RBS 2013 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

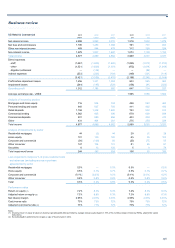

Business review

136

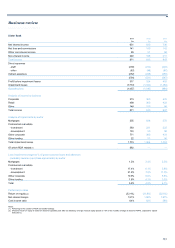

UK Corporate continued

2013 2012 2011

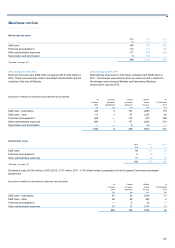

Performance ratios

Return on equity (1) 7.9% 14.5% 15.2%

Net interest margin 3.07% 3.06% 3.06%

Cost:income ratio 50% 44% 44%

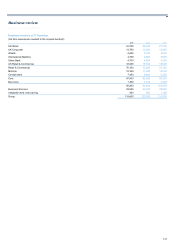

Capital and balance sheet £bn £bn £bn

Loans and advances to customers (gross)

- financial institutions 5.5 5.8 5.8

- hotels and restaurants 4.7 5.6 6.1

- housebuilding and construction 2.9 3.4 3.9

- manufacturing 4.2 4.7 4.7

- private sector education, health, social work, recreational and community services 8.5 8.7 8.7

- property 22.0 24.8 28.2

- wholesale and retail trade, repairs 8.2 8.5 8.7

- asset and invoice finance 11.7 11.2 10.4

- shipping 6.5 7.6 7.8

- other 28.3 26.7 26.4

102.5 107.0 110.7

Loan impairment provisions (2.8) (2.4) (2.1)

Net loans and advances to customers 99.7 104.6 108.6

Total third party assets 105.0 110.2 114.2

Risk elements in lending 6.2 5.5 5.0

Provision coverage (2) 46% 45% 40%

Customer deposits 124.7 127.1 126.3

Loan:deposit ratio (excluding repos) 80% 82% 86%

Risk-weighted assets

- credit risk (non-counterparty) 77.7 77.7 71.2

- operational risk 8.4 8.6 8.1

Total risk-weighted assets 86.1 86.3 79.3

Notes:

(1) Divisional return on equity is based on divisional operating profit after tax, divided by average notional equity (based on 10% of the monthly average of divisional RWAs, adjusted for capital

deductions).

(2) Provision coverage percentage represents loan impairment provisions as a percentage of risk elements in lending.

2013 was a year in which UK Corporate underlined its commitment to

support the UK economy and played an active role in the communities it

operates in.

As part of this commitment the Bank appointed Sir Andrew Large to

undertake a thorough and independent review of the lending standards

and practices used by RBS and NatWest. UK Corporate will implement

all of the Independent Lending Review’s recommendations and is

adopting a revised strategy and capabilities to enhance support to SMEs

and the wider UK economic recovery while maintaining sound lending

practices.

As part of the division’s concerted effort to support its SME customers,

UK Corporate has been proactively reviewing the business needs of SME

customers to understand if they could benefit from the offer of additional

facilities. In 2013, over 12,000 customers were identified for additional

funding under UK Corporate’s 'Statements of Appetite' initiative. The

initiative resulted in approximately £6 billion of new funding being offered

to customers.

The division has continued to support the government-backed Funding

for Lending Scheme (FLS) and as at 31 December 2013 had allocated in

excess of £4.7 billion of new FLS-related lending to almost 25,000

customers, £3.1 billion of which has been drawn since the scheme was

launched. Mid-sized manufacturers are being offered targeted support,

with interest rates reduced by more than 1% in some cases. SME

customers benefited from both lower interest rates and the removal of

arrangement fees.