RBS 2013 Annual Report Download - page 425

Download and view the complete annual report

Please find page 425 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

415 -

416

416 -

417

417 -

418

418 -

419

419 -

420

420 -

421

421 -

422

422 -

423

423 -

424

424 -

425

425 -

426

426 -

427

427 -

428

428 -

429

429 -

430

430 -

431

431 -

432

432 -

433

433 -

434

434 -

435

435 -

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Notes on the consolidated accounts

423

Notes:

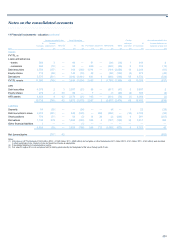

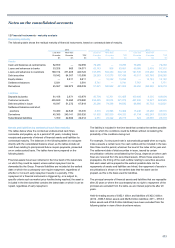

(1) Level 3 structured issued debt securities of £1.3 billion are not included in the table above as valuation is consistent with the valuation of the embedded derivative component.

(2) Price and yield: There may be a range of price based information used for evaluating the value of an instrument. This may be a direct comparison of one instrument or portfolio with another or

movements in a more liquid instrument may be used to indicate the movement in the value of less liquid instrument. The comparison may also be indirect in that adjustments are made to the price to

reflect differences between the pricing source and the instrument being valued, for example different maturity, credit quality, seniority or expected payouts. Similarly to price, an instrument’s yield may

be compared to other instruments either directly or indirectly. Prices move inversely to yields.

(3) Credit spreads and discount margins: Credit spreads and margins express the return required over a benchmark rate or index to compensate for the credit risk associated with a cash instrument. A

higher credit spread would indicate that the underlying instrument has more credit risk associated with it. Consequently, investors require a higher yield to compensate for the higher risk. The

discount rate comprises credit spread or margin plus the benchmark rate; it is used to value future cash flows.

(4) Recovery rate: Reflects market expectations about the return of principal for a debt instrument or other obligations after a credit event or on liquidation. Recovery rates tend to move conversely to

credit spreads.

(5) Probability of default: This is a measure of the expected rate of losses in an underlying portfolio of mortgages or other receivables. The higher the probability of default the lower the value of the

underlying portfolio. The cumulative losses tend to move conversely to prepayment rates and in line with constant default rates. The higher the rate, the higher the expected number of defaults and

therefore the expected losses. An increase in the default rate is likely to reduce the value of an asset.

(6) Volatility: A measure of the tendency of a price to change with time.

(7) Conditional prepayment rate: The measure of the rate at which underlying mortgages or loans are prepaid. An increase in prepayment rates in a portfolio may increase or decrease its value

depending upon the credit quality and payment terms of the underlying loans. For example an increase in prepayment rate of a portfolio of high credit quality underlying assets may reduce the value

and size of the portfolio whereas for lower credit quality underlyings it may increase the value.

(8) EBITDA (earnings before interest, tax, depreciation and amortisation) multiple: This is a commonly used valuation technique for equity holdings. The EBITDA of a company is used as a proxy for the

future cash flows and when multiplied by an appropriate factor gives an estimate for the value of the company.

(9) Correlation: Measures the degree by which two prices or other variables are observed to move together. If they move in the same direction there is positive correlation; if they move in opposite

directions there is negative correlation. Correlations typically include relationships between: default probabilities of assets in a basket (a group of separate assets), exchange rates, interest rates and

other financial variables.

(10) Upfront points: These are similar to credit spreads in that a higher figure is a measure of increased credit risk. A credit derivative price can be quoted on either credit spread or upfront points basis

and the two can be considered a near equivalent from a risk perspective. As with credit spreads higher upfront points indicate that the underlying entity has a higher credit risk associated with it.

(11) The Group does not have any material liabilities measured at fair value that are issued with an inseparable third party credit enhancement.

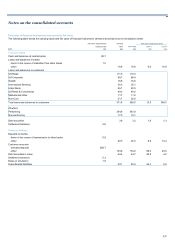

The level 3 sensitivities above are calculated at a trade or low level

portfolio basis. They are not calculated on an overall portfolio basis and

therefore do not reflect the likely overall potential uncertainty on the

whole portfolio. The figures are aggregated and do not reflect the

correlated nature of some of the sensitivities. In particular, for some of the

portfolios the sensitivities may be negatively correlated where a

downwards movement in one asset would produce an upwards

movement in another, but due to the additive presentation of the above

figures this correlation cannot be displayed. The actual potential

downside sensitivity of the total portfolio may be less than the non-

correlated sum of the additive figures as shown in the above table.

Judgmental issues

The diverse range of products traded by the Group results in a wide

range of instruments that are classified into level 3 of the hierarchy.

Whilst the majority of these instruments naturally fall into a particular

level, for some products an element of judgment is required. The majority

of the Group’s financial instruments carried at fair value are classified as

level 2: inputs are observable either directly (i.e. as a price) or indirectly

(i.e. derived from prices).

Active and inactive markets

A key input in the decision making process for the allocation of assets to

a particular level is liquidity. In general, the degree of valuation

uncertainty depends on the degree of liquidity of an input. For example, a

derivative can be placed into level 2 or level 3 dependent upon the

liquidity of level 3 inputs.

Where markets are liquid or very liquid, little judgment is required.

However, when the information regarding the liquidity in a particular

market is not clear, a judgment may need to be made. This can be made

more difficult as assessing the liquidity of a market may not always be

straightforward. For an equity traded on an exchange, daily volumes of

trading can be seen, but for an over-the counter (OTC) derivative

assessing the liquidity of the market with no central exchange can be

more difficult.

A key related issue is where a market moves from liquid to illiquid or vice

versa. Where this change is considered to be temporary, the

classification is not changed. For example, if there is little market trading

in a product on a reporting date but at the previous reporting date and

during the intervening period the market has been considered to be

liquid, the instrument will continue to be classified in the same level in the

hierarchy. This is to provide consistency so that transfers between levels

are driven by genuine changes in market liquidity and do not reflect short

term or seasonal effects.

Interaction with the IPV process

The determination of an instrument’s level cannot be made at a global

product level as a single product type can be in more than one level. For

example, a single name corporate credit default swap could be in level 2

or level 3 depending on whether the reference counterparty is liquid or

illiquid.