RBS 2013 Annual Report Download - page 328

Download and view the complete annual report

Please find page 328 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

326

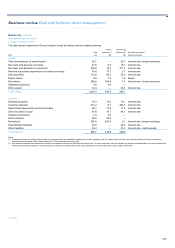

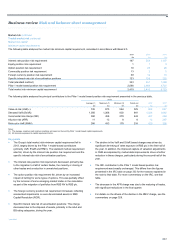

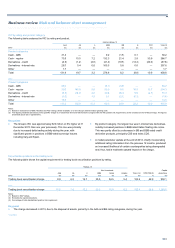

Market risk continued

Traded market risk continued

VaR validation*

In addition to the independent VaR model reviews carried out by GRA

(discussed on page 323), a dedicated model-testing team within Market

Risk works with the risk managers to:

• Test the accuracy of the valuation methods used in the VaR model

on appropriately chosen test portfolios and trades.

• Apply in-house models to perform advanced internal back-testing to

complement the regulatory back-testing.

• Ensure that tests capture the effect of using external data proxies

where these are used.

• Identify risks not adequately captured in VaR, and ensure that such

risks are addressed via the RNIV framework (see page 328).

• Identify any model weaknesses or scope limitations and their

impact.

• Identify and give early warning of any market or portfolio weakness

that may become significant.

As well as being an important market risk measurement and control tool,

the VaR model is also used to determine a significant component of the

market risk capital requirement (see page 332 for more information on

calculation of capital requirements). Therefore, it is subject to not only

ongoing internal review and validation but also regulator-prescribed back-

testing.

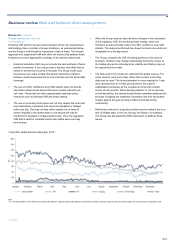

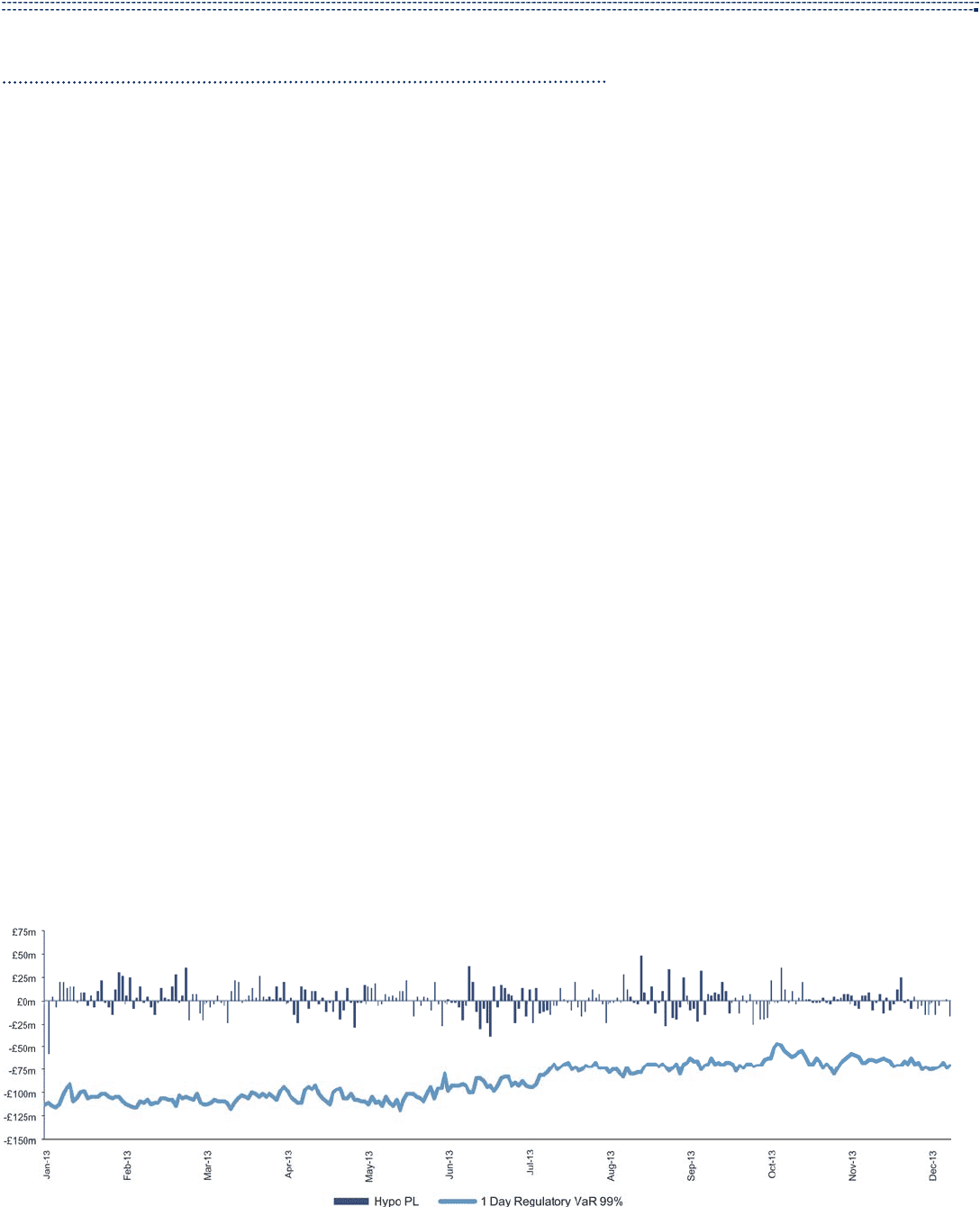

VaR back-testing*

The main approach employed to assess the ongoing model performance

is back-testing, which counts the number of days when a loss exceeds

the corresponding daily VaR estimate, measured at a 99% confidence

level.

There are two types of profit and loss (P&L) used in back-testing

comparisons: Clean P&L and Hypothetical (Hypo) P&L.

The Clean P&L figure for a particular business day is the firm’s actual

P&L for that day in respect of the trading activities within the scope of the

firm’s regulatory VaR model, adjusted by stripping out:

• Fees and commissions;

• Brokerage;

• Additions to, and releases from, reserves that are not directly related

to market risk; and

• Any Day 1 P&L exceeding an amount of £500,000 (per transaction).

The Hypo P&L reflects the firm’s Clean P&L excluding any intra-day

activities.

A portfolio is said to produce a back-testing exception when the Clean or

Hypo P&L exceeds the VaR level on a given day. Such an event may be

caused by a large market movement or may highlight issues such as

missing risk factors or inappropriate time series. Any such issues

identified are analysed and addressed through taking appropriate

remediation or development action. The Group monitors both Clean and

Hypo back-testing exceptions.

Regulatory back-testing is performed and reported on a daily basis for

legal entities and major business portfolios. Divisional market risk teams

also perform back-testing at the lower levels as part of the internal

ongoing VaR model validation.

The back-testing described above primarily applies to Markets and Non-

Core models, which are approved by the regulators. However, where

appropriate, back-testing is also performed for other portfolios that are

not subject to regulatory approval.

The graph below presents 1-day 99% regulatory VaR vs. Hypo P&L for RBS plc, the Group's largest legal entity by market risk RWAs and positions.