RBS 2013 Annual Report Download - page 151

Download and view the complete annual report

Please find page 151 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

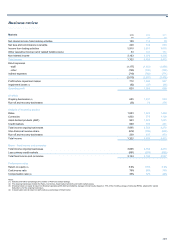

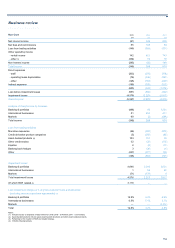

Business review

149

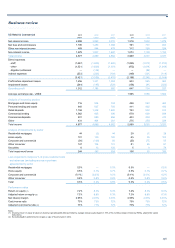

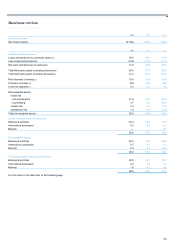

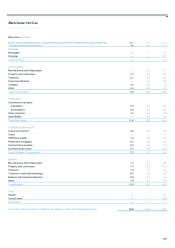

2013 compared with 2012

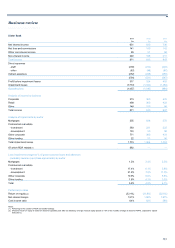

Operating profit of £647 million ($1,012 million) was down £107 million

($184 million), or 14%. The operating environment and market conditions

remained challenging, with intense competition for loans. An extended

period of low short-term rates limited net interest margin expansion and

the rise in long-term rates dramatically slowed mortgage refinance

volumes.

Net interest income was down 1% at £1,916 million ($2,998 million) due

to a smaller investment portfolio, consumer loan run-off and the effect of

prevailing economic conditions on asset yields partially offset by the

benefit of interest rate swaps, commercial loan growth and favourable

funding costs.

Average loans and advances were flat, with commercial loan growth of

5% despite competition for lending opportunities offset by run-off of long-

term fixed-rate consumer products.

Average customer deposits were flat, with planned run-off of high priced

time deposits and lower wholesale deposits offset by growth achieved in

checking and money market balances. Consumer checking balances

grew by 3% while small business checking balances grew by 7% over the

year.

Excluding the £47 million ($75 million) gross gain on the sale of Visa B

shares in 2012, non-interest income was down £39 million ($83 million),

or 4% at £1,073 million ($1,679 million), reflecting lower mortgage

banking fees as refinancing volumes have slowed, and lower deposit

fees. This was partially offset by higher securities gains and commercial

banking fee income.

Excluding the £88 million ($138 million) litigation settlement in 2012

relating to a class action lawsuit regarding the way overdraft fees were

assessed on customer accounts prior to 2010 and the £8 million ($13

million) litigation reserve associated with the sale of Visa B shares, total

expenses of £2,186 million ($3,421 million) were broadly in line with prior

year. This largely reflects a mortgage servicing rights impairment

recapture driven by the increase in long-term rates offset by the cost of

regulatory compliance and new technology investments and a one-off

£21 million ($33 million) pension gain in 2012.

Impairment losses increased by £65 million ($99 million) to £156 million

($244 million) for the year and represented 0.3% of loans and advances

to customers.

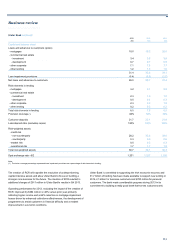

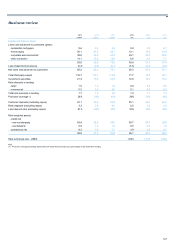

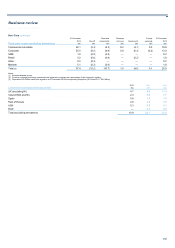

2012 compared with 2011

US Retail & Commercial posted an operating profit of £754 million

($1,196 million), up £217 million ($336 million), or 40%, from 2011.

Excluding the £88 million ($138 million) litigation settlement in Q1 2012

and the £39 million ($62 million) net gain on the sale of Visa B shares in

Q2 2012, operating profit was up £266 million ($412 million), or 50%,

largely reflecting lower impairment losses due to an improved credit

environment.

Net interest income was up £53 million ($47 million), or 3%, driven by

targeted commercial loan growth, deposit pricing discipline and lower

funding costs. This was partially offset by consumer loan run-off and

lower asset yields reflecting prevailing economic conditions.

Non-interest income was up £7 million. In US dollar terms non-interest

income was down $10 million, or 1%, reflecting a decline in debit card

fees as a result of the Durbin Amendment legislation and lower securities

gains and deposit fees. This was largely offset by strong mortgage

banking fees of £69 million ($109 million), up 71%, and the £47 million

($75 million) gross gain on the sale of Visa B shares.

Gross loans and advances to customers were down £0.3 billion. In US

dollar terms loans and advances to customers were up $3.1 billion, or

4%, due to strong growth in commercial loan volumes.

Customer deposits decreased by 1% as a result of movements in foreign

exchange rates partially offset by strong growth achieved in checking

balances. Consumer checking balances fell by 1% while small business

checking balances grew by 4% over the year.

Excluding the £88 million ($138 million) litigation settlement, relating to a

class action lawsuit regarding the way overdraft fees were assessed on

customer accounts prior to 2010, and the £8 million ($13 million) litigation

reserve associated with the sale of Visa B shares, and a one-off £21

million ($33 million) pension gain in Q4 2012, total expenses were down

1%, reflecting lower loan collection costs and the elimination of the

Everyday Points rewards programme for consumer debit card customers,

partially offset by higher operational losses.

During the year, RBS Citizens offered former employees a one-time

opportunity to receive the value of future pension benefits as a single

lump sum payment. The transaction allowed RBS Citizens to partially de-

risk its pension plan and future liability under the plan. A strong

participant take-up rate of 60% enabled RBS Citizens to reduce its

pension liability by 17% and recognise a £21 million ($33 million)

accounting gain.

Impairment losses were down £235 million ($379 million), or 72%,

reflecting an improved credit environment and lower impairments on

securities. Loan impairments improved by £168 million ($266 million)

driven primarily by commercial loan impairments. Impairments as a

percentage of loans and advances fell to 20 basis points.