RBS 2013 Annual Report Download - page 350

Download and view the complete annual report

Please find page 350 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

360 -

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

348

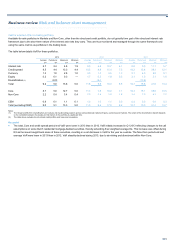

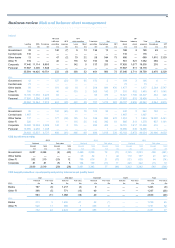

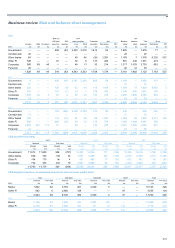

Country risk continued

Country exposure continued

• Eurozone periphery - despite the appreciation of the euro against

sterling, balance sheet exposure decreased to £52.9 billion, a

reduction of £6.6 billion or 11%, in nearly all countries, as follows:

° Ireland - exposure decreased by £2.1 billion to £37.0 billion, in

all broad product categories. Residential and commercial real

estate lending declined slightly to £16.9 billion and £10.3

billion, respectively. Provisions increased by £2.8 billion, most

of which related to corporate lending.

° Spain - Group Treasury’s holdings of covered bonds (cedulas)

decreased by £0.7 billion due to sales in improved market

conditions. Corporate lending decreased by £1.3 billion to £2.9

billion, with commercial real estate lending more than halving,

largely as a result of disposals in Non-Core, to £0.8 billion.

° Italy - the £1.3 billion decrease in exposure to £5.2 billion

reflected reductions in lending and derivatives to corporate

clients. Net HFT debt exposure fluctuates as the Group is a

market-maker in Italian government bonds. Off-balance sheet

exposure to corporates and non-bank financial institutions also

declined, by £0.7 billion.

° Portugal - exposure declined further by £0.4 billion to £0.9

billion. The remaining exposure mainly consisted of corporate

lending to a few large highly creditworthy clients and

collateralised derivatives trading with the largest local banks.

° Greece - exposure decreased by £0.2 billion to £0.4 billion,

caused by reductions in lending and derivatives. The

remaining exposure comprised mostly of collateralised

derivatives exposure to banks and corporate lending, including

exposure to local subsidiaries of international companies.

° Cyprus - exposure increased slightly to £0.2 billion, most of

which was covered by parental and export credit agency

guarantees from elsewhere.

• Germany - balance sheet exposure decreased from £48.4 billion to

£23.9 billion principally owing to a £16.4 billion reduction in cash

balances held with the central bank. AFS government bonds

decreased by £4.1 billion in line with treasury management

strategies. Lending to corporate clients decreased by £1.1 billion,

principally in the commercial real estate, oil and gas, and media

sectors.

*unaudited

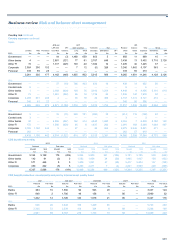

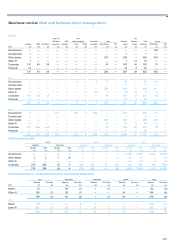

• Netherlands - balance sheet exposure decreased from £23.6 billion

to £16.1 billion. AFS debt securities issued by non-bank financial

institutions declined by £2.8 billion, primarily following repayments.

Corporate lending decreased by £0.8 billion, primarily in commercial

real estate. Off-balance sheet exposure to corporate clients

decreased by £1.1 billion, mainly in the telecommunications, retail

and food and consumer sectors.

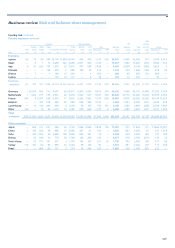

• France - balance sheet exposure decreased from £19.7 billion to

£14.0 billion. The net long HFT position in government bonds

declined by £1.9 billion in the course of normal trading in the rates

business.

• Japan - balance sheet exposure decreased by £6.0 billion to £5.3

billion. Net HFT and AFS government bonds fell by £5.1 billion and

£1.5 billion, respectively, and derivatives exposure, largely to banks,

decreased by £0.5 billion. This reflected depreciation of the yen,

lower trading flows and a reduction in Japanese bonds held as

derivatives collateral. Lending to the central bank increased by £0.8

billion.

• China - lending to banks increased by £1.8 billion to £2.8 billion.

Corporate lending rose by £0.5 billion to £1.5 billion, reflecting

customer demand. Derivatives exposure to public sector entities

decreased by £0.5 billion to £0.4 billion owing to fluctuations in

short-term hedging by clients.

• India - balance sheet exposure decreased by £1.3 billion to £3.8

billion, driven largely by reductions in lending to banks and to the

telecommunications and oil and gas sectors.

• CDS positions - the Group approximately halved its European CDS

positions by consolidating its derivatives portfolio through contract

terminations to reduce risks and capital requirements in line with

strategic plans, while maturities reduced the positions further. This

resulted in major reductions in the gross notional value of CDS

protection bought and sold. Net bought protection in terms of CDS

notional less fair value, also fell by £1.2 billion to £5.6 billion, with

reductions particularly in the Netherlands and France.

• Funding mismatches - the estimated funding mismatch at risk of

redenomination for Ireland was £6.5 billion at the end of the year,

falling from £9.0 billion a year before due to an increase in

provisions and a reduction in assets. The mismatch for Spain was

£6.5 billion, up from £4.5 billion as the Group reduced its local

funding (and associated cost) given the improved outlook for the

country. The net position for Italy fell to £0.5 billion from £1.0 billion.

The net positions for Portugal, Greece and Cyprus were all minimal.

Overall, perceived risks of redenomination events in the eurozone

declined considerably in 2013.