

decline in impairment losses. Net interest income was broadly stable,

though investment advice income was adversely impacted following

changes introduced by the Retail Distribution Review (RDR). Costs

increased primarily because of a higher FSCS levy and other regulatory

charges totalling £116 million in the year, conduct-related provisions of

£63 million and additional technology investment of £45 million.

Mortgage balance growth was affected in H1 2013 by mortgage advisor

training; however, balances recovered during H2 2013 assisted by early

adoption of the second phase of the UK Government’s Help To Buy

scheme. Gross lending increased to £8.9 billion in H2 2013. Customer

deposits increased by 7%, above the UK market average of 4% due to

strong growth in both current accounts (13%) and instant access savings

accounts (15%).

Net interest income was broadly flat.

• Mortgage new business margins reduced in line with market

conditions; however, overall book margins improved.

• Deposit margins declined reflecting the impact of continued lower

rates on current account hedges. Savings margins, however, have

increased over 2013 with improved market pricing.

Non-interest income fell by 2% to £958 million due to subdued advice

income post RDR.

Direct costs increased by 7% due to higher FSCS levy and other

regulatory charges and conduct-related provisions of £63 million. This

was partly offset by lower staff costs due to a reduction in headcount of

2,300. Indirect costs increased by 3%, largely due to investment in

technology.

Impairments declined by 39% to £324 million due to lower customer

defaults across all products reflecting continued improvement in asset

quality.

Risk-weighted assets declined by 4% to £43.9 billion largely reflecting

balance reductions across the unsecured portfolio and quality

improvements.

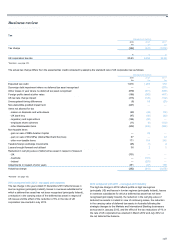

2012 compared with 2011

Operating profit fell by 6% as a 10% decline in income was only partly

offset by lower costs, down 6%, and improved impairment losses, down

33%.

Mortgage balances grew by £4.1 billion with the share of new business at

10%, ahead of our stock level of 8%. Growth as a result of FLS was

starting to appear by the end of the year as mortgage applications moved

through the pipeline to completion. Deposit growth of 6% was in line with

the market and drove a 300 basis point improvement in the loan:deposit

ratio to 103%.

Net interest income was down 7% due to weaker deposit margins and

reduction in unsecured balances, partly offset by mortgage growth.

Unsecured balances now represent 13% of total loans and advances to

customers compared with 23% in 2008, following realignment of risk

appetite and strong mortgage growth. Net interest margin declined as a

result of lower rates on current account hedges and increased

competition on savings rates in the early part of the year, partly offset by

widening asset margins.

Non-interest income was 19% lower mainly due to:

• lower unauthorised overdraft fees as we continue to help customers

manage their finances by providing mobile text alerts and further

improving mobile banking functionality;

• weak consumer confidence lowering spending and associated fees

on cards; and

• lower investment income as a result of weak customer demand and

less advisor availability due to restructuring and retraining in

preparation for regulatory changes in 2013.

Costs were down £150 million, 6%, driven by the ongoing simplification of

processes across the business, lower headcount and lower FSCS levy.

Impairment losses were £259 million or 33% lower, reflecting the

continued benefit of risk appetite tightening in prior years and also a

smaller unsecured loan book. Impairments as a percentage of loans and

advances were 50 basis points versus 70 basis points in 2011.

Risk-weighted assets continued to improve over the year as the portfolio

mix adjusted, with increases in lower-risk secured mortgages, decreases

in unsecured lending and further quality improvements across the book.